Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Home Staging Tips That Actually Help Sell Your Property Faster

First impressions matter in real estate. In fact, most buyers now start their search online, long before they ever step through the front door. That means your listing photos often decide whether a buyer books a showing at all. Staging is how you win that first impression.

Does Staging Really Work?

Yes, and the data backs it up. According to the National Association of Realtors’ 2025 Profile of Home Staging, about half of agents say today’s buyers expect homes to look like they belong on a design show. So, staging isn’t just a nice extra touch anymore. It’s becoming an expectation.

The report also found that 29% of agents saw a 1% to 10% increase in the dollar value of offers on staged homes. Meanwhile, nearly half of sellers’ agents said staging reduced the time a home spent on the market. In short, staging can help you sell faster and for more money.

Where to Focus Your Effort

You don’t need to stage the entire house. In fact, professional stagers often recommend focusing on just a few key rooms to save money. According to NAR, buyers rank these rooms as most important:

- Living room – ranked most important by 37% of buyers

- Primary bedroom – ranked most important by 34% of buyers

- Kitchen – ranked most important by 23% of buyers

So, if your budget is tight, start here. These are the spaces that shape a buyer’s first impression the most.

Staging Tips That Make a Real Difference

1. Declutter first, always. Before you touch paint or furniture, clear out anything unnecessary. A tidy, open space photographs better and helps buyers picture their own belongings there.

2. Depersonalize the space. Family photos and personal collections feel homey to you, but they can distract buyers. Instead, aim for a neutral backdrop buyers can imagine themselves living in.

3. Let in natural light. Open the blinds, clean the windows, and swap out dim bulbs. Bright rooms consistently photograph and show better than dark ones.

4. Rearrange furniture to show flow. Buyers want to picture how they’d move through a space. So, pull furniture away from walls and create clear pathways between rooms.

5. Add a few warm, neutral touches. A little greenery, fresh towels, or a bowl of fruit on the counter can go a long way. Just don’t overdo it. The goal is warmth, not clutter.

6. Fix the small stuff. Chipped paint, leaky faucets, and squeaky doors are easy to overlook. However, buyers notice, and small flaws can raise doubts about bigger, unseen problems.

7. Don’t forget curb appeal. The exterior is the first thing buyers see, whether in person or in photos. A trimmed lawn, a fresh coat of paint on the front door, and clean walkways set the tone before anyone walks inside.

What Staging Costs

Staging costs vary a lot depending on your market and how much of the home you stage. According to recent industry data, a full staging consultation alone often runs $150 to $300, while professional full-home staging can run into the thousands, especially in higher-priced markets. That said, a consultation is usually the highest-value option for budget-conscious sellers, since it gives you a room-by-room plan you can carry out yourself.

The Bottom Line

Staging isn’t about chasing design trends. Instead, it’s about helping buyers picture themselves living in your home. Even a modest budget, spent in the right rooms, can shorten your time on market and strengthen your offers. So before your next listing goes live, take a hard look at your space through a buyer’s eyes.

Curious how staging costs stack up against what you’ll actually walk away with? Try my Seller Net Proceeds Calculator to see your estimated bottom line before you decide how much to invest in prepping your home.

Thinking about listing your home soon? Reach out — I can walk you through what buyers in your area are looking for, room by room. You can also learn more about my background and read client reviews on my Homes.com profile.

A Beginner’s Guide to Real Estate Investing

So you’ve been thinking about real estate investing. Maybe you’ve watched one too many home-flipping shows. Or maybe a friend told you about a rental property that’s paying their mortgage for them. Either way, you’re curious. And that’s a great first step.

Real estate investing isn’t just for the wealthy. With the right knowledge and a realistic plan, almost anyone can get started. Here’s what you need to know.

Why Invest in Real Estate?

Unlike stocks, real estate is a tangible asset. You can see it, touch it, and improve it. It also offers a few unique advantages:

- Cash flow. Rental income can provide steady monthly earnings.

- Appreciation. Property values tend to rise over time. However, this isn’t guaranteed.

- Leverage. You can control a large asset with a small down payment.

- Tax benefits. Deductions on mortgage interest, depreciation, and expenses can add up.

- Diversification. It’s a way to spread your money beyond the stock market.

Common Ways to Get Started

1. Rental Properties

Buy a property and rent it out to tenants. This is the classic path. It offers steady income, but it also means hands-on management. Or, you can hire a property manager to handle it for you.

2. House Hacking

Buy a multi-unit property. Live in one unit, and rent out the others. This is a popular strategy for first-time investors. Why? Because it can significantly reduce your own housing costs.

3. Fix-and-Flip

Buy an undervalued property, fix it up, and sell it for a profit. This path requires more capital and strong contractor relationships. It also demands a higher tolerance for risk. In exchange, it can generate quicker returns.

4. REITs (Real Estate Investment Trusts)

Don’t want to deal with tenants or toilets? REITs let you invest in real estate through the stock market. That means you get exposure to real estate without the hands-on responsibilities.

5. Real Estate Crowdfunding

Some platforms let investors pool their money into larger projects. This means you can invest in commercial or residential real estate with a relatively low minimum.

What to Know Before You Buy

Location matters more than the property itself. For example, a modest home in a growing area will often outperform a beautiful house in a declining one.

Run the numbers before you fall in love. First, calculate your expected rental income. Then subtract the mortgage, taxes, insurance, maintenance, and vacancy costs. If the numbers don’t work, walk away. This holds true no matter how charming the property is.

Financing isn’t one-size-fits-all. Investment properties often require larger down payments and carry higher interest rates than a primary residence. So, shop around early and understand your options.

Build a team. A good real estate agent, lender, inspector, and property manager can save you from costly mistakes. In short, you don’t have to do this alone.

Start small. Your first investment doesn’t need to be your last. In fact, many successful investors began with a single rental or a house hack. Only later did they scale up.

Mistakes Beginners Often Make

- Underestimating repair and maintenance costs

- Overpaying because of emotional attachment

- Skipping the property inspection

- Not accounting for vacancy periods

- Trying to do everything alone instead of building a network

The Bottom Line

Real estate investing rewards patience and research. It also rewards a willingness to learn from mistakes, including other people’s. You don’t need to buy your first property tomorrow. Instead, start by learning your local market. Talk to investors and agents in your area. Then get clear on your financial goals.

After all, the best time to start learning was yesterday. The second-best time is now.

Thinking about investing in your area? Reach out. I’d be happy to walk you through what’s happening in the local market and help you figure out if now is the right time for you.

Student Loans Are Back in the News. Don’t Let It Put Your Homeownership Plans on Hold.

Student loans are back in the spotlight, and whether you’ve been keeping up with the latest news or only hearing the occasional update, there’s a good chance they’ve been on your mind recently.

And if you’re wondering whether you have to hit pause on your plans to buy a home, here’s the one thing you need to remember:

Having student loans doesn’t automatically mean buying a home has to wait.

The Biggest Myth About Student Loans and Buying a Home

One of the most common misconceptions among first-time buyers is that they have to pay off their student loans before they can qualify for a mortgage. But in most cases, that’s just not true.

As an article from Redfin explains, student loans usually get evaluated the same way other debts do, like credit cards or car payments:

“Yes, you can get a mortgage with student loan debt. Lenders primarily assess your debt-to-income (DTI) ratio, which compares your monthly debt payments, including student loans, to your gross monthly income. Having student debt doesn’t automatically disqualify you if your DTI is within acceptable limits.”

That means seeing student loans on your credit report isn’t an automatic dealbreaker.

Instead, lenders evaluate your complete financial picture, including your income, credit score, employment history, savings, and existing debts. Student loans are just one factor they consider, not the deciding factor.

You’re in Better Company Than You Think

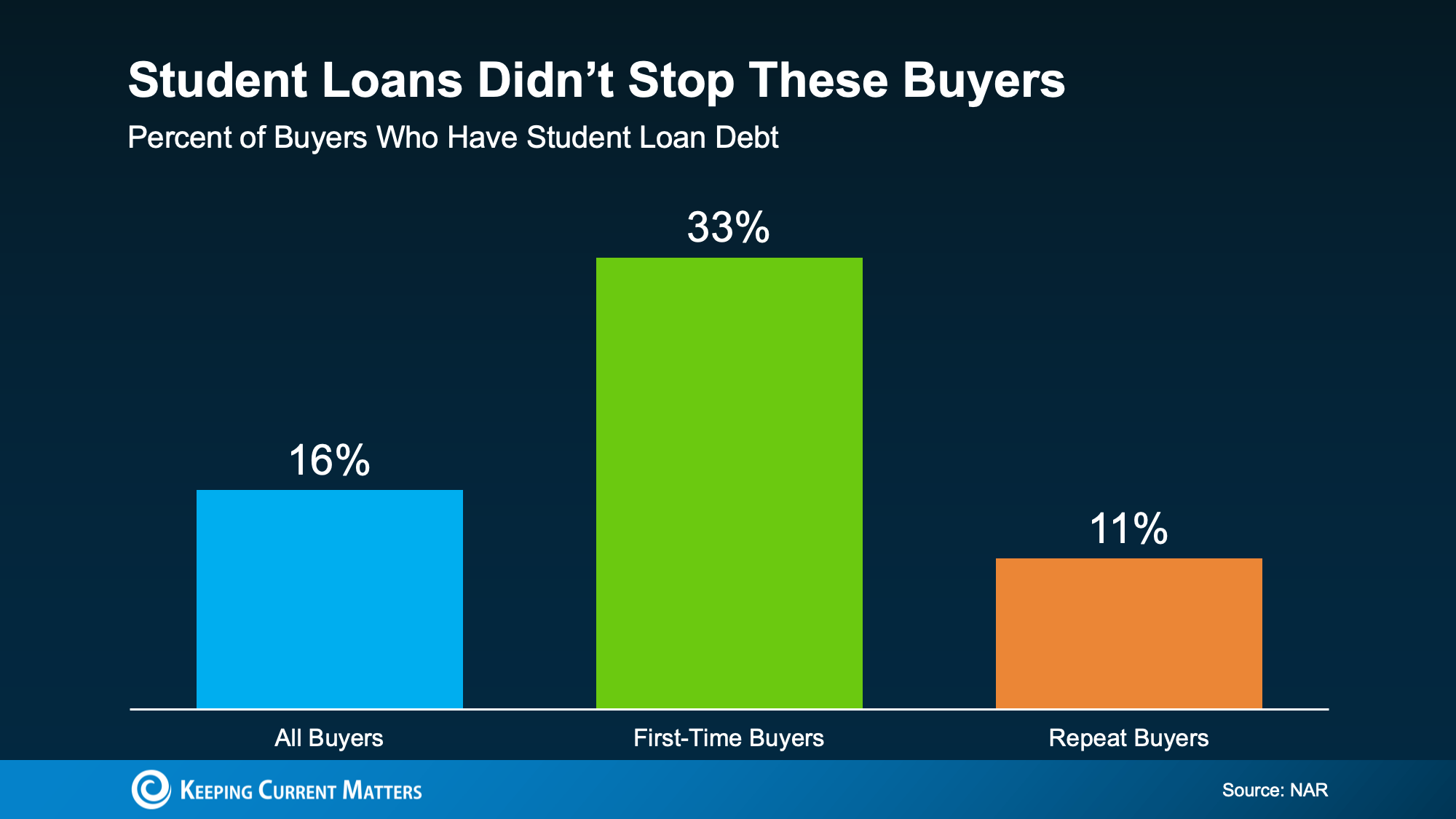

Just to really drive this home, here’s a stat from the National Association of Realtors (NAR) that proves you can have student debt and still buy a home. Their research shows 33% of first-time homebuyers still had student loan debt.

That’s 1 out of every 3 first-time buyers. The median amount they owed? $30,400.

Every day, people with student loans successfully buy homes. Having student debt doesn’t automatically mean homeownership is out of reach.

Don’t Count Yourself Out Before You Even Try

One of the biggest mistakes many buyers make is assuming they won’t qualify for a mortgage without ever exploring their options. The truth is, every financial situation is different, and student loans are just one piece of the puzzle.

If you have a steady income and your overall finances are in good shape, buying a home may be more achievable than you realize. The best way to find out is to speak with a trusted lender who can review your finances and help you understand what you qualify for.

You might be surprised to learn you’re closer to homeownership than you think.

Bottom Line

Student loans don’t have to stand between you and owning a home. If you’ve been putting your homebuying plans on hold because of student debt, now is a great time to explore your options. A conversation with a lender could show you that buying a home is more within reach than you expected.

Is It Still a Seller’s Market? Here’s What the Data Says.

Saving for a down payment can often feel like the biggest obstacle to buying a home. With affordability still a challenge in many markets, it’s easy to wonder how buyers are making homeownership happen.

The good news is that many are getting into the market with smaller down payments than you might expect.

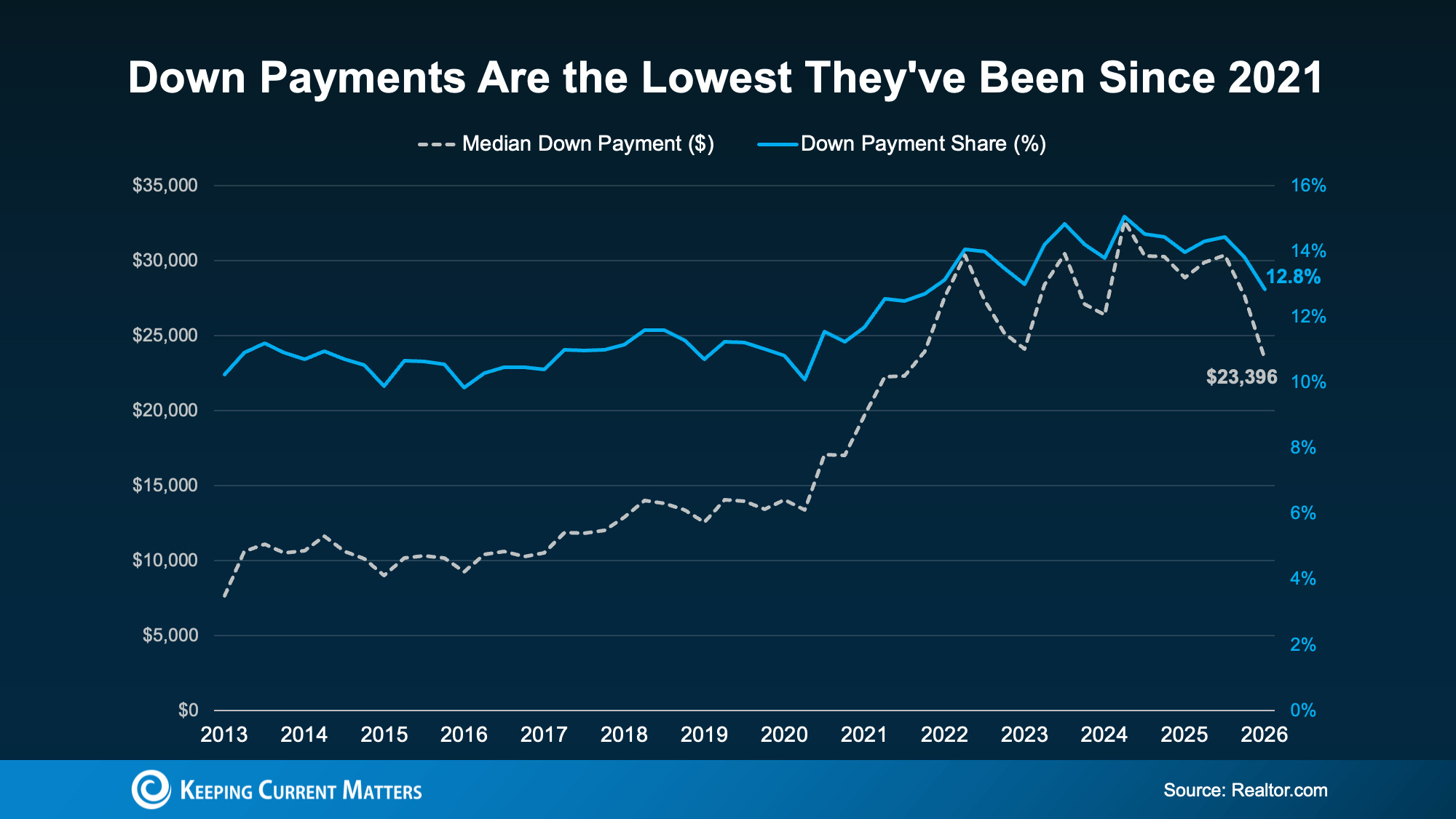

According to Realtor.com, the typical homebuyer put down about $23,400 in early 2026. That’s roughly $5,000 less than the average down payment a year earlier, representing a 19% year over year decrease. In fact, it’s the lowest typical down payment seen since 2021 (see graph below).

So why are buyers putting less money down, and how can you put less down, too? Here’s your answer.

Why Down Payments Are Getting Smaller

Several factors are contributing to this trend:

A More Balanced Housing Market

As the market becomes more balanced, buyers are facing less competition than they did a few years ago. That means there’s less pressure to make a larger down payment just to strengthen an offer.

Slower Home Price Growth

Since your down payment is based on a percentage of the home’s purchase price, slowed price appreciation can reduce the amount you need upfront. In many markets, home prices have stabilized, and some have even seen slight declines, making smaller down payments more achievable.

More Buyers Choosing Low Down Payment Loan Programs

Many homebuyers are taking advantage of government-backed loan options, such as FHA and VA loans, which often require little or even no money down. According to Mortgage Professional America, FHA loans have accounted for more than 24% of purchase mortgages for five consecutive quarters, while VA loans recently reached their highest market share in over a decade.

Even so, a down payment is still a significant expense, and saving for it isn’t always easy. That’s why many buyers rely on down payment assistance programs or financial support from family members to help bridge the gap.

Help You May Not Know You Qualify For

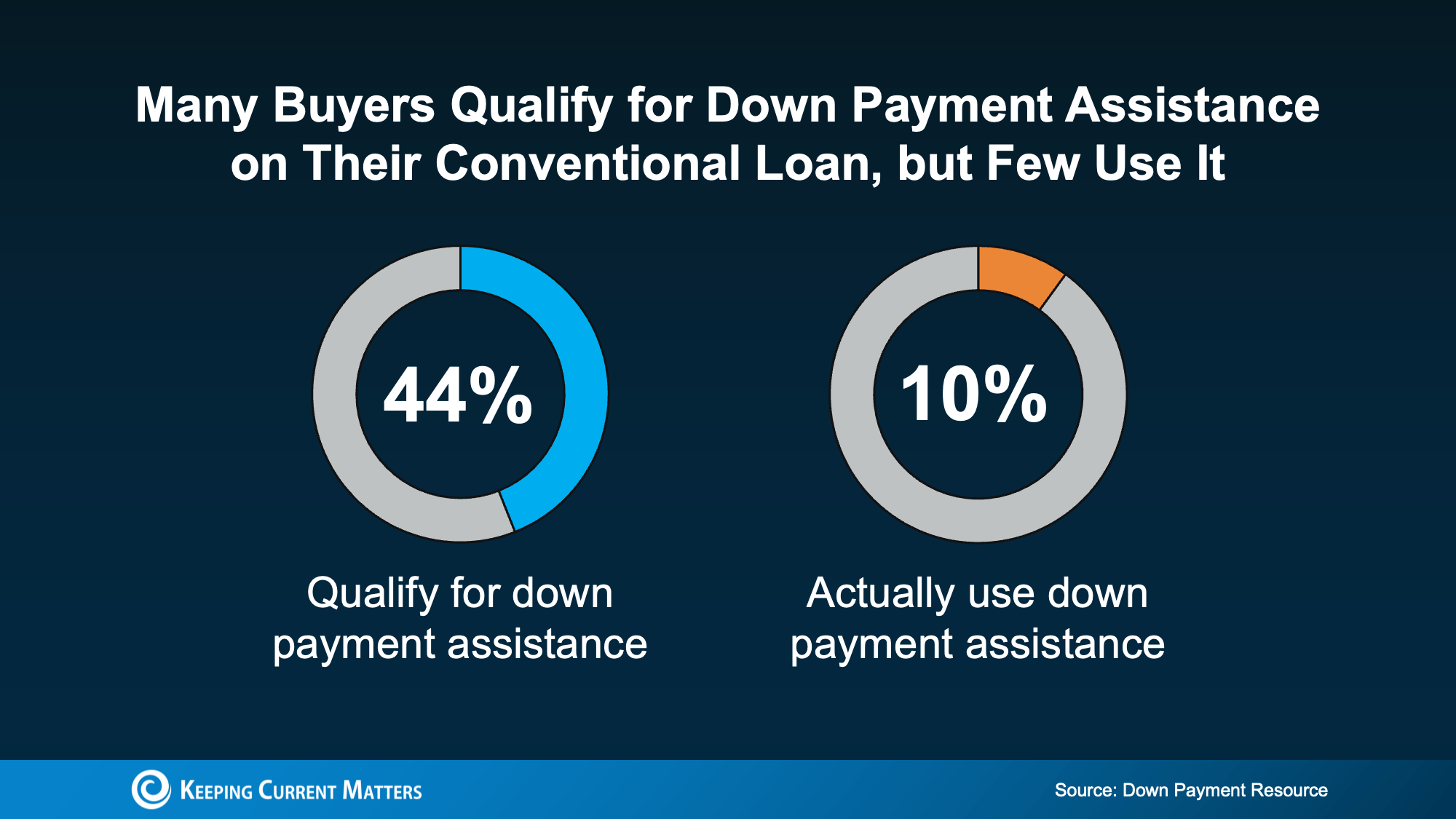

Down payment assistance is one of the most overlooked tools out there. Looking at the 10 largest U.S. metros, Urban Institute and Down Payment Resource found nearly 44% of recent buyers already qualified for a down payment program, but many of them closed on their loan without tapping the help (see chart below):

The options are broader than you might assume, too. According to Down Payment Resource:

- There are more than 2,600 down payment assistance programs available

- More than half (62%) are designed to help first-time buyers

- 38% have no first-time buyer requirement, so you may qualify even if you’ve owned before

- 62% are open to buyers earning $100,000 or more

A Helping Hand from Family

For many homebuyers, financial support starts with family. According to Veterans United, about 59% of parents have either helped or plan to help their children purchase a home.

That assistance most often goes toward the down payment, but it can also help with qualifying for a mortgage or covering closing costs. As Chris Birk, Vice President of Mortgage Insight at Veterans United, explains:

“For many families, helping a child buy a home has become less of an optional gesture and more of a practical response to today’s affordability challenges.”

If your loved ones are in a position to help, that support could make it possible to achieve homeownership sooner than you expected.

Bottom Line

Down payments are smaller than they’ve been in years, making homeownership more attainable for many buyers.

When you combine lower down payment options with down payment assistance programs and support from family, there may be more paths to homeownership than you realize. The best place to start is by connecting with a trusted lender who can help you explore your options and find the loan program that fits your needs.

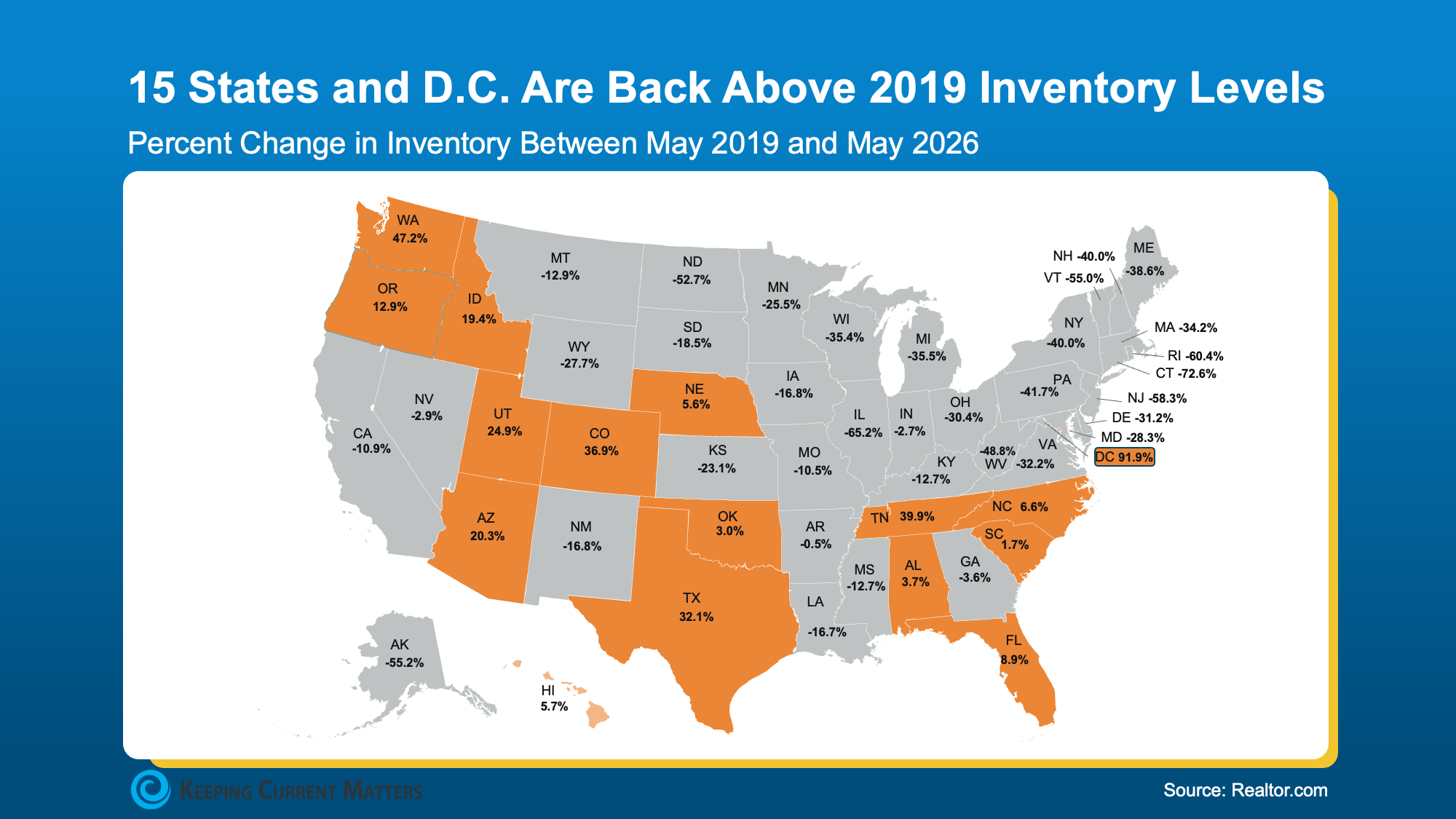

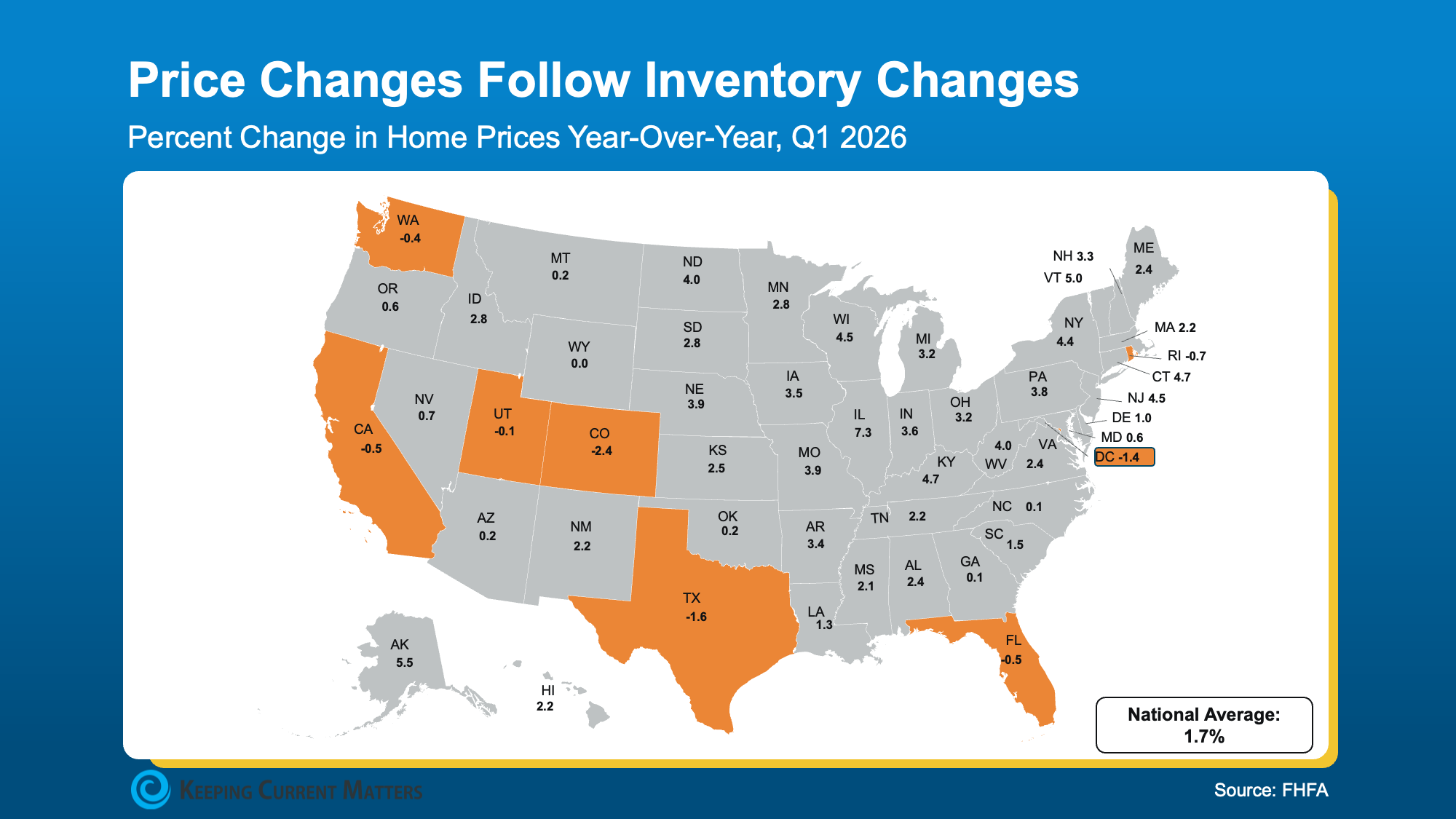

The 1 Factor That Explains Everything Happening with Home Prices Right Now

You’ve probably seen headlines saying home prices are cooling. While that’s true on a national level, it doesn’t tell the whole story. Real estate is local, and what’s happening in one market can be very different from another.

Some areas continue to experience steady home price appreciation, while others have leveled off or even seen slight declines. So what’s driving the difference?

Inventory Is the Biggest Factor

The answer comes down to one key thing: the number of homes available for sale.

When more homes are on the market, buyers have more choices. That means less competition for each property, giving buyers more negotiating power and making it harder for sellers to push prices higher.

On the other hand, when inventory remains limited, buyers compete for fewer available homes. Increased competition often leads to stronger prices and continued appreciation.

This trend is playing out across the country today.

Markets where inventory has returned to—or even exceeded—pre-pandemic levels are generally seeing slower price growth or modest price declines. Meanwhile, areas where housing supply is still well below 2019 levels continue to experience price increases.

According to industry experts, many communities throughout the Northeast and Midwest still have limited inventory, helping support home values. In contrast, parts of Texas, Florida, and Colorado have seen inventory rise above pre-pandemic levels, leading to flatter pricing or slight price adjustments.

Inventory and Prices Go Hand in Hand

Recent housing data shows that most states still have fewer homes available than they did before the pandemic. That’s one reason prices continue to climb in many markets, even if the pace is more moderate than in recent years.

However, several states—including parts of Texas, Florida, Colorado, and Washington, D.C.—now have more inventory than they had in 2019. Those same areas are also the ones experiencing slower appreciation or mild price declines.

This isn’t a coincidence. As inventory rises, buyers gain more leverage, which naturally reduces upward pressure on home prices.

While the national average may show home prices increasing by around 1.7%, that figure combines markets with slight declines and many others where prices are still moving higher.

What Buyers and Sellers Should Know

If you’re buying a home, your local market matters more than ever. In areas where inventory has grown, you may find more available homes, less competition, and sellers who are willing to negotiate. In markets where inventory remains tight, buyers should still expect competition and limited choices.

If you’re selling, pricing your home correctly from the start is essential. In markets with higher inventory, overpricing can cause your home to sit on the market longer and may ultimately result in a lower sale price. In lower-inventory markets, demand remains strong, but strategic pricing is still the key to attracting qualified buyers quickly.

That’s why working with a local real estate agent is so valuable. They understand current inventory levels, pricing trends, and buyer demand in your neighborhood, helping you make informed decisions whether you’re buying or selling.

Bottom Line

National housing headlines only tell part of the story. The real picture depends on what’s happening in your local market.

Whether you’re planning to buy or sell, partnering with a local real estate agent can help you understand your area’s trends and create a strategy that works for today’s market.

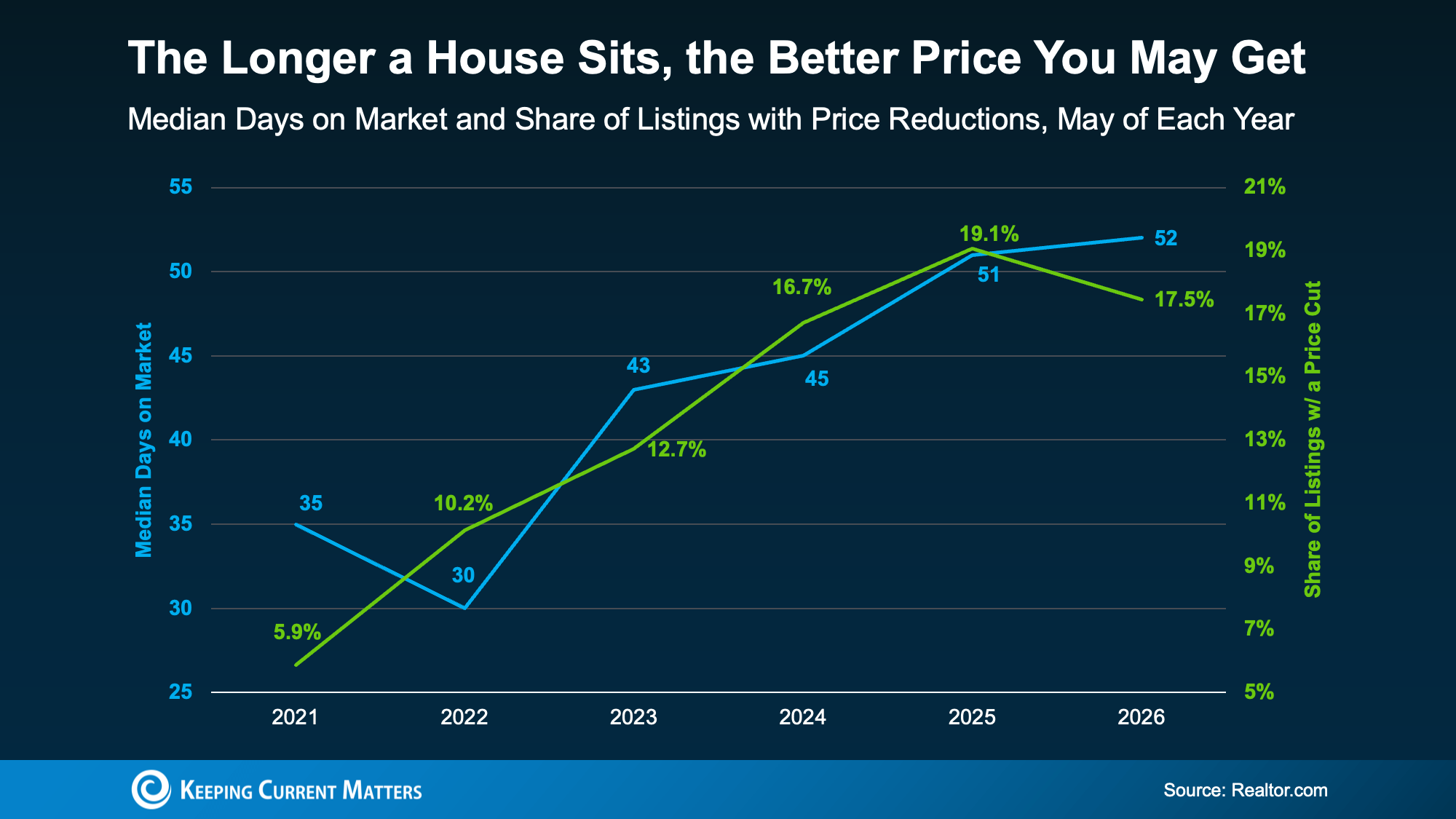

That House That’s Been Sitting Could Be Your Best Shot at a Deal

Open up a home search and you’ll notice them right away—homes that have been listed for two, three, or even more months.

Many buyers skip over these properties, assuming there must be an issue. But that assumption could mean missing out on a great opportunity. In many cases, the longer a home stays on the market, the more willing the seller may be to negotiate, creating potential advantages for buyers.

Where Some Buyers Are Finding Better Deals

If affordability has been the biggest obstacle keeping you from buying a home, there’s a simple strategy worth considering: focus on listings that have been on the market the longest. Those homes can often present some of the best opportunities for buyers.

Here’s why. According to data from Realtor.com, homes that spend more time on the market are more likely to sell for less than their original asking price. In many cases, sellers become more open to price reductions and negotiations the longer their property sits unsold, creating potential savings for buyers.

The blue line represents how long homes are staying on the market, while the green line shows the percentage of listings that have had a price reduction. As one rises, so does the other.

That means homes that have been sitting on the market may offer more opportunity than many buyers realize.

According to Redfin, there are currently about $347 billion worth of stale listings on the market—more than at any other point during this time of year. That’s why it can be worthwhile to ask your agent to sort listings from oldest to newest. The home that fits your needs and budget may already be available; it just might be buried further down the list.

A Longer Time on Market Doesn’t Always Mean There’s a Problem

If a home catches your attention but has been listed for a while, don’t automatically assume something is wrong. In many cases, the reason has little to do with the condition of the property.

Redfin points to several common reasons homes linger on the market:

• The home was initially priced too high

• The online photos or marketing didn’t showcase it effectively

• There is a larger inventory of homes in the area, causing the listing to get overlooked

None of these are necessarily dealbreakers. And if there is a legitimate concern with the property, a professional home inspection will help uncover it. That information can often be used as a negotiating tool rather than a reason to dismiss the home altogether.

The bottom line: don’t overlook homes simply because they’ve been on the market longer. They could offer more value, greater negotiating power, and a better opportunity than you expect.

How To Turn a Lingering Listing into a Win

So how do you capitalize on a lingering listing? According to USA Today, you have two main levers to pull.

The first is price. Work with your agent to study what comparable homes recently sold for, then build an offer around that. Coming in below asking price is fair game when a home has been sitting.

The second is concessions. If a seller won’t budge much on price, they may still help in other ways, like covering some closing costs, repair credits, or even a mortgage rate buydown that lowers your monthly payment.

A local agent has the context to tell which homes are the real opportunities and which are skippable.

Bottom Line

A home that’s been on the market for a while isn’t always a warning sign. In today’s market, it could be one of the best opportunities for buyers looking to maximize their budget and gain negotiating power.

If you’re wondering which long-standing listings are worth a closer look, connect with a local real estate professional. An experienced agent can help you identify hidden gems, evaluate potential concerns, and determine whether a property is truly a smart investment.

Two Big Reasons To Move This Summer

A lot of people who are thinking about moving are telling themselves the same thing: “Maybe I’ll wait until later this year when things settle down.”

While that may seem like a smart strategy, there’s something important to consider before putting your plans on hold. Mortgage rates aren’t expected to shift significantly. If that’s the main reason you’re waiting, the payoff may not be what you expect. There could also be opportunities you miss by delaying.

Historically, Summer has been one of the strongest seasons of the year for both buyers and sellers. If you wait until Fall or Winter, some of those advantages may already be behind you.

Why Summer Matters in Real Estate

The Summer housing market typically brings more activity from both buyers and sellers. More homes come on the market, and motivated buyers remain active. That combination can create opportunities that may not be available later in the year.

Buyers: Fresh Inventory Is Your Biggest Summer Opportunity

One of the most common challenges buyers have faced in recent years has been limited inventory. You may have experienced it yourself:

- You find a home you like, but it’s outside your budget.

- You find one that fits your budget, but it doesn’t check the boxes you want.

- Or worse, nothing new comes on the market for weeks.

This is where Summer often creates an advantage.

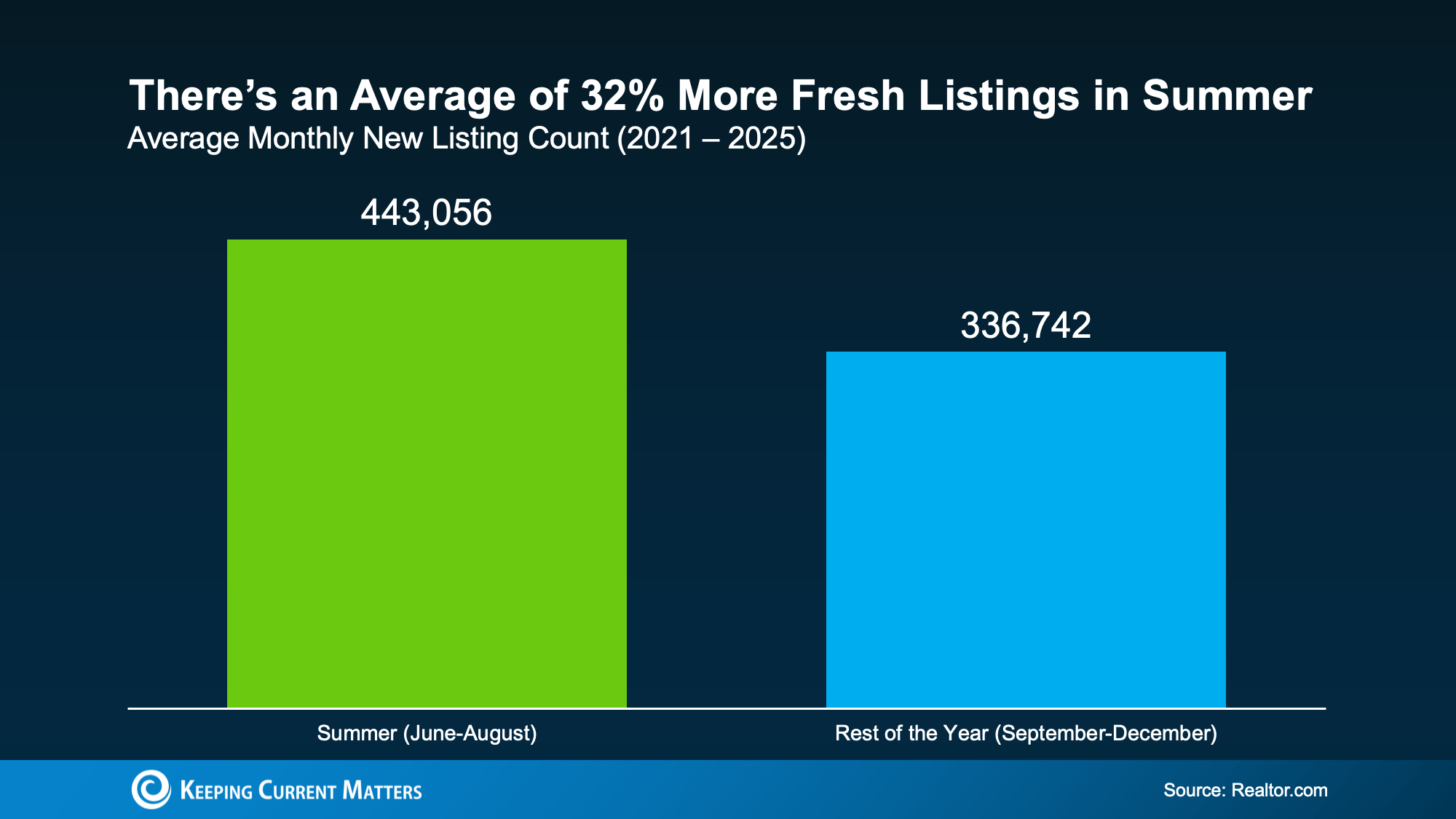

Looking at market trends from recent years, Summer months consistently bring more sellers into the market than the months that follow. As a result, buyers typically have more homes to choose from.

According to Realtor.com, the average Summer month usually offers about 32% more newly listed homes than the average month between September and December.

More Choices Can Change Everything

With more homes hitting the market, your chances of finding one that fits both your needs and budget increase.

Sometimes it only takes one home to completely change your search. When more listings are available, the odds of finding that perfect match improve.

However, this seasonal opportunity doesn’t last forever. New inventory typically slows down once Summer comes to an end.

By that point, many homeowners who planned to sell have already listed their properties. Families hoping to move before the school year begins have often completed their move or are already well into the process. As a result, new listing activity generally eases heading into Fall and Winter.

Every market cycle is different. Still, if your biggest challenge has been finding the right home at the right price, waiting until later in the year may not lead to more choices. Recent trends suggest the opposite could happen.

Sellers: Homes Often Command Higher Prices During Summer

If you’ve been considering selling, you may be tempted to wait because of headlines about price reductions, lower asking prices, or softer market conditions in certain areas. Those headlines don’t always tell the full story. Market conditions can vary greatly from one location to another.

The key takeaway is simple. Even as the housing market becomes more balanced and some areas experience price adjustments, that doesn’t mean your opportunity to sell has passed.

Seasonal Trends Still Favor Sellers

Seasonal trends can still work in your favor. This Summer may offer an excellent opportunity to maximize your home’s value.

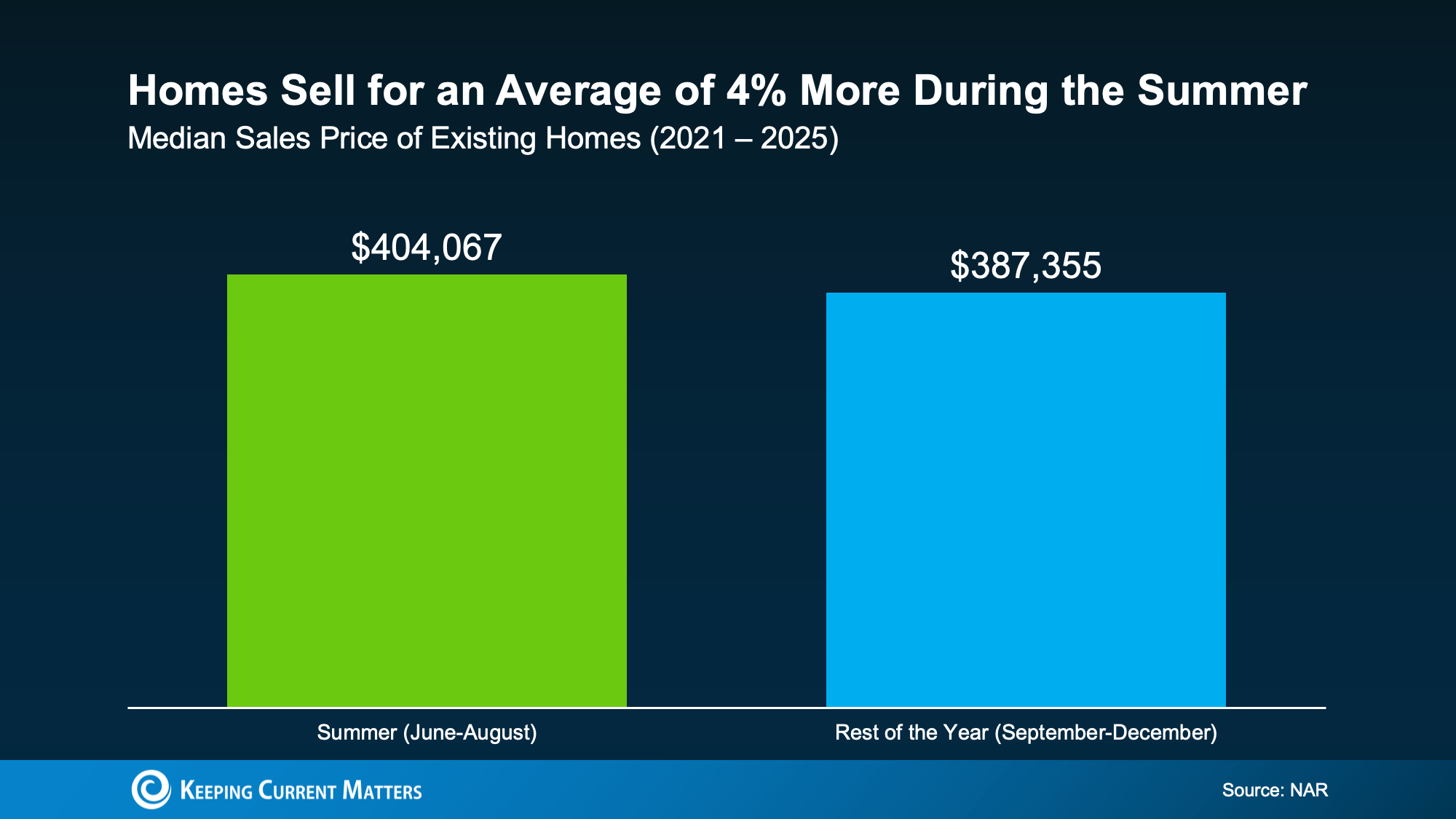

According to the National Association of Realtors (NAR), homes sold during Summer months typically sell for about 4% more than homes sold during the average month from September through December.

Why Summer Buyers Are More Motivated

Summer buyers often work within specific timelines. Many are trying to relocate before a new school year begins. Others are taking advantage of vacation time and favorable weather to tour homes. That added motivation can lead to stronger offers.

Of course, that doesn’t mean you should automatically raise your asking price by 4% this Summer. In today’s market, pricing too aggressively could work against you.

Instead, it suggests that if your goal is to achieve the strongest possible sale price, moving during the Summer may be more advantageous than waiting until later in the year.

Based on typical seasonal patterns, sellers often receive higher offers during Summer than they do in Fall or Winter. Buyer activity generally slows as the year progresses.

If you’re already planning a move, that’s an important factor to consider.

Bottom Line

Could waiting until later this year still work out? Absolutely. However, it’s important to understand the opportunities available right now so you can make a fully informed decision.

If a move is part of your plans for 2026, connect with a real estate professional to discuss your goals and priorities. Depending on what matters most to you, this Summer could be the ideal time to make your move.

The Mid-Year Housing Market Update: Why Forecasts Changed in 2026

If the housing market feels uncertain right now, you’re definitely not alone.

Mortgage rates have remained higher than many expected. Home sales haven’t accelerated the way experts anticipated. And many buyers and sellers are still wondering when the market will become more affordable and easier to navigate.

The reality is that a lot has changed during the first half of this year.

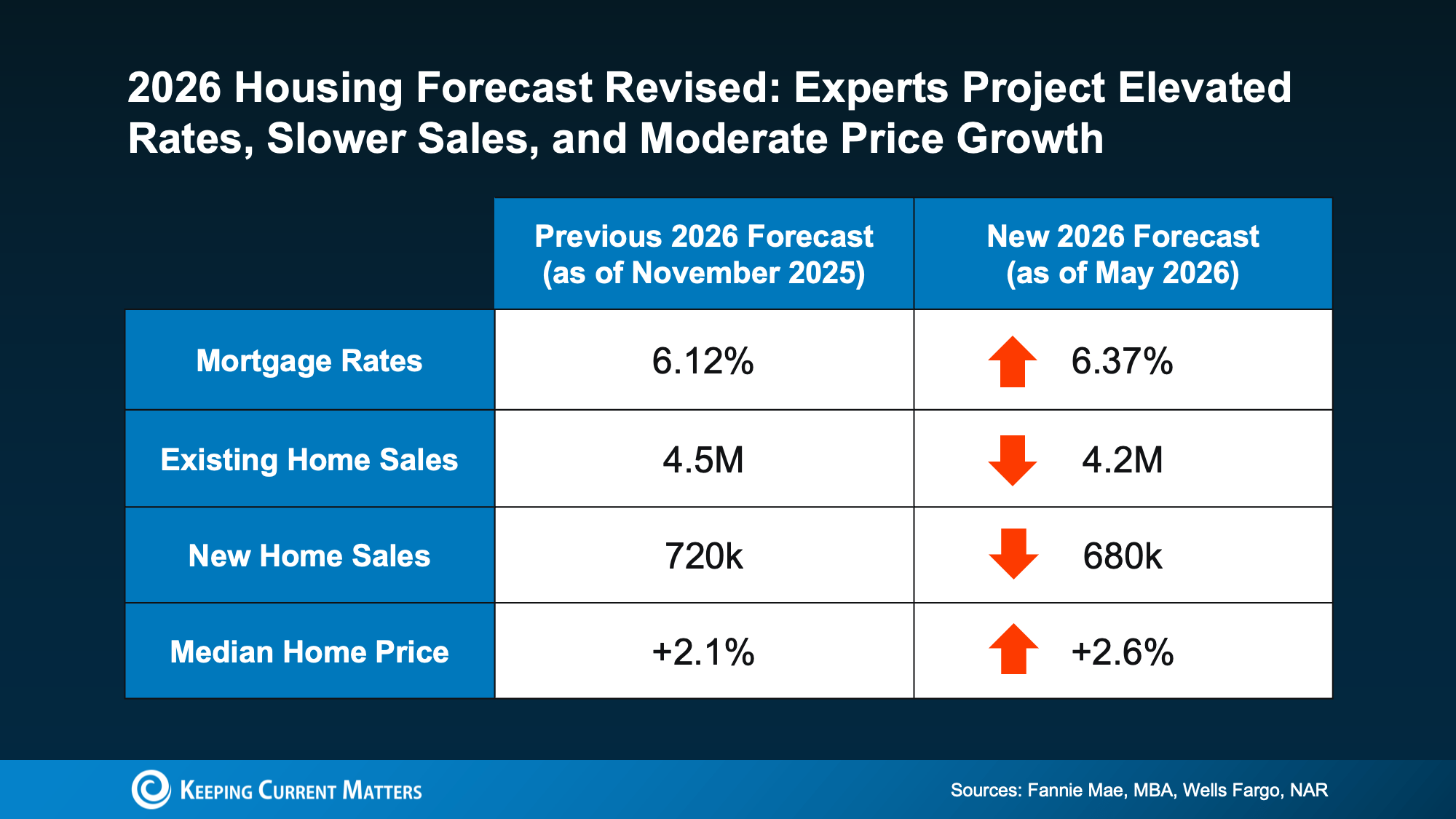

At the end of 2025, economists were forecasting a much stronger housing market for 2026. They expected mortgage rates to decline, affordability to improve significantly, and home sales to gain momentum.

However, persistent inflation, economic uncertainty, and ongoing geopolitical tensions around the world kept mortgage rates elevated. Because rates stayed higher for longer than anticipated, many buyers chose to remain on the sidelines.

As a result, housing experts have adjusted their forecasts for the remainder of the year (see graph below):

a graph of sales and sales

So, what does all of this mean for you? Let’s take a closer look.

Mortgage Rates May Stay Higher for Longer

While many buyers are hoping mortgage rates will return to the high-5% or low-6% range seen earlier this year, most experts no longer expect that to happen in 2026.

Instead, forecasts have been revised upward from the low-6% range originally projected. Many leading housing organizations now expect rates to remain in the mid-6% range throughout the year. The positive news is that rates are still lower than they were a year ago.

Of course, forecasts can change. If inflation eases or global conflicts begin to settle, rates could move lower. But if you’re delaying your plans solely in hopes of significantly lower rates, the payoff may not be as large as expected.

Existing Home Sales Forecasts Have Been Lowered

At the end of 2025, economists projected approximately 4.5 million existing-home sales in 2026. Today, that forecast has been adjusted closer to 4.2 million.

This tells us that affordability challenges continue to impact buyer activity.

Higher mortgage rates have increased monthly housing costs, making homeownership more difficult for many households—especially first-time buyers. While the pace of the market has slowed compared to earlier expectations, experts still anticipate more homes will sell this year than last year.

Many economists believe that once geopolitical concerns ease and mortgage rates stabilize, a large number of waiting buyers will return to the market. As Lawrence Yun, Chief Economist at NAR, explains:

“There is sizable pent-up demand that could be released into the market.”

There have already been encouraging signs in recent months. Pending home sales have shown month-over-month improvement despite higher borrowing costs.

If purchasing a home is financially comfortable for you today, buying now may still be worth considering. Waiting could mean facing increased competition and fewer available homes when more buyers decide to re-enter the market.

New Home Sales Have Also Slowed

Homebuilders entered 2026 expecting a stronger sales environment. Earlier projections suggested new-home sales would exceed 700,000 this year. Current forecasts now place that figure slightly below that mark.

Once again, mortgage rates are a major factor behind the slowdown.

However, this creates potential opportunities for buyers. Builders may be more motivated to attract purchasers through incentives, price adjustments, and flexible negotiations. In areas with significant new construction activity, this can be a major advantage.

Builders may be willing to offer concessions or negotiate more aggressively, giving buyers additional leverage when making a purchase.

Home Prices Are Still Expected To Increase

This remains one of the most important points in the entire forecast.

Even though sales activity has cooled, experts have largely maintained their projections for home price growth. They still expect home prices to rise nationally throughout the year.

The reason is simple: while demand has softened somewhat, housing inventory remains relatively limited in many markets. That supply-and-demand imbalance continues to support home values, even as overall activity slows.

Naturally, real estate is local, and market conditions vary from one area to another. Some regions are experiencing more cooling than others. But on a national level, experts are still forecasting steady appreciation rather than significant price declines.

That should provide reassurance to both buyers and sellers.

Sellers generally want to protect the value of their homes, and buyers often feel more confident making a major investment when values are expected to remain stable or increase over time.

Bottom Line

The housing market has not rebounded as quickly as many experts originally expected. But that doesn’t mean the market has stopped moving.

Inflation, higher mortgage rates, and ongoing economic uncertainty have led economists to revise their forecasts for 2026. However, many industry experts believe momentum will return once these challenges begin to ease.

Rather than viewing these forecast revisions as a warning sign, think of them as a reflection of current economic conditions.

If you’re curious about what’s happening in your local market and how it may affect your plans for the remainder of the year, connect with a local real estate professional who can help you understand your options.

The Real Reason Some People Are Still Moving Right Now

You may be telling yourself that you’re going to wait before making a move. Maybe you’re hoping mortgage rates will come down, home prices will soften, or the market will feel a little less competitive.

A lot of people are thinking the same thing right now. But here’s what many are beginning to realize.

Waiting doesn’t usually solve the reason you wanted to move in the first place.

Your growing family may still need more space. Your empty nest may still feel a little too quiet.

Your parents or grandparents may still need you closer by.

Maybe you recently got married… or went through a divorce.

Maybe your retirement plans still include living somewhere new.

At some point, staying put can feel more difficult than making a move.

That’s why many people are still choosing to buy or sell in today’s market. Not because conditions are perfect, but because the life events driving their decision haven’t gone away.

And perhaps that’s where you are too. If so, you’re far from alone.

The Real Reasons People Move

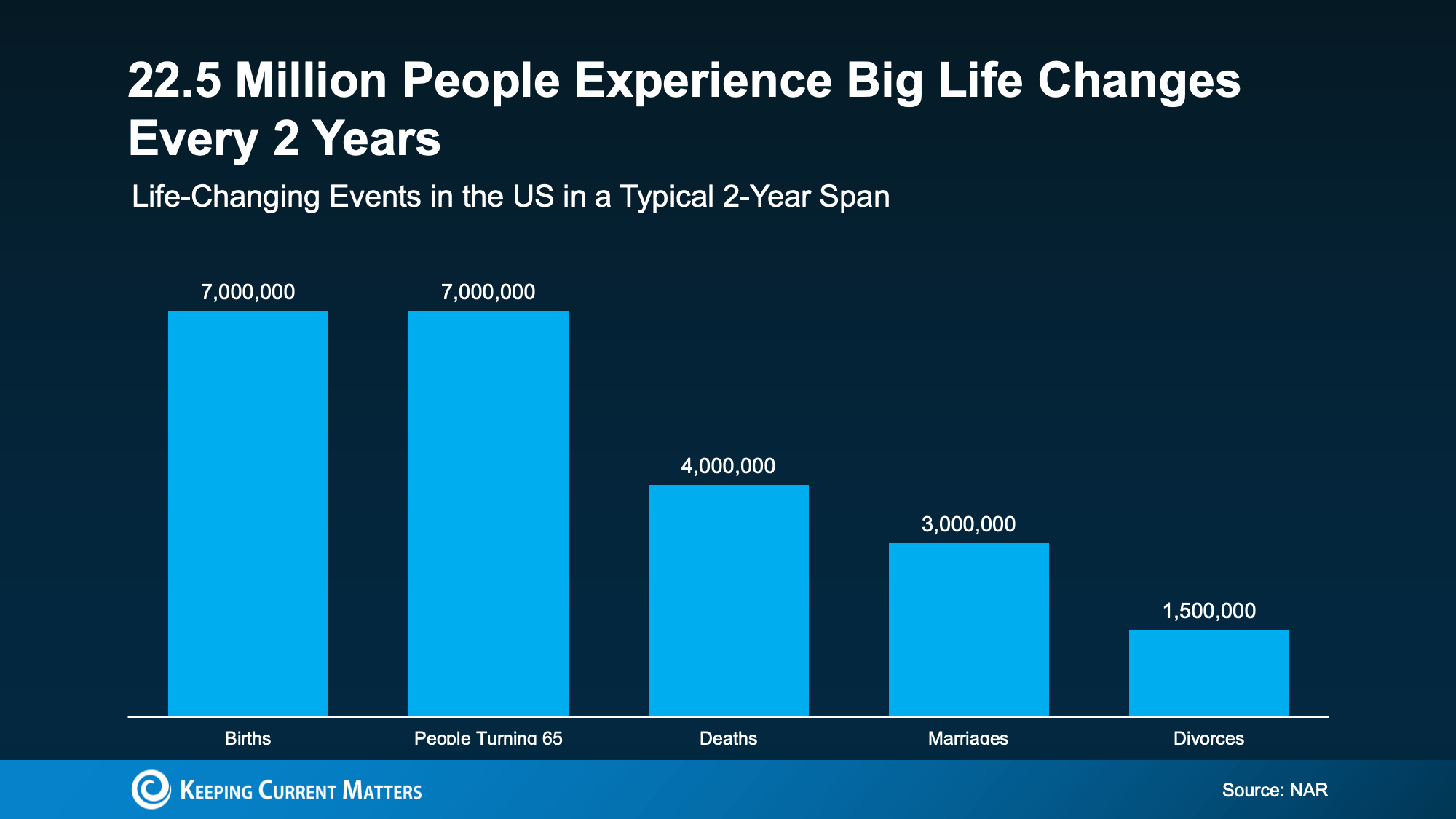

According to the National Association of Realtors (NAR), one out of every five buyers last year said they felt they needed to purchase a home at that particular time, regardless of market conditions.

That’s an important perspective to keep in mind. While the financial side of a move certainly matters, major life changes don’t wait for mortgage rates or home prices to reach the ideal level.

In fact, NAR reports that approximately 22.5 million people experience significant life changes over a typical two-year period (see graph below).

These are the kinds of events that often impact how much space you need, where you want to live, and what type of lifestyle fits your current stage of life. As Chen Zhao, Head of Economics Research at Redfin, explains:

“Life doesn’t stand still—people get new jobs, grow their families, downsize after retirement, or simply want to live in a different neighborhood.”

And that’s exactly why waiting can be so challenging. Every month spent hoping for different market conditions is another month living in a home that may no longer fit your needs. Feeling stuck can be frustrating, and that feeling often doesn’t simply fade away.

There May Be More Opportunity Than You Think

While affordability remains a concern for many buyers, opportunities may still exist to help you make your move.

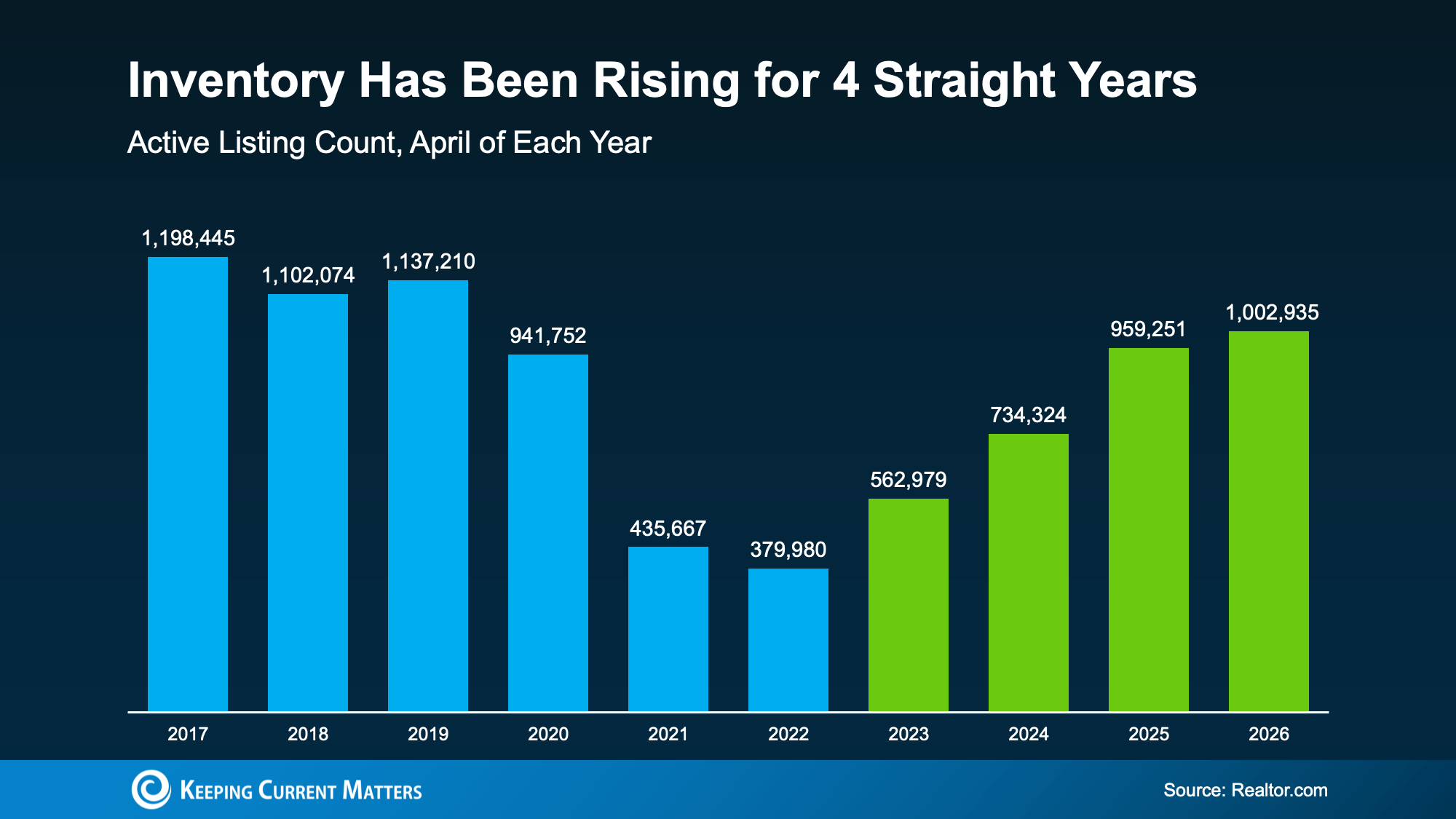

The number of homes available for sale has been increasing for four consecutive years (see graph below). That means buyers have more options to choose from and, in many markets, more negotiating power than they had just a few years ago.

That doesn’t mean moving is effortless. But it does mean more people are finding ways to make their plans work.

So, if you’ve been putting your move on hold, perhaps the question isn’t only:

“What’s the market doing?” or “When will conditions improve?”

Maybe it’s also worth asking:

“Can my current home still support the life I want to live?”

If the answer is no, it may be time to explore what your options look like right now, regardless of where rates or prices are headed. With more inventory available, you may find a home that better fits both your lifestyle and your budget.

Bottom Line

Life changes. Priorities evolve. Families grow. Children move out. Careers shift. And eventually, the home you’re living in may no longer fit the life you’re building.

If that’s something you’ve been thinking about lately, connect with a real estate professional to discuss what your options might look like today, no matter where mortgage rates or home prices are.

Life doesn’t always wait for perfect market conditions. Your next move may not have to either.

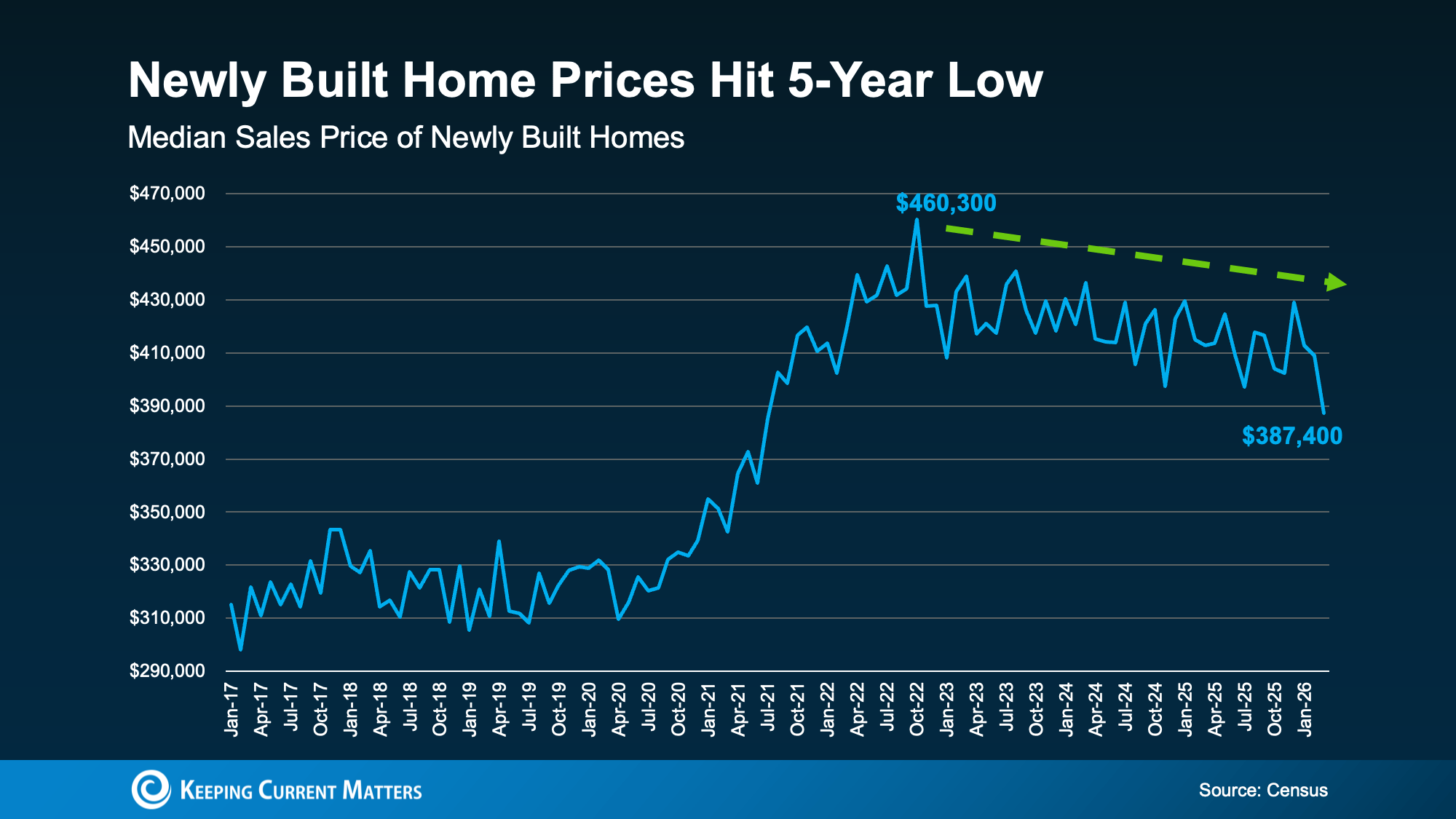

Newly Built Home Prices Hit a 5-Year Low

If you’ve always assumed a newly built home is just not in your budget, you should know the math just got a little friendlier.

The median sale price of a newly built home is now at its lowest level since 2021, according to the latest data from the Census. And on top of that, builders are still rolling out incentives to bring buyers through the door.

Here’s what’s happening, and what it means if you’re shopping right now.

Prices on Newly Built Homes Have Come Down

After a steep climb during the pandemic years, prices have eased a bit. The median sale price of newly built homes is sitting at about $390,000. That’s the lowest it’s been in nearly five years (see graph below):

While local markets vary, the national trend is moving in your favor, especially if you’re a first-time buyer. According to Zonda, prices in the entry-level price range have dropped roughly 2.7% over the past 12 months – more than any other price tier.

While local markets vary, the national trend is moving in your favor, especially if you’re a first-time buyer. According to Zonda, prices in the entry-level price range have dropped roughly 2.7% over the past 12 months – more than any other price tier.

That doesn’t mean every home in every market is suddenly affordable. But it does mean that, broadly, you’ll see the best prices on new builds since 2021, if you’re buying now.

Why This Isn’t a Repeat of 2008

And just in case you’re thinking it, lower prices don’t mean the new home market is in trouble. Builders today are being intentional about how much inventory they have, so it doesn’t pile up the way it did in 2008.

If you look back up at the graph, you’ll see that even after the recent improvement in new home prices, they’re still higher than pre-pandemic norms. So, this isn’t a crash. It’s a builder strategy to keep inventory moving.

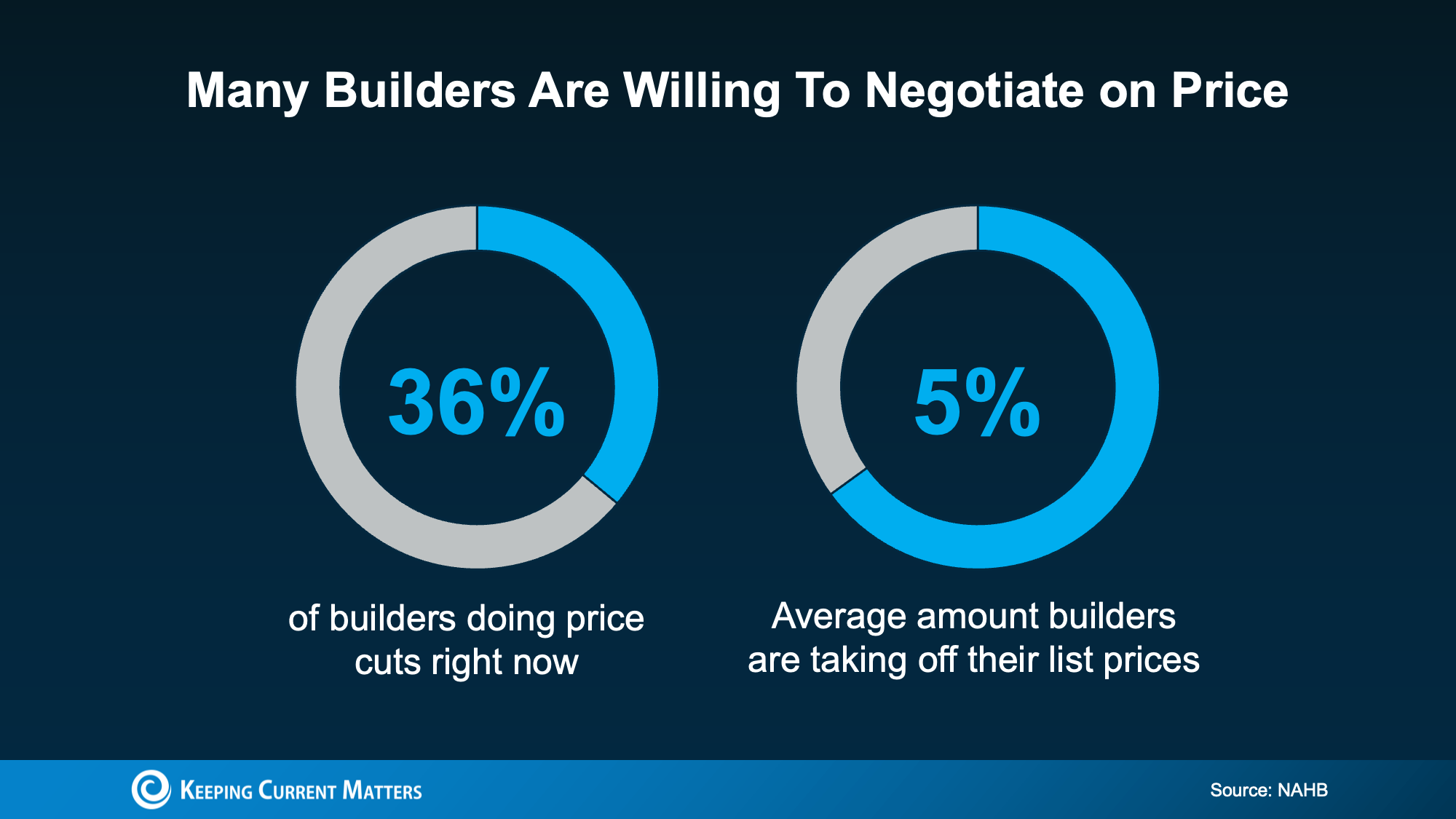

Homebuilders Are Still Sweetening the Deal

Lower sticker prices aren’t the only break buyers are getting. According to the National Association of Home Builders (NAHB), 60% of builders are currently offering some form of incentive to attract buyers. Those typically include:

- Help with closing costs: Some builders are covering thousands of dollars in fees to reduce the upfront cost of buying.

- Extra upgrades: Think premium finishes, appliance packages, and designer features, often added at no extra cost.

- Mortgage rate buydowns: When the builder pays to lower your mortgage rate, which reduces your monthly payment.

- Price cuts: Over one in three builders (36%) are cutting prices right now, averaging about 5% off list price (see graph below):

That last point catches a lot of buyers off guard – most assume that builders won’t budge on price.

That last point catches a lot of buyers off guard – most assume that builders won’t budge on price.

But builders need to move what they’ve built. That’s a different mindset than a homeowner deciding whether to budge on price. So, you may find they’re more open to adjusting the price than you’d think. As Joel Berner, Senior Economist at Realtor.com, puts it:

“. . . many existing-home sellers resort to taking down their listing instead of taking less than their desired price, but builders are more motivated to sell their inventory than owner-occupants . . .”

And if you use the version of the graph that shows 2008 prices, you can even reference that in this explainer.

And if here, should I change the last sentence of the lede?

Bottom Line

Builder incentives and lower new home prices are working to your advantage in a way they haven’t in years. Connect with a local real estate agent to see what’s available in your area and what kind of deal a builder may be willing to make.

{kind=link}