Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Are Home Prices Going To Fall?

It’s one of the biggest concerns many buyers have right now: “What if I buy a home and prices drop afterward?”

With so much uncertainty in the headlines, it’s understandable to feel cautious. No one wants to make a major financial decision at the wrong time. But it’s important not to focus too heavily on the few areas experiencing small price declines right now.

When you step back and look at the bigger picture, home values have historically trended upward over time.

What the Data Really Shows

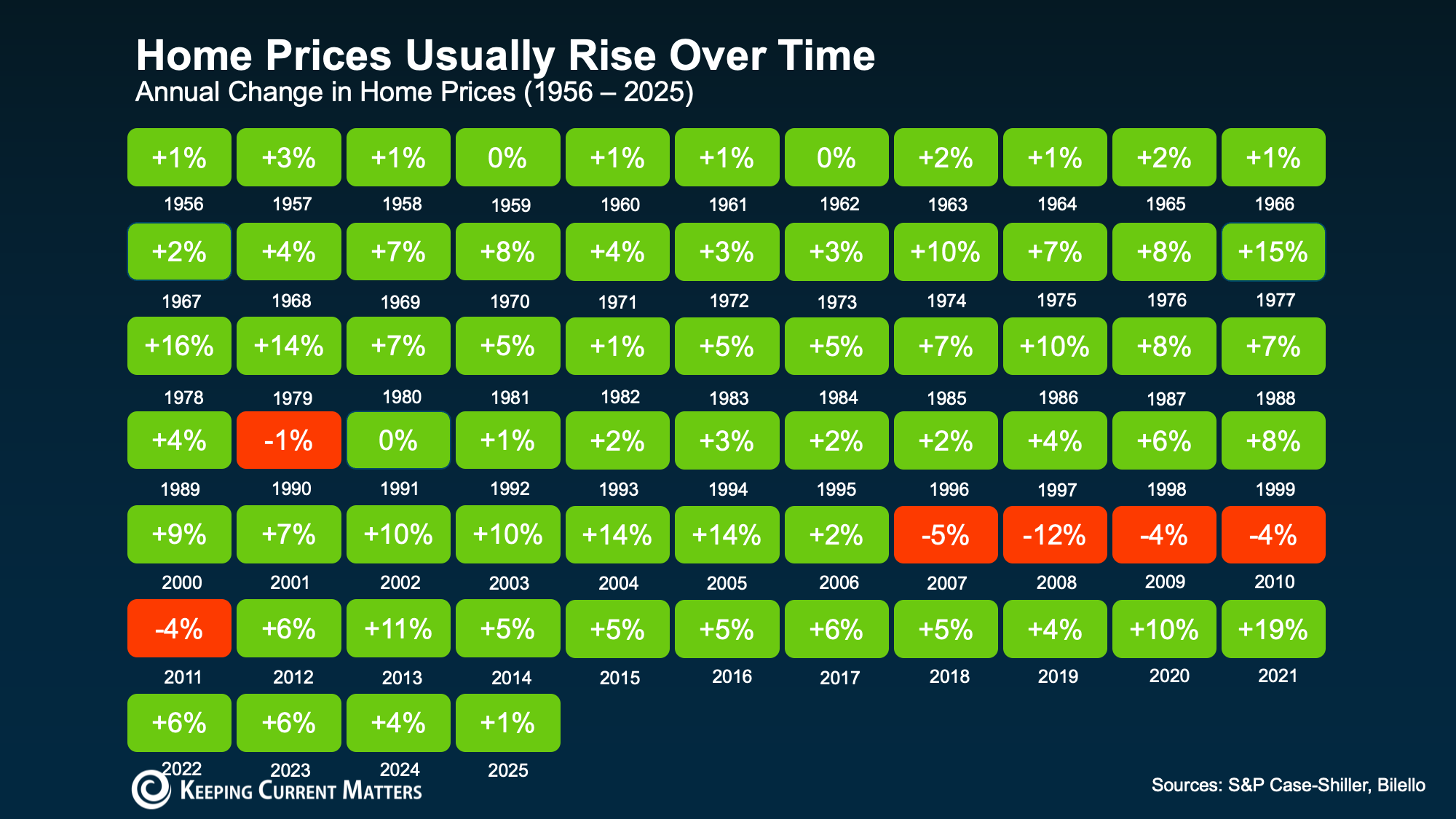

Take a look at the visual below. Using data from Case-Shiller and Bilello, it highlights how home prices have performed year after year dating back to the 1950s.

Here’s the most important takeaway.

Aside from the housing crash, home prices have remained stable or appreciated in nearly every year over the past several decades (see visual below):

a chart of percentages and numbers

That’s an incredibly consistent pattern — and one that many headlines tend to overlook.

While short-term fluctuations can happen, it’s the long-term growth that matters most.

Why Prices Typically Increase Over Time

There are several key reasons home prices generally continue to rise:

People will always need housing. Life changes like new jobs, growing families, marriages, and relocations mean there will always be buyers in the market. Demand may shift at times, but the need for housing never disappears.

Inventory is still limited. Although more homes have come onto the market recently, there still aren’t enough available homes nationwide to meet buyer demand. That imbalance continues to support home prices.

Inflation plays a role. As the cost of goods and services rises over time, home values tend to rise as well.

What That Means for You as a Buyer

It’s easy to worry about where prices may go next month or even next year — especially if you’re buying your first home and making a significant financial commitment. But historically, the overall trend has been clear: home prices tend to appreciate over time.

Of course, that doesn’t mean every market rises every single year. Real estate is local, and short-term changes can happen. We’re seeing some of that in certain markets today. You can even spot a few temporary declines in the visual above.

But historically, those downturns haven’t lasted forever.

That’s why buying a home is usually recommended when you plan to stay put for several years — often at least five. That timeframe can help you build equity and ride out any temporary market shifts.

And over time, rising home values can strengthen your net worth and help build long-term wealth.

The best decision isn’t about perfectly timing the market. It’s about making a move that fits your goals and staying long enough to benefit from the long-term trend.

Bottom Line

Home prices have consistently increased over the long run, which is why real estate is often viewed as a strong long-term investment.

That doesn’t mean you need to buy right now. The right time to move is when it makes sense for your situation and future plans.

But if you’ve been feeling uncertain, let this offer some reassurance. And if you’d like to talk about what’s happening in our local market, your goals, or your timeline, connect with a trusted local real estate professional.

Stay or Sell? How To Make the Right Call as You Age

Thinking Ahead About Your Long-Term Housing Plans

At some point, as you begin thinking about the years ahead, this question often comes up:

“Can I comfortably stay here long-term… or would moving make more sense?”

It’s not always an urgent thought. Often, it comes up during everyday moments — walking up and down the stairs, keeping up with home maintenance, or simply wondering what the next chapter of life may look like in your current home.

For many people, the answer is clear: they want to stay.

The USC Leonard Davis School of Gerontology found that nearly 90% of adults over 65 would prefer to remain in their homes as they age (see below).

But even when staying feels like the right choice, it’s still important to think ahead about what that could realistically look like over time. That’s where having the right real estate agent by your side can make a difference.

What To Consider If You Plan To Stay in Your Home

Aging in place is absolutely possible. However, having a plan in place can make the process much easier.

The reality is, the home that once fit your lifestyle perfectly may need adjustments as your needs change over the years. Planning ahead can help you better prepare for those future costs and avoid feeling overwhelmed later on.

In some cases, the updates are simple, like installing grab bars in the bathroom. In other situations, they may involve larger changes, such as modifying layouts or relocating essential living spaces to the main floor.

While some improvements are relatively minor, others may require a more significant investment. Thinking about these things early is valuable because it gives you time:

- Time to understand what changes your home may need

- Time to explore different options

- Time to connect with trusted contractors

- Time to spread out the cost of improvements over time

According to ElderLife Financial, here’s a general estimate of what certain updates could cost depending on the work involved (see below).

If staying in your home is important to you, but the costs feel overwhelming, there may be options available. Depending on your circumstances, financial assistance programs or tools like home warranties could help offset unexpected expenses.

Before starting major updates, it’s also a smart idea to have a conversation with a local real estate agent. They can help you understand which improvements make the most sense for your goals and how those changes could affect your home’s value in today’s market.

When Moving May Make More Sense

At the same time, staying isn’t always the best solution for everyone. According to Pegasus Senior Living:

“While most seniors hope to age in place, practical considerations sometimes make selling a home the wiser choice.”

Sometimes, it comes down to recognizing when the home that once made life easier begins to create new challenges.

Those challenges may include:

- Maintenance or yardwork becoming harder to manage

- Stairs or home layouts becoming less practical day-to-day

- Needing more support, care, or closer proximity to loved ones

For some homeowners, it’s simply about lifestyle. Many people don’t want to take on major renovations. Others are ready to simplify, downsize, or move somewhere that better supports this next stage of life — whether that’s a smaller home, a 55+ community, or a location closer to family.

In many situations, moving is simply about making everyday life more comfortable and manageable.

Bottom Line

There’s no one-size-fits-all answer.

Some homeowners choose to stay and make updates over time. Others decide to move and simplify their lifestyle. Both can be the right decision depending on your needs and goals.

The important thing isn’t making a decision today. Instead, it’s understanding your options early so, when the time comes, you can move forward feeling informed and confident instead of rushed.

And if you ever want someone to help you think through what your future options may look like, a trusted local real estate agent is there to help.

3 Things That Are Not Going To Happen in Today’s Housing Market

There’s a lot of uncertainty right now, and that’s fueling some pretty dramatic headlines. If you’re thinking about buying a home, it can leave you feeling unsure about your next move.

A recent study by CNBC asked homebuyers what concerns them most, and three key themes came up repeatedly:

Mortgage rates

The number of homes for sale

Home prices

But much of what you’re hearing about these topics is driven more by misconceptions than facts. Let’s break it down and separate reality from the noise.

Misconception #1: “I’ll Wait Because Mortgage Rates Will Drop Dramatically”

There’s a common belief circulating that mortgage rates are about to fall significantly, making it smarter to hold off on buying.

But is that actually likely?

While mortgage rates have eased slightly in recent weeks, forecasts don’t point to a major drop anytime soon. The most probable outlook is that rates will hover in the low 6% range throughout the year.

That’s not a significant shift from where they are today.

Of course, this could change depending on inflation and the broader economy. But based on current data, waiting for a big drop may not pay off the way some expect. As U.S. News & World Report notes:

“Mortgage rates aren’t expected to change much over the next several quarters . . .”

It’s also worth noting that affordability has already improved compared to last year. So even if rates remain relatively stable, conditions are still better than they were.

Misconception #2: “There Are Too Many Homes for Sale Right Now”

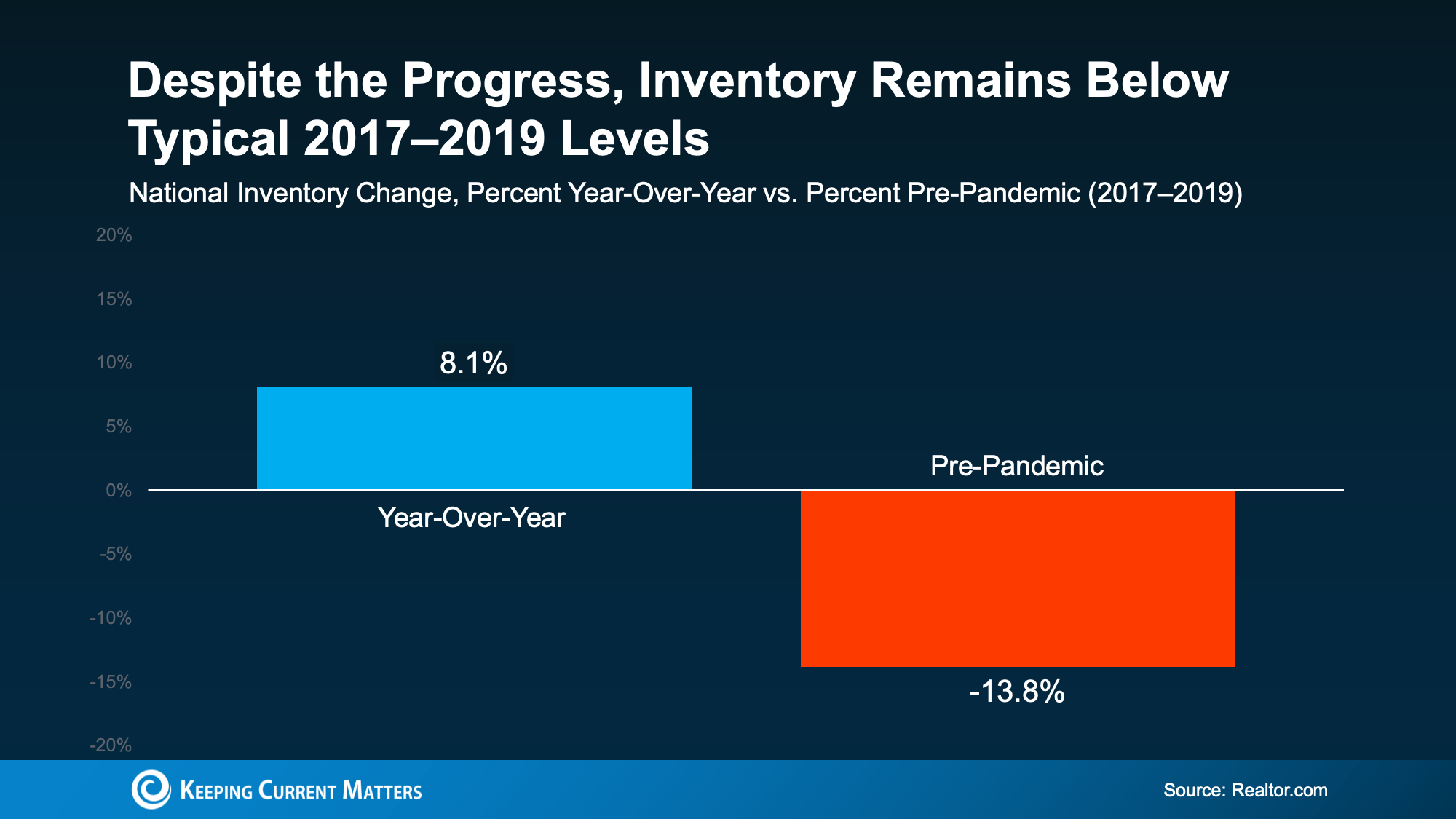

You may have heard that inventory is rising—and nationally, that’s true. The number of homes for sale is up about 8% compared to this time last year. But that’s actually a positive development, giving buyers more options and flexibility.

The issue is how headlines frame the story. They highlight that inventory is at its highest level since 2019 or emphasize new construction, making it seem like supply is surging out of control.

But the bigger picture tells a different story.

Data from Realtor.com shows that while inventory has increased year over year, it’s still nearly 14% lower than typical pre-pandemic levels (2017–2019).

While conditions vary by location, only a small number of states currently have more inventory than they did before the pandemic. That’s a major reason why today’s market doesn’t have the oversupply needed to trigger a crash like in 2008.

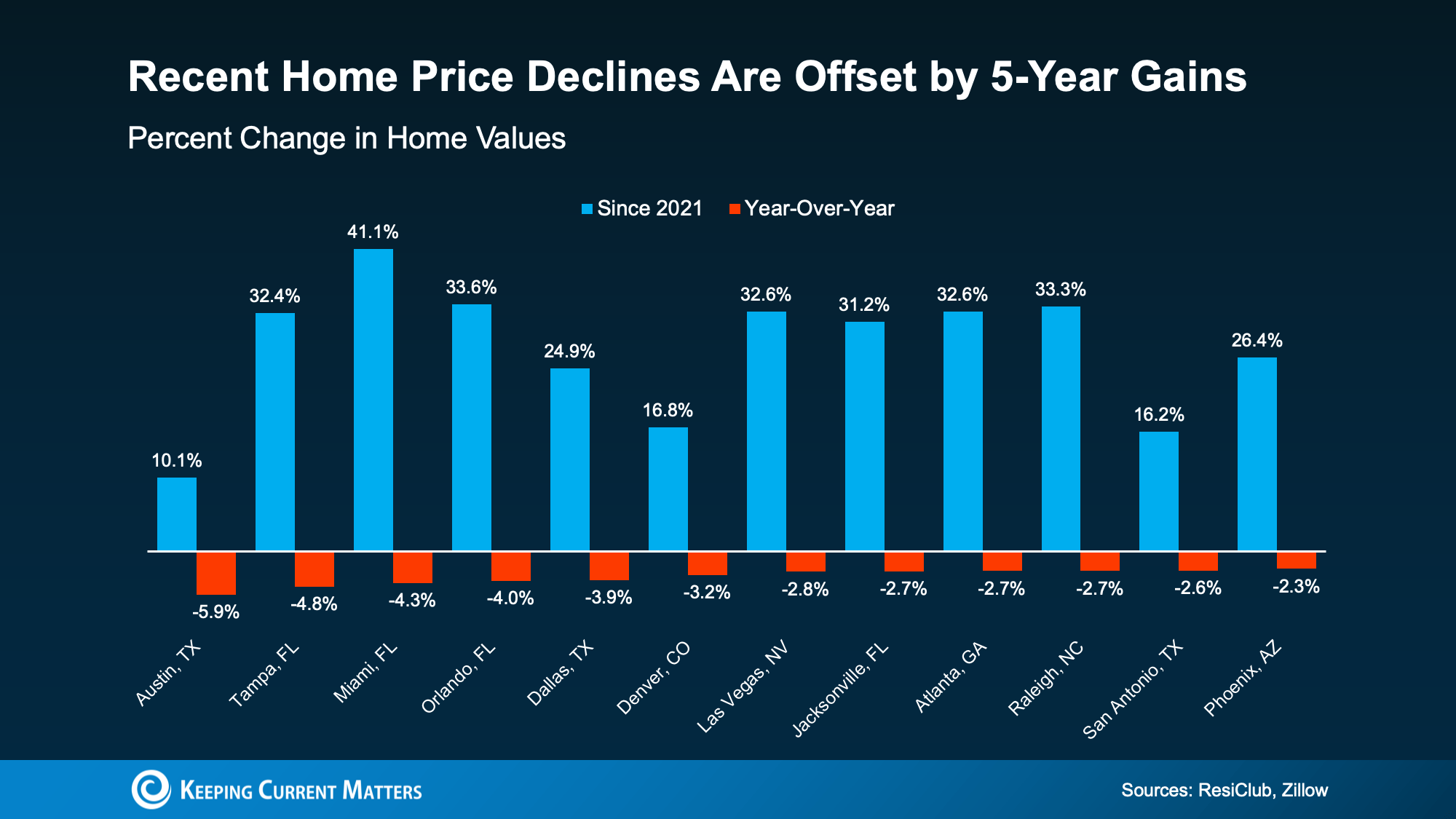

Misconception #3: “Home Prices Are About To Crash”

You’ve likely seen claims that home prices are about to drop sharply. This confusion often comes from certain markets experiencing slight price declines, which are then exaggerated into broader predictions of a crash.

But that’s not what the data shows.

In most areas, home prices are still increasing. And here’s why:

Many homeowners are holding onto their properties because they secured historically low mortgage rates in recent years, limiting new listings.

Inventory remains below pre-pandemic levels, which helps support pricing.

Even in markets with more listings, some sellers are choosing to withdraw their homes rather than reduce prices significantly.

These factors are why a widespread price crash isn’t expected.

Even in areas where prices are softening slightly, the declines are modest and don’t erase the substantial gains homeowners have seen over the past five years.

That’s not a crash—it’s simply the market normalizing after a period of rapid growth.

Bottom Line

Online headlines can often make the situation seem more alarming than it really is. For a clear, data-driven understanding of today’s housing market, it’s best to work with a real estate professional.

Connect with a local agent who can help you separate fact from fiction and guide you with accurate insights.

Rent or Buy? The Real Tradeoff Most People Don’t Talk About

You’ve probably found yourself wondering lately: Is buying a home even worth it right now? It’s a question more and more people are asking.

With current home prices and mortgage rates, renting can feel like the simpler route. In some situations, it might even seem like the only practical choice for now. And if that’s where you are, that’s completely okay.

But if you’re trying to decide, there’s one important part of the conversation that often gets overlooked.

It’s how each option impacts your future.

What Renting Really Offers (And What It Doesn’t)

Depending on your situation, renting does come with some advantages:

Lower upfront expenses.

Less maintenance and responsibility.

Greater flexibility to move when needed.

But even with those perks, a Bank of America survey shows that 70% of future homeowners are concerned about what long-term renting means for their future. And that concern comes down to one key issue: you’re not building anything over time. As Yahoo Finance puts it:

“Paying rent doesn’t build equity. You get a place to live, but no ownership stake, no price appreciation, and no asset to leverage for future borrowing or investment.”

So while renting may feel more convenient, that flexibility often comes at a long-term cost.

How Homeownership Builds Wealth Over Time

On the other hand, owning a home remains one of the most reliable ways to build wealth. Why? Because as a homeowner, you build equity—the difference between your home’s value and what you still owe on it.

That equity grows with every payment you make. It can also increase as property values rise over time—and it adds up faster than many people expect.

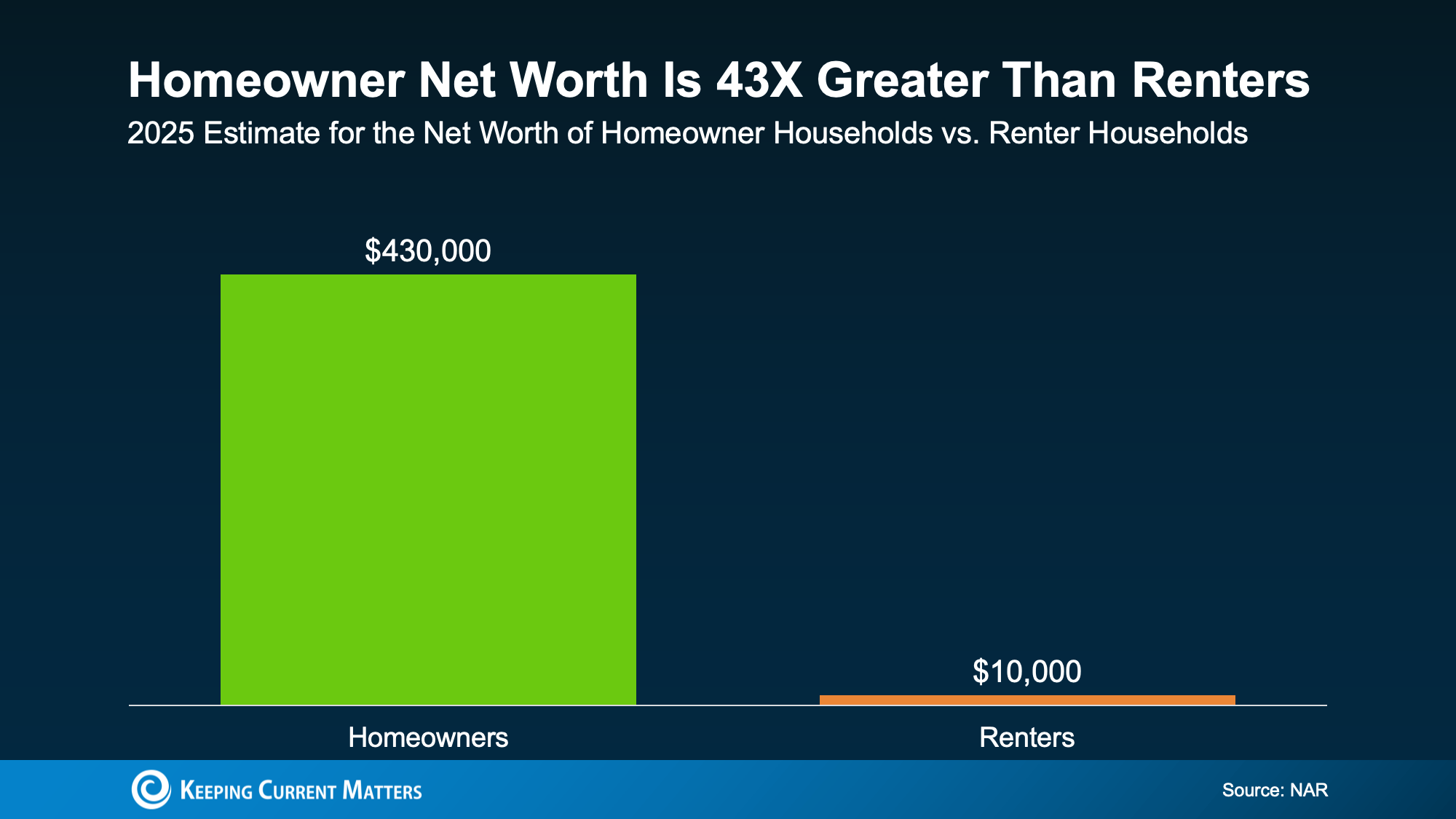

According to the National Association of Realtors (NAR), the average homeowner’s net worth is 43 times higher than that of a renter:

a graph of a number of people

The numbers speak for themselves. On average, here’s how net worth compares:

Homeowners: $430k

Renters: $10k

It’s not because homeowners make drastically different day-to-day choices. It’s because over time, one path builds wealth—and the other doesn’t.

So yes, buying comes with upfront costs and added responsibility. But it also functions like a savings account you live in.

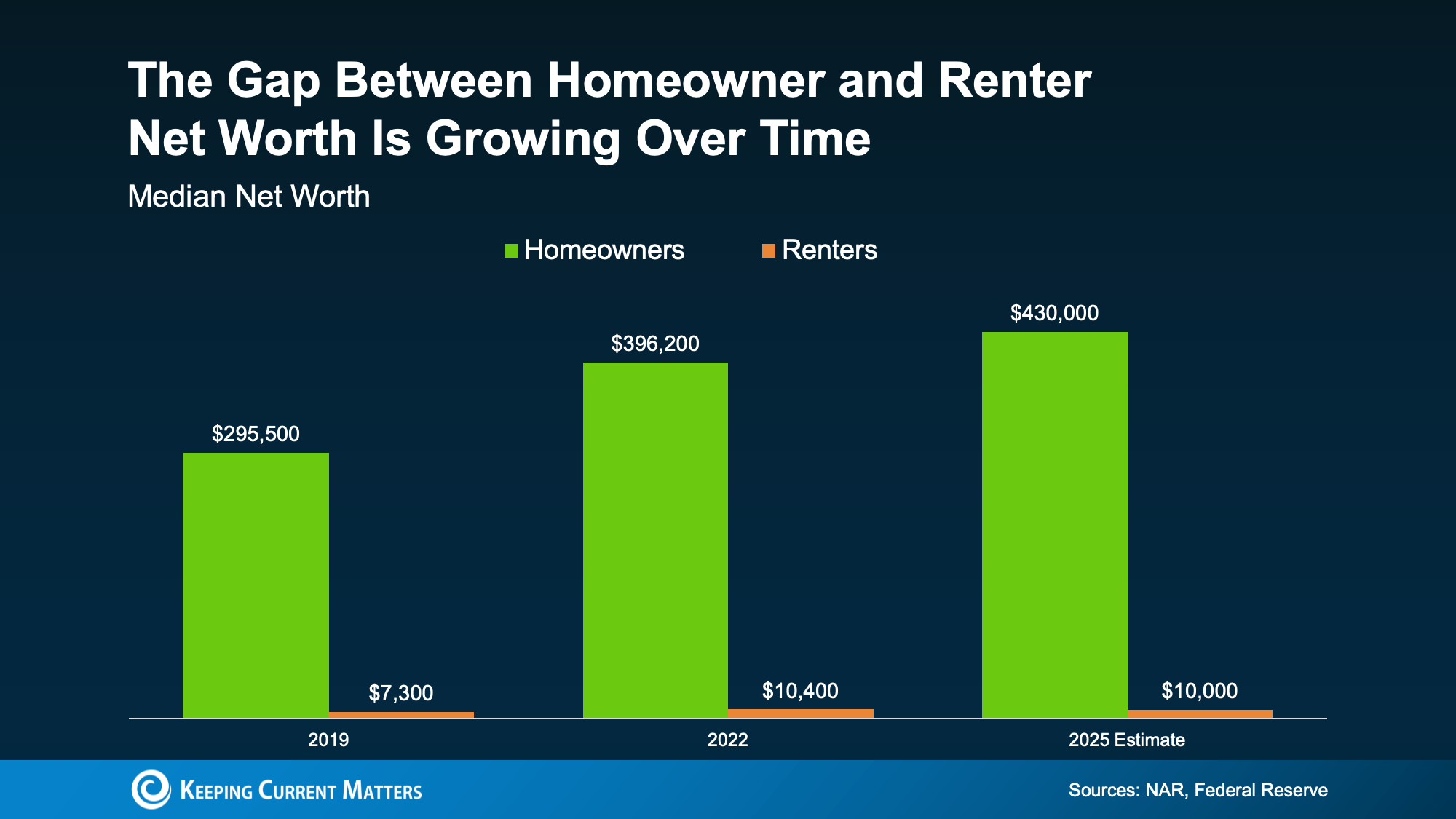

The Gap Continues to Grow

There’s another important point to consider. The net worth gap between homeowners and renters has been increasing over time—not shrinking.

Looking at historical data, the gap keeps widening as homeowners continue building wealth while renters remain in place (see graph below):

a graph of green and blue bars

Even in 2025, when home price growth slowed, homeowners still gained ground. And that highlights something important:

When you’re financially ready and able to take on the responsibility, history shows that buying is typically worth it in the long run. Because either way, you’re contributing to a mortgage—just not always your own.

When you rent, you’re paying your landlord’s mortgage. When you own, your payments build your own equity.

So the real question becomes: whose investment do you want to support—yours or someone else’s?

So, Should You Buy a Home Now?

The honest answer is: it depends on your situation.

While the long-term advantages of homeownership are clear, that doesn’t mean it’s the right time for everyone. And that’s perfectly fine. You should only buy when you’re financially ready and comfortable with the commitment.

Whether you’re ready now or planning ahead, the first step is the same. Have a quick conversation with a local real estate agent about your goals, timeline, and budget.

They can help you break down the numbers and see what’s possible. You might find that buying is more within reach than you expected. And if not, you’ll walk away with a clear plan to get there.

Because having a plan puts you in control—instead of constantly wondering if or when it will happen.

Bottom Line

Renting may feel more manageable today—but over time, it could cost you.

If your goal is to move beyond renting and start building for your future, it begins with a simple conversation. Connect with a real estate agent to discuss your goals and explore your options—so you’re ready when the timing is right.

Thinking About an Adjustable-Rate Mortgage? Here’s What You Need To Know.

If you’ve been searching for a home recently, you’ve probably noticed how challenging affordability still is. That’s exactly why more buyers are turning to adjustable-rate mortgages, or ARMs.

Here’s what you should know about how they work—and whether they might be right for you.

What Is an Adjustable-Rate Mortgage?

Since many people aren’t as familiar with this type of loan, let’s start with a simple explanation. Here’s how Business Insider describes the key difference between a fixed-rate mortgage and an adjustable-rate mortgage:

“With a fixed-rate mortgage, your interest rate stays the same for the entire life of the loan, keeping your monthly payment consistent over time . . . adjustable-rate mortgages work differently. You begin with a set rate for a few years, but after that, your rate can change at regular intervals. This means your payment could go up if rates rise, or go down if rates fall.”

In short, one remains stable over time.

And the other can fluctuate—sometimes slightly, sometimes significantly.

Of course, factors like taxes or homeowner’s insurance can still impact a fixed-rate loan. But overall, the base mortgage payment tends to stay consistent. With an ARM, however, your monthly payment can change as rates adjust.

Why Adjustable-Rate Mortgages Are Getting More Attention

So why are more buyers considering this option? It comes down to upfront savings. Business Insider explains:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers improve affordability when rates are high. A lower ARM rate can mean a smaller monthly payment or the ability to afford a more expensive home compared to a fixed-rate loan.”

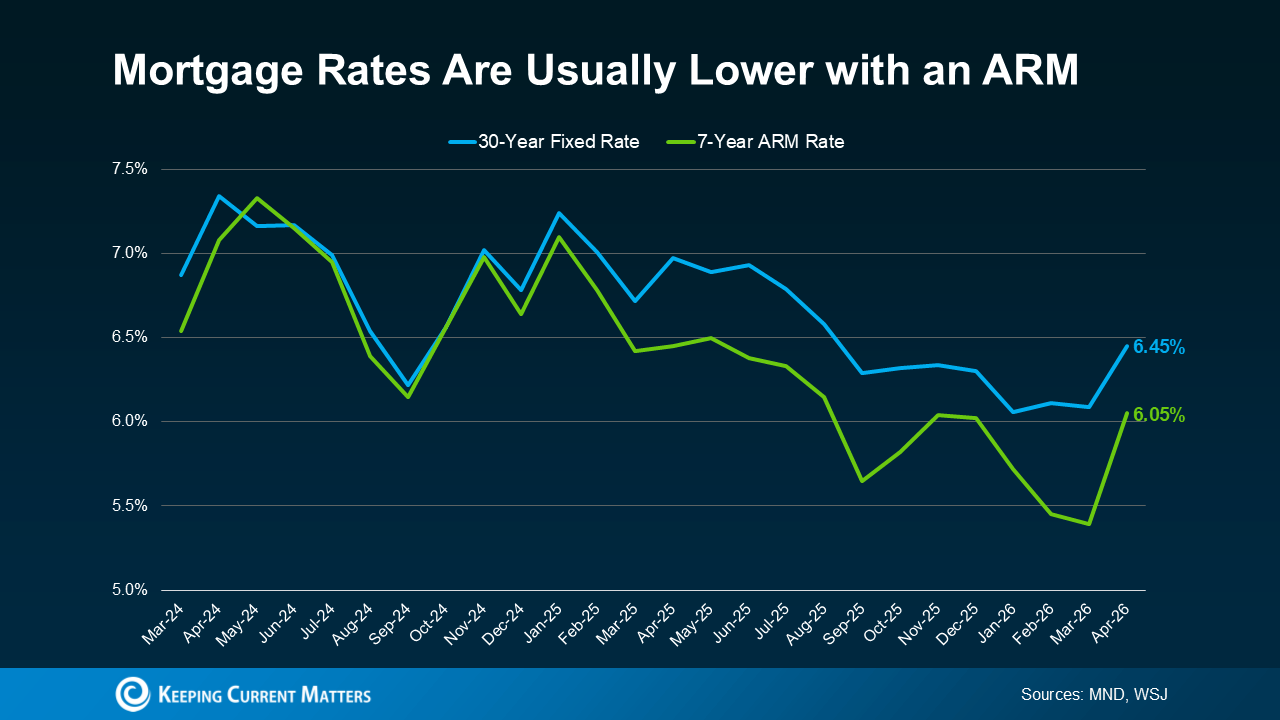

Right now, based on data from Mortgage News Daily and the Wall Street Journal, initial ARM rates are lower than those for a 30-year fixed mortgage.

If you’re wondering what that looks like in real numbers, Redfin reports that the average buyer could save about $150 per month by choosing an ARM over a 30-year fixed loan.

For many, that difference can be meaningful.

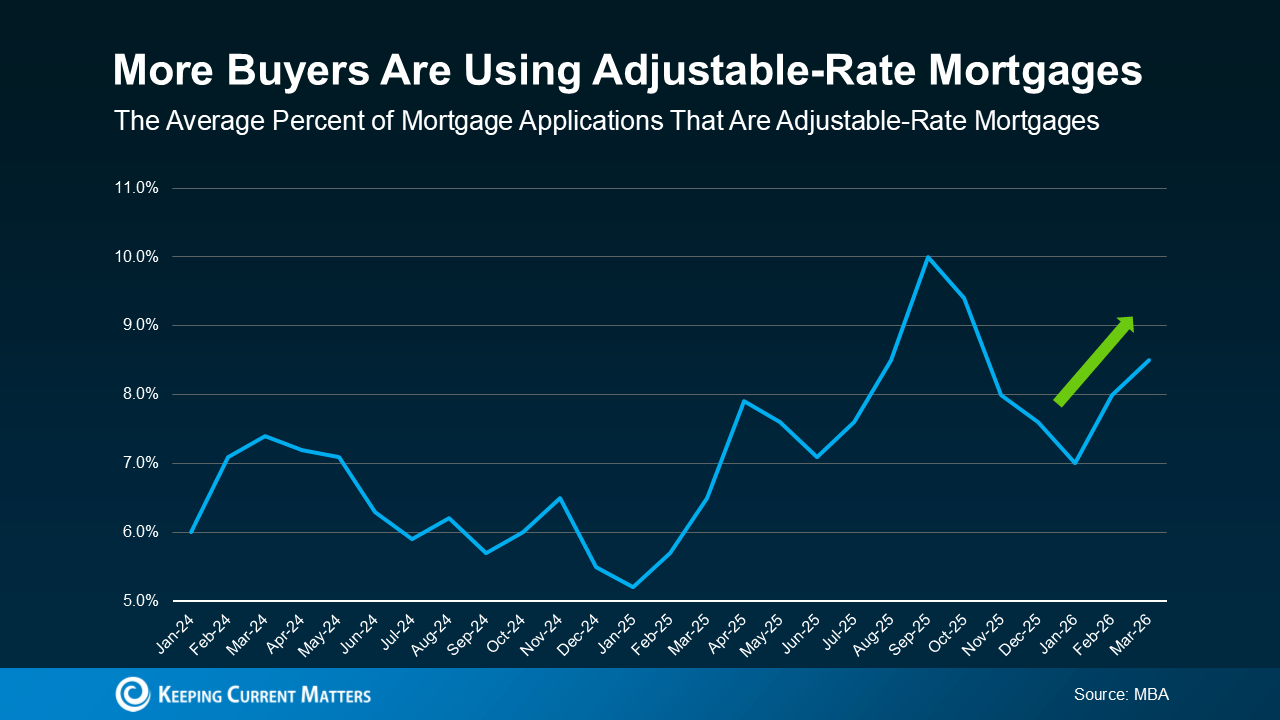

More Buyers Are Choosing Adjustable-Rate Mortgages Today

An increasing number of buyers are willing to accept some future uncertainty in exchange for lower payments today. Data from the Mortgage Bankers Association (MBA) shows that the share of buyers choosing ARMs has risen, particularly in recent years.

That doesn’t mean ARMs are becoming the default choice—it simply shows that some buyers are using them as a strategy to make homeownership more attainable right now.

If you remember the housing crash, this trend might sound concerning. But today’s ARMs are very different.

In the past, some borrowers were approved for loans they couldn’t afford once rates adjusted.

Now, lending standards are much stricter. Lenders assess whether borrowers can still manage payments if rates increase. So, the renewed interest in ARMs doesn’t signal another crisis—it reflects how buyers are adapting to today’s affordability pressures.

The Trade-Off – What You Need To Consider

If you’re thinking about an adjustable-rate mortgage, it ultimately comes down to your personal situation and comfort with risk.

An ARM might make sense if you plan to move before the rate adjusts, or if you expect your income to increase over time. Still, there are important trade-offs to consider.

Once the fixed-rate period ends, your rate can change—and your monthly payment could rise, potentially by a significant amount depending on market conditions.

Also, there’s no guarantee that mortgage rates will drop in the future, which means refinancing may not always be an option. That’s why it’s essential to have a clear plan, understand your long-term financial outlook, and work closely with a trusted lender before choosing this type of loan.

Bottom Line

ARMs are gaining attention again because they can offer lower payments upfront, making homeownership more accessible in the short term. But they aren’t the right fit for everyone.

The key is understanding how they work, weighing the risks, and deciding whether they align with your financial goals. That’s why it’s important to consult with a trusted lender and financial advisor before making any decisions.

You Can’t Control What’s Happening with Mortgage Rates. But You Can Control This.

Mortgage rates have been fluctuating lately, and if you’re thinking about buying a home, that can make planning feel more challenging. The good news? There are still steps you can take to secure the best rate possible in today’s market—it all starts with understanding what’s going on.

So, what’s behind the recent rate swings? And what can you do about it? Let’s break it down.

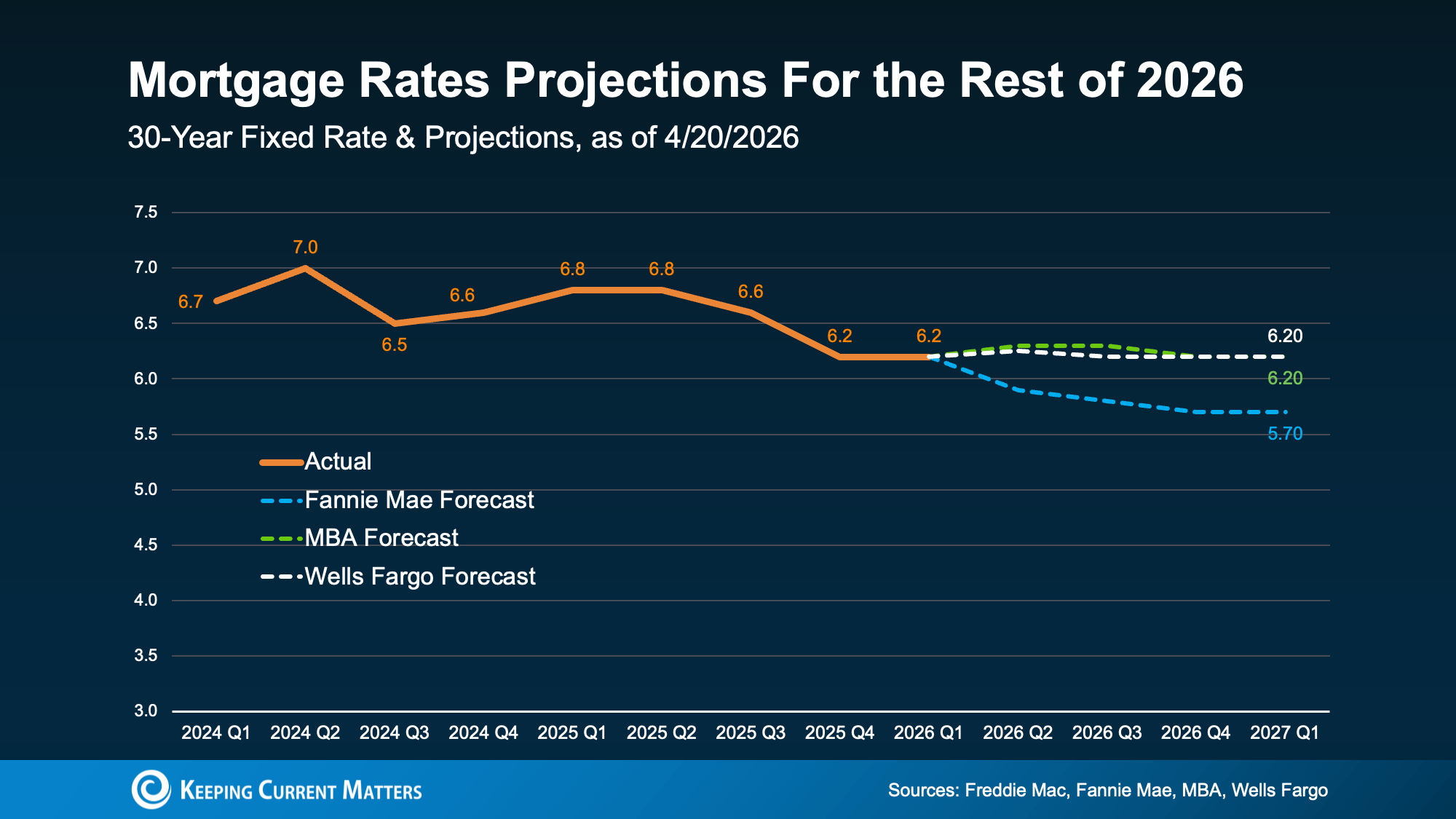

Mortgage Rate Volatility Is Normal

Recent data from Freddie Mac highlights the ups and downs. After steadily declining for over a year, rates have ticked up this month (see graph below):

a graph showing a line of a moving rate

While it’s easy to focus on short-term changes, here’s what really matters.

It’s completely normal for mortgage rates to move up and down from time to time. Looking back over the past year, there have been several moments when rates briefly increased. We’re simply in one of those periods again—and it’s important to recognize that.

Periods of economic uncertainty or major global events often contribute to this kind of movement. As Investopedia explains:

“Mortgage rates don’t move in isolation. When global events create uncertainty in financial markets, it can impact borrowing costs… mortgage rates can shift quickly in response to geopolitical developments. As long as uncertainty stays elevated, rate fluctuations are likely to continue.”

That’s why trying to perfectly time the market usually isn’t the best strategy.

While you can’t control where mortgage rates go, you can control several key factors that influence the rate you’re offered. Here’s where to focus:

Your Credit Score

Your credit score is a major factor in determining your mortgage rate. Even a slight improvement can lead to meaningful savings on your monthly payment. As Bankrate notes:

“Your credit score is one of the most important factors lenders evaluate—not just for loan approval, but for the terms. Generally, higher scores qualify for lower interest rates and better conditions.”

Be proactive about maintaining or improving your credit. If you’re unsure where you stand, a trusted loan officer can help guide you.

Your Loan Type

There are several types of home loans, each with its own requirements, benefits, and interest rates. The Consumer Financial Protection Bureau (CFPB) explains:

“Common mortgage categories include conventional, FHA, USDA, and VA loans. Each comes with different eligibility criteria, and rates can vary significantly depending on the loan type.”

This is why it’s so important to review your options with a lender—and even compare offers from multiple lenders.

Your Loan Term

The length of your loan also plays a key role. Most lenders offer 15-, 20-, or 30-year terms. According to Freddie Mac:

“When selecting a home loan, consider the loan term—the time it will take to repay the loan in full. The term impacts your interest rate, monthly payment, and the total interest paid over time.”

To find the best fit for your financial goals, have a lender walk you through how each option affects your budget.

Bottom Line

If you’re thinking about buying a home right now, the key is to accept that mortgage rates are out of your control.

What you can control is how prepared you are. By working with a trusted lender and focusing on the factors that influence your rate, you can put yourself in the best possible position.

When you’re ready to make a move, connect with a real estate agent and a lender. Stay focused on what you can control—and that’s where you’ll see the biggest impact.

3 Must-Do’s for First-Time Home Buyers

Buying Your First Home Doesn’t Have to Feel Overwhelming

Buying your first home is exciting—but it can also feel overwhelming since it’s something new. Keeping track of everything may seem like a lot at first. But here’s the good news:

You don’t have to figure it all out on your own, and you don’t have to do everything at once. Take it one step at a time.

Here are three key areas to focus on to help you get started:

1. Assemble Your Team: Don’t Do This Alone

Buying a home works best when you have the right team supporting you. The right professionals can guide you and help you avoid costly mistakes.

A local real estate agent will guide you from your first showing to closing day. They explain each step clearly so you can make confident decisions.

A trusted lender will walk you through your loan options, estimate your monthly payments, and help you understand what fits your budget. Getting this information early gives you a strong advantage.

2. Prep Your Finances: Build a Strong Foundation

Your financial preparation shapes what you can afford, how competitive your offer will be, and how confident you feel during the process.

Start by checking your credit score. Your score affects your loan options and interest rate, so reviewing it early gives you time to improve it if needed.

Save for both your down payment and closing costs. Many buyers focus only on the down payment, but closing costs matter just as much. Preparing for both helps you avoid last-minute stress.

Explore assistance programs available to first-time buyers. These programs can boost your savings and make homeownership more achievable.

Talk to a lender about your mortgage options. Fixed-rate, adjustable-rate, FHA, VA, and conventional loans all offer different benefits. Understanding them helps you choose what works best for your goals.

Get pre-approved. This step shows how much a lender is willing to lend you, helps define your budget, and allows you to act quickly when you find the right home.

Create a realistic budget. Include not just your mortgage, but also utilities, insurance, maintenance, and daily expenses. This helps keep your finances comfortable—not stressful.

3. Gather Your Documents: Save Time and Reduce Stress

When you’re ready to move forward, lenders will review your financial history. Preparing your documents early helps speed up the process and prevents delays.

Gather your W-2s and tax returns from the past two years to show income consistency.

Collect recent pay stubs from the past 1–2 months to confirm your current income.

Prepare bank statements from the past 2–3 months to show your savings and spending habits.

Include investment account statements if they apply to your financial situation.

Provide a copy of your driver’s license to verify your identity.

List your residential history from the past two years to show stability.

Gather statements for any outstanding debts, such as credit cards, student loans, or car loans.

Include proof of additional income like bonuses, commissions, or side work if applicable.

Note: Requirements may vary depending on the lender, but this list gives you a solid starting point.

Bottom Line

You don’t need to have everything figured out to buy your first home—you just need a clear plan.

When you prepare your finances, organize your documents, and build the right team, you set yourself up for success.

If you want more guidance or need help getting started, reach out to a trusted real estate professional.

The #1 Reason Buyers Walk Away (And How To Get Ahead of It)

You may have seen headlines on social media saying the number of buyers backing out of home contracts is rising, reaching levels not seen since 2017. While that might sound concerning, the reality is that this trend can vary greatly depending on the local market.

More importantly, there is often one main reason deals fall apart — and it is something sellers can actually prepare for and manage.

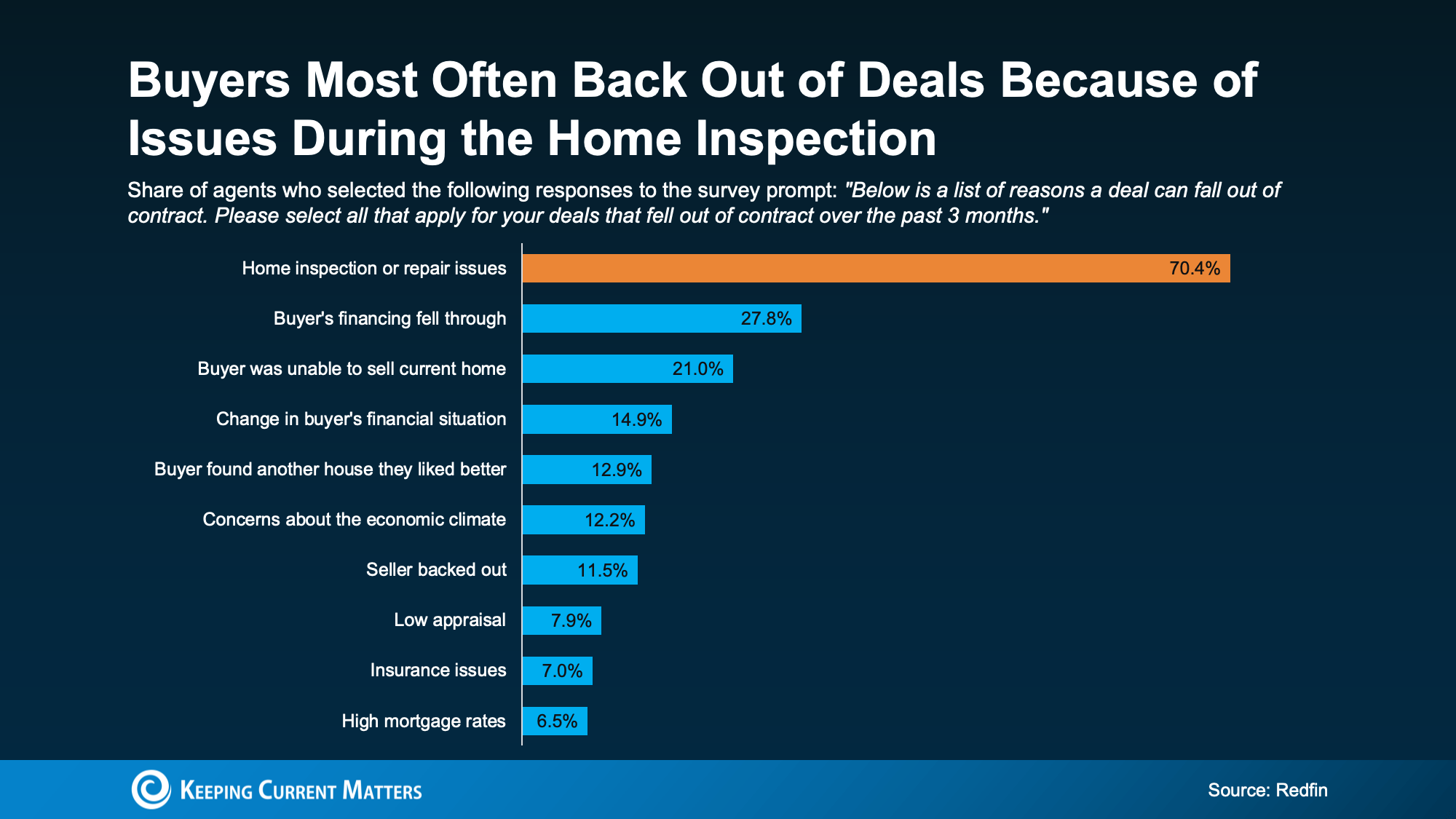

The Biggest Dealbreaker: Home Inspection Issues

According to a survey from Redfin, more than 70 percent of recently cancelled contracts happened because problems were uncovered during the home inspection. This makes sense in today’s market. Buyers now have something they did not have a few years ago — more options.

This makes sense in today’s market. Buyers now have something they did not have a few years ago — more options.

Why Repairs Matter More in Today’s Market

During the peak of the competitive market, buyers often overlooked certain issues because there were so few homes available. Many felt pressured to move quickly.

Today, that dynamic has shifted.

With more inventory on the market, buyers can afford to be selective. If a home feels like it may come with costly repairs, hidden issues, or potential risks, many buyers will simply move on to another property.

This is why addressing key maintenance items before listing your home can make a significant difference.

How a Real Estate Agent Can Help

A knowledgeable local agent can walk through your home and help identify which repairs or improvements may be worth addressing before you list. Their experience in the local market can help you prioritize the updates that matter most to buyers.

According to Zillow, some of the issues buyers pay the closest attention to include:

-

Roof damage or leaks

-

Plumbing problems such as leaks or water damage

-

Electrical concerns like outdated wiring or missing GFCI outlets

-

HVAC systems that are not functioning properly

-

Pest or insect damage, including termites

-

Hazardous materials such as mold, lead, or asbestos

-

Safety or code violations

-

Structural concerns like foundation cracks or sagging floors

Of course, not all of these issues apply to every home. In some cases, there may only be one or two items to address — or none at all. The key is knowing what buyers in your market are most likely to notice.

The Value of a Pre-Listing Inspection

For buyers, inspection findings are not just about repairs — they are about trust. Once buyers start wondering what other problems might be hiding behind the walls, it can be difficult to regain their confidence.

This is why some agents recommend a pre-listing inspection. It allows sellers to see potential concerns before a buyer does.

With that information, you can:

-

Make necessary repairs before listing

-

Disclose issues upfront

-

Avoid last-minute negotiations under pressure

-

Plan repairs without rushing before closing

That said, you do not need to fix every single item. The goal is to focus on the issues that are most likely to impact the sale.

A trusted agent can help you decide:

-

Whether a pre-listing inspection makes sense in your market

-

Which inspector to work with

-

What repairs are worth making

-

When offering a credit might make more sense than completing repairs

Bottom Line

Inspection issues are one of the most common reasons home sales fall through — but the good news is that many of these problems can be addressed before your home even hits the market.

Being proactive with key repairs can help build buyer confidence and keep your sale moving forward.

If you want guidance on where to focus before listing your home, connecting with a knowledgeable agent can make all the difference.

{kind=link}