Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Should You Wait for Lower Mortgage Rates?

Many homebuyers wonder if they should wait for lower mortgage rates. Mortgage rates have already dropped into the upper 5% range twice this year, only to tick back up into the low 6% range shortly after. If you saw that and thought, “Great, I missed it,” you’re not alone.

A lot of buyers are treating the 5s like some kind of magic number. As if moving from 6.1% to 5.99% suddenly changes everything. And from a mindset perspective, it does feel different.

But here’s the part most people don’t actually run the math on.

The Payment Difference Isn’t What You Think

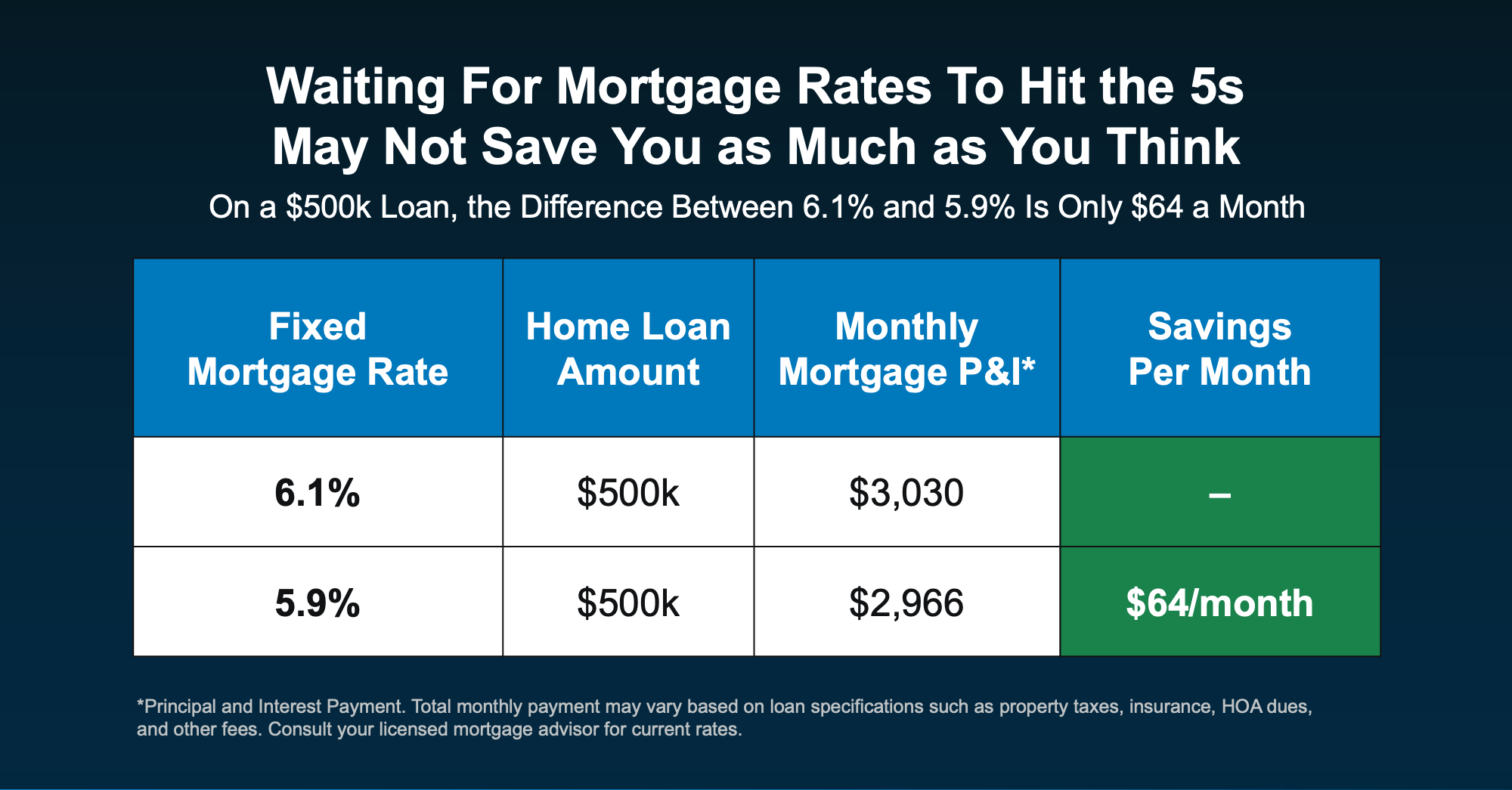

Let’s say you’re looking at a $500,000 home loan. At 6.1%, generally speaking, your principal and interest payment is roughly $3,030 per month. At 5.9%, it’s about $2,966 per month.

That’s a difference of only $64 a month.

Not $300.

Not $500.

Sixty dollars.

Let that sink in for just a moment.

Yes, over time that $64 a month can add up. But it’s far from the dramatic swing many buyers imagine when they say they’re “waiting for the 5s.”

The psychological impact of seeing a 5 in front of your rate can feel big. The financial impact? It might be something you don’t even notice when it’s all said and done.

Experts Aren’t Predicting a Big Drop

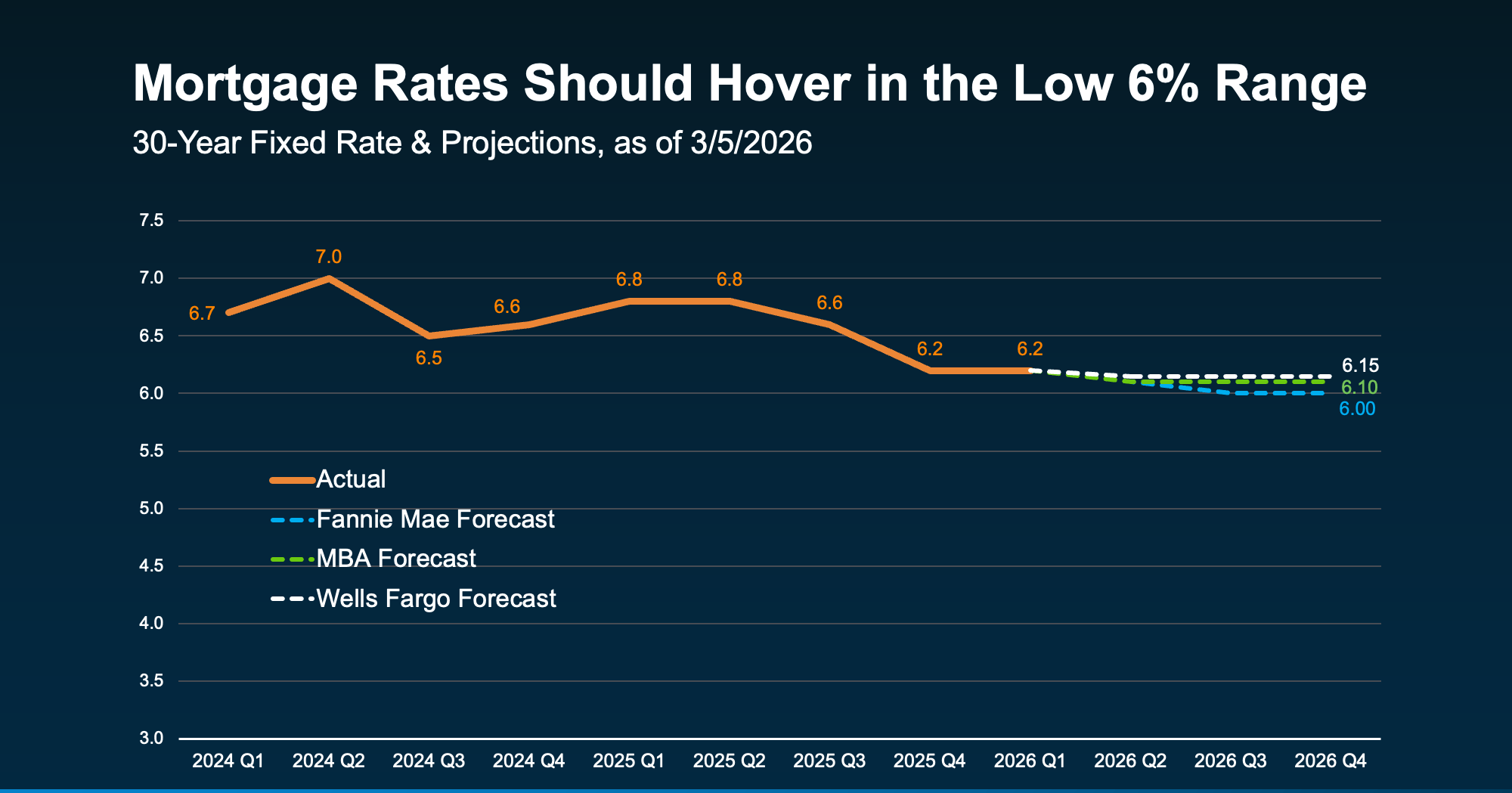

Another important piece to think about: most housing economists aren’t forecasting a long-term return to 5% territory anytime soon.

While rates will move up and down, likely hitting the high 5s here and there, the broader expectation is for mortgage rates to hover in the low 6% range this year, not stay in the 5’s or decline much more.

While it certainly could happen, the reality is, waiting for a deep drop may not deliver the payoff you’re hoping for, if you’re holding out

The Bigger Question to Ask

Instead of asking, “Did I miss the 5s?” A better question is: “Does today’s payment work for me?”

If the monthly payment fits comfortably in your budget, and you’ve found a home that meets your needs, the difference between 6.1% and 5.9% likely isn’t the deciding factor. It might be one of them, but it shouldn’t be everything.

And remember, mortgage rates aren’t permanent. If they drop meaningfully later, refinancing is always an option. But you can’t refinance a home you didn’t buy.

Waiting Might Feel Safe, But It Isn’t Always Strategic

It’s natural to want the best possible rate. Everyone does. But sometimes buyers overestimate how much a rate in the high 5s will change things in today’s market. Many people ask themselves if they should wait for lower mortgage rates, thinking that a small drop will dramatically improve their monthly payment.

Don’t miss the fact that rates have already come down. A year ago, they were in the 7s. Now? They’re hovering in the low 6s. And for a lot of people, that percentage point difference that’s already here is the real game changer.

If you paused your plans when rates were higher, now may be the right time to re-run your numbers. Not because rates are “perfect.” But because the monthly payment math might work better than you think, even with rates in the low 6s.

Before assuming you’ve missed your moment, take another look at the numbers.

You may find it never disappeared.

Bottom Line

If you’ve been sitting on the sidelines waiting for that magic five number for rates, that strategy may not pay off as much as you’d expect.

Reference: https://www.keepingcurrentmatters.com/2026/03/09/should-you-wait-for-lower-rates/

Repeat Home Buyers And Their Hidden Advantage Today

What if you didn’t have a mortgage payment on your next home? For many repeat home buyers, that’s not as unrealistic as it sounds.

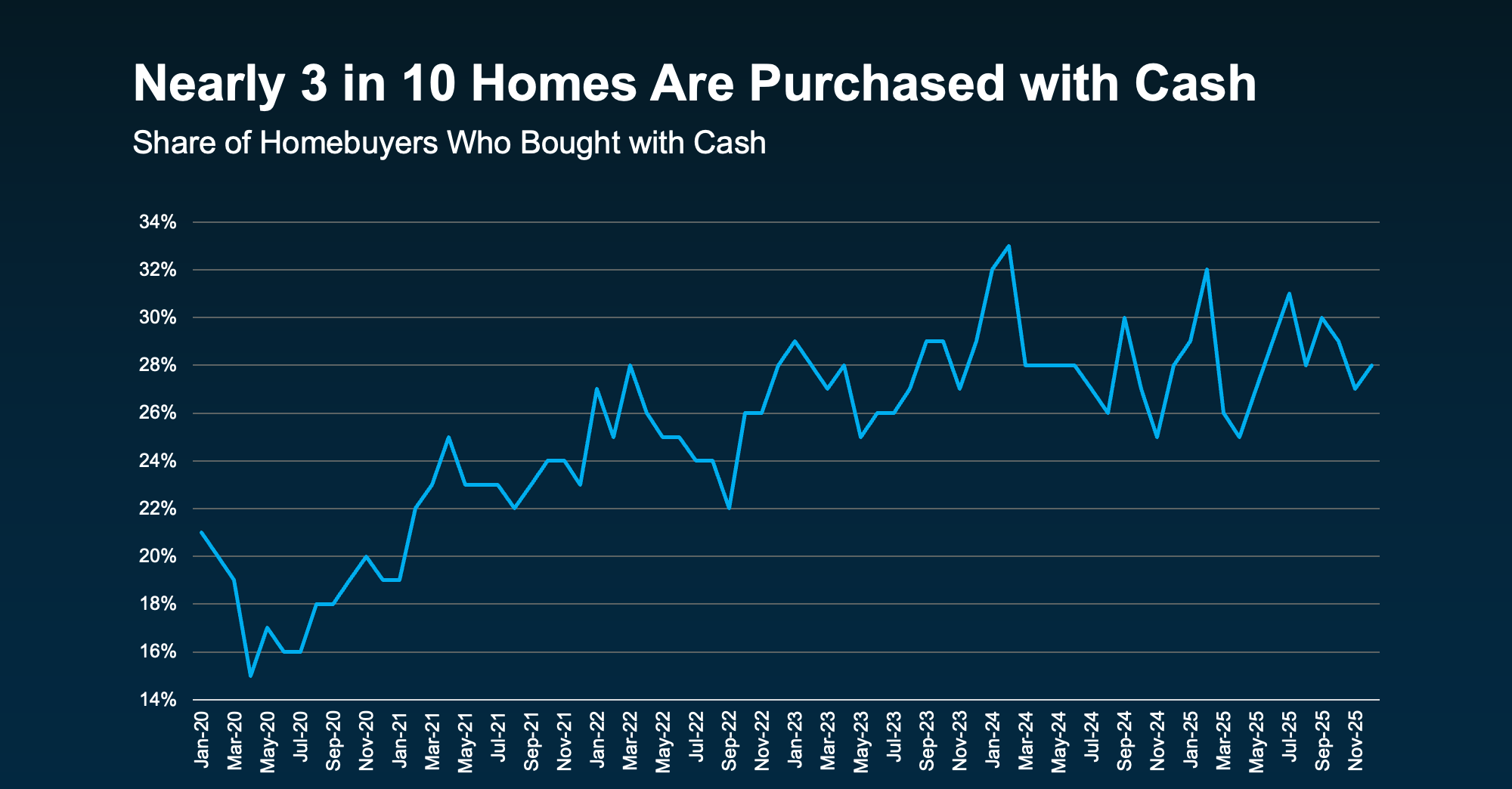

Nearly 3 in 10 homes purchased today are bought in cash, according to the National Association of Realtors (NAR). That’s far more than the pre-pandemic norm (see graph below):

So, how are so many repeat home buyers making that happen? The answer is simple: home equity.

Back in 2020-2021, mortgage rates and the number of homes for sale were both at all-time lows. And that combination pushed home prices up, fast.

If you owned a home during that time, it likely gained significant value – maybe even enough to buy your next house in cash. NAR explains:

“. . . rising home equity has armed many existing homeowners with the financial leverage to make cash offers, allowing them to convert years of price appreciation into immediate purchasing power.”

Here’s why you may want to go that route yourself, if you have enough equity to do it.

1. Your Offer Becomes More Attractive

Sellers value certainty. And an all-cash offer removes one of the biggest unknowns in a transaction: financing. As Rocket Mortgage explains:

“Cash offers are attractive to sellers. Sellers often prefer to work with cash buyers if they can because they don’t have to worry about a buyer’s financing falling through at the last minute.”

In many markets, an all-cash offer can give you a serious edge.

2. You Can Close Faster

And since you don’t have to worry about underwriting, lender approvals, and loan processing, the time it takes to close shrinks. Cotality puts it this way:

“Cash buyers have always enjoyed an edge over borrowers. They remove financing risk, reduce delays, and often close in days rather than weeks.”

If the owner of the house you’re buying is already under contract on their next home or they just need to move fast (like for a new job), that speed is a real draw.

3. You Won’t Have Monthly Mortgage Payments

When you buy in cash, you don’t have to finance your purchase. That means you don’t have to worry about what today’s mortgage rates are and you own the house outright from the day you close. And that’s a big deal.

No mortgage.

No monthly payment.

Full ownership.

That financial freedom opens the door for other big lifestyle benefits. Zillow explains:

“Paying in cash means you own your home outright. This eliminates the need for monthly mortgage payments, freeing up your finances for other priorities like savings, travel, or home improvements.”

4. You May Get a Better Deal

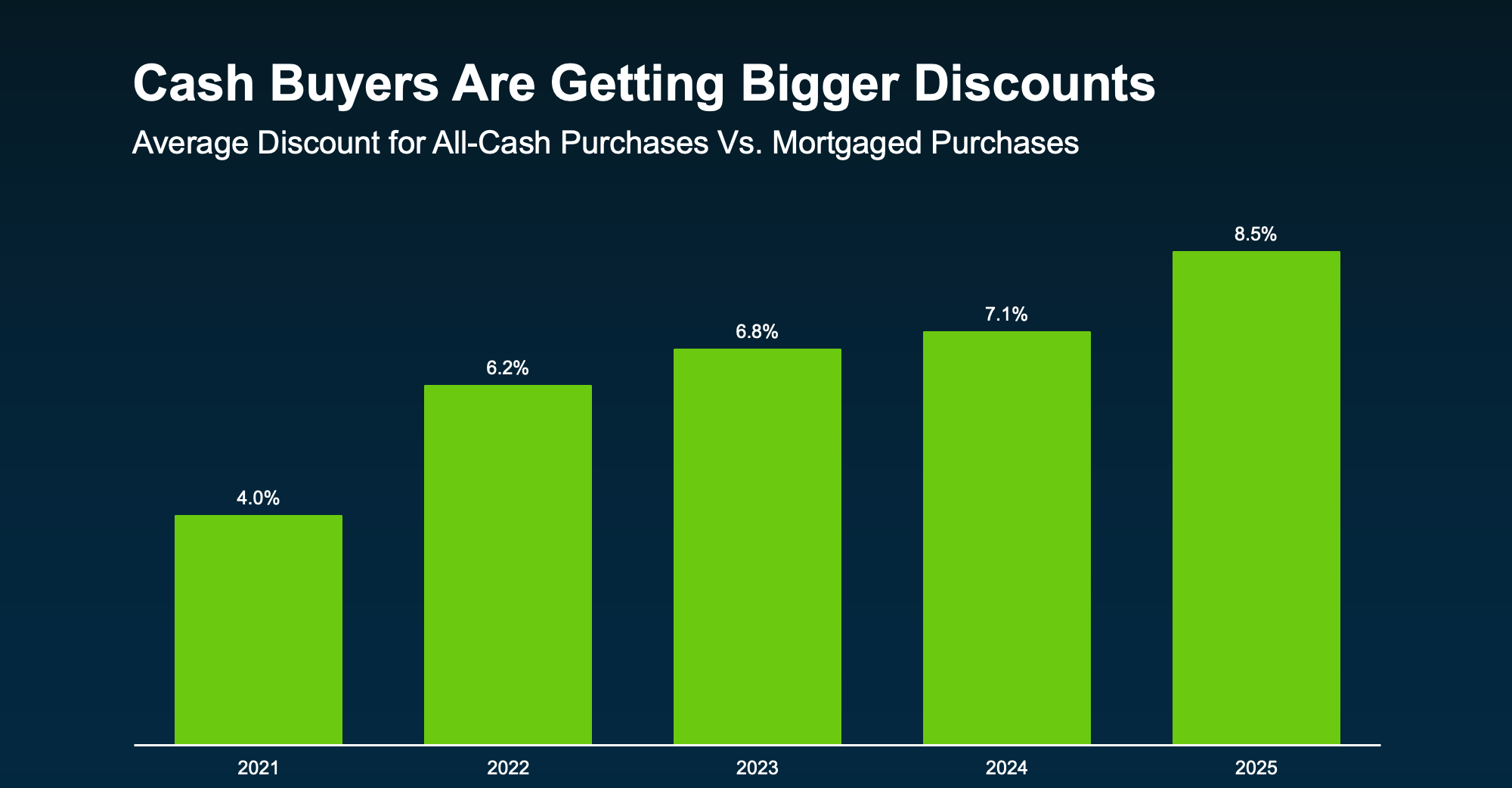

And here’s one more thing that surprises a lot of homeowners: cash buyers often pay less for the house.

According to Cotality, all-cash buyers tend to spend roughly 9% less on the house than buyers who use a mortgage. That’s because some sellers are willing to accept lower offers to get a deal done quickly, with more certainty of closing, and fewer financing hoops to jump through. As Cotality explains:

“From a seller’s point of view, a lower but reliable offer can feel preferable to a higher one that may collapse weeks later.”

And that advantage grows with each passing year (see graph below):

Is an All-Cash Move Realistic for You?

Not every homeowner will buy their next house outright in cash. And that’s okay.

But the bigger takeaway is this: the equity you’ve built may give you more options than you think.

Whether that means downsizing and eliminating a mortgage entirely, or just relocating with stronger negotiating power, your current house may be what makes it possible.

Bottom Line

Before assuming you’ll need another traditional mortgage, it’s worth asking one simple question: How much equity do you really have? Because the answer might change what you thought your next move could look like.

Reference: https://www.keepingcurrentmatters.com/2026/03/02/the-hidden-advantage-repeat-buyers-have-right-now/

Why Your Asking Price Matters When Selling Your Home

There’s one decision you’re going to make when you sell that determines whether your house sells quickly or sits on the market. Whether buyers make an offer or scroll past, and whether you walk away with the maximum return or end up cutting the price later. That decision is your asking price, and it plays a critical role in the success of your home sale.

The #1 Mistake Sellers Make Today: Trusting the Wrong Number

If you’re thinking of moving and trying to figure out what your house may sell for, it’s tempting to start with an online home value tool. They’re fast, free, and easy. And you don’t have to talk to anyone. But here’s the problem: they don’t know your house.

And that can be a bigger drawback than you realize.

Where Online Estimates Fall Short

Online tools often lag behind the market. They look in the rearview mirror, relying on closed sales and delayed information. And in that sense, they’re using incomplete data.

That’s not a miss in how these systems are built. Some information just isn’t available online. Bankrate explains:

“While these tools can be a useful starting point, keep in mind that they typically do not provide the most accurate pricing. Algorithms can only rely on the information available; they can’t account for things like a home’s condition or renovations made since the last public information was updated.”

They can’t see:

- The unique features that make your house special

- All the work you’ve put in to keep it in good condition

- Or, how in-demand your specific neighborhood is right now

So, while they may do a good job in some cases, they can’t be as accurate as a local agent who has boots on the ground day in and day out.

In a market where buyers have more options, a seemingly small margin of error can cost you thousands if you price too low, or weeks of lost momentum and time if you price too high.

If you want to sell for the most money and in the least amount of time, you don’t want the fast answer on how to price your house. You want the right one.

That’s why the savviest homeowners today don’t rely on algorithms when it actually matters. They rely on people, specifically trusted local agents.

What an Expert Agent Brings to the Table

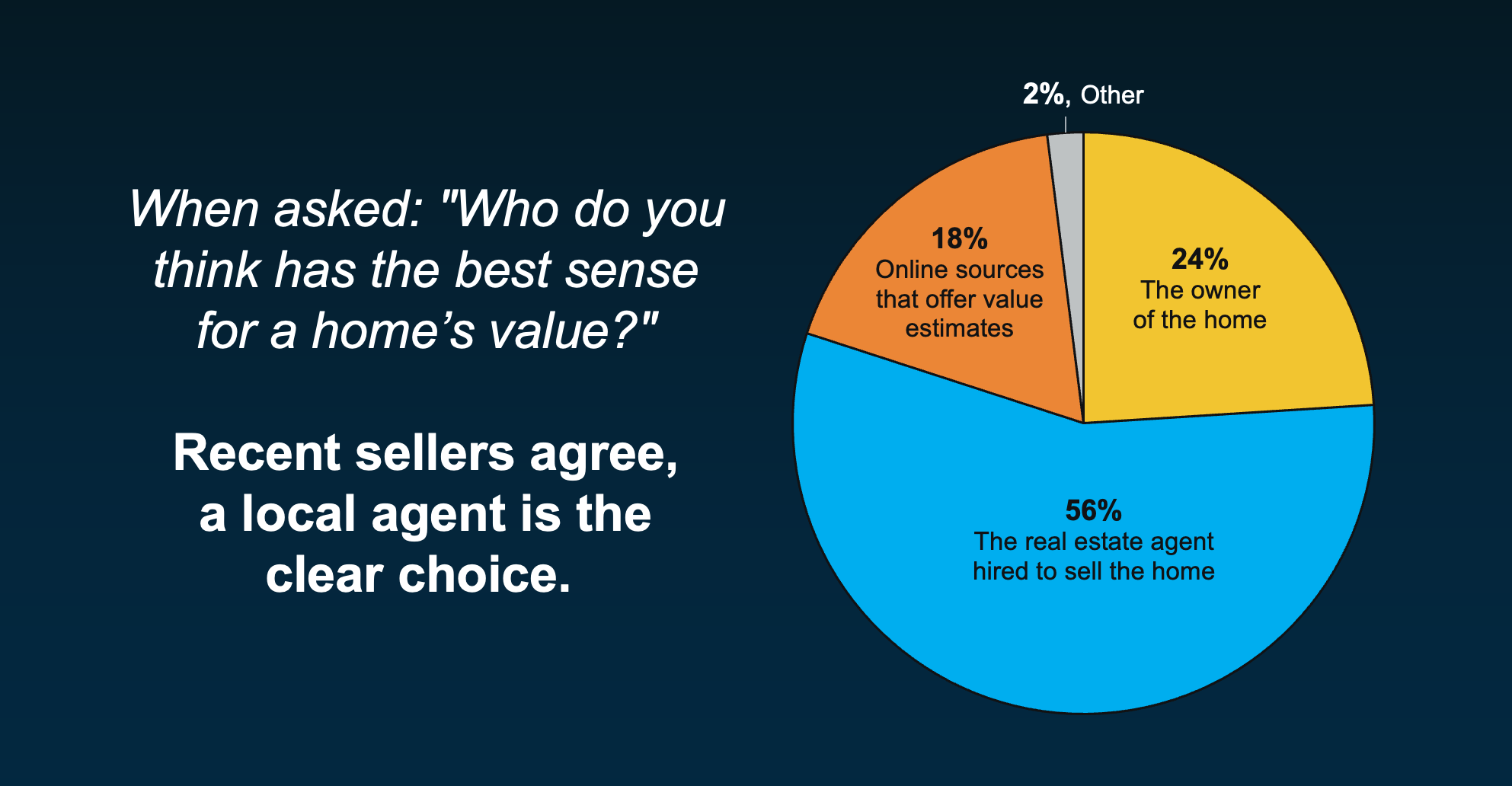

According to 1000WATT, sellers overwhelmingly believe real estate agents have the best sense of a home’s true value, far more than any automated tools.

That confidence isn’t accidental. As Bankrate puts it:

“A professional appraiser or real estate agent can visit the home in person, assess the neighborhood as a whole as well as the individual property, perform more thorough market research, and consider subjective details.”

And those details matter. A skilled local agent doesn’t just pull reports. They know what’s happening right now:

- What buyers are paying this month, not last month, or even last year

- How your home compares to the current competition in your neighborhood

- Which features add value based on what buyers are willing to pay for today

- How to price your house to create urgency in this market

And once an agent steps foot in your house, they may even find your online estimate undershot your value. So, if you stuck with the estimate you got online, you’d actually be leaving money on the table. And no one wants that.

Bottom Line

While online tools can give you a rough starting point, only a local expert can give you a price that actually works.

Reference: https://www.keepingcurrentmatters.com/2026/02/19/the-price-you-set-can-make-or-break-your-sale/

Four Ways Your Home Equity Can Work for You

Home equity is one of the most powerful financial tools homeowners have today. You may have heard that many homeowners have built up a significant amount of home equity in recent years, but what does that really mean? Let’s break it down.

Because your equity isn’t just a number, it’s a powerful asset that can help you take your next big step in life.

How Much Equity Does the Typical Homeowner Have?

Here’s how it works. As you pay down your loan and home prices rise through the years, the share of your home that you own free and clear grows. That’s your equity.

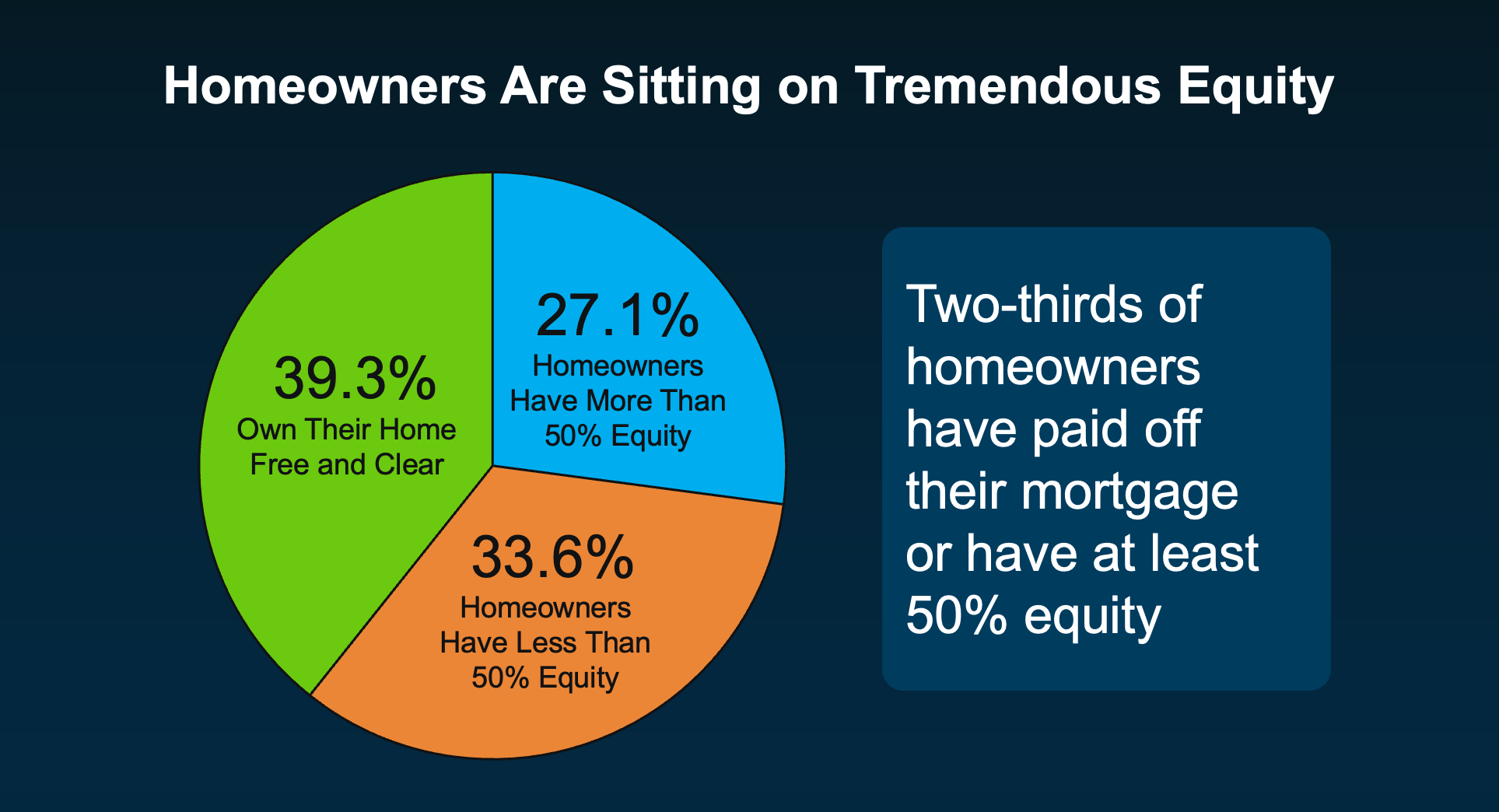

And according to data from the Census and ATTOM, two-thirds of homeowners have a substantial amount of it today.

39% own their home outright without owing anything on it. And another 27% have at least 50% equity in their homes (see chart below):

That’s a big deal. And just in case you’re wondering how that translates into real dollars, Cotality says the typical homeowner has almost $300k in equity today. That’s six figures.

And whether you have that much, even more, or a bit less, here are a few examples of how you can use it.

Ways You Could Use Your Home Equity

1. Move Into a Home That Better Fits Your Life

Your needs change over time. Maybe your home is starting to feel cramped, or maybe you have more space than you need now that your adult children have moved out. Either way, you can use your equity as a down payment on a home that’s a better fit for what you need now, and going forward. You may even have enough equity to buy your next house in cash.

2. Upgrade Your Current Home

And if you’re not ready to move just yet, you could reinvest it in your current home instead. Renovations like a kitchen refresh or updated bathrooms could add value when it’s time to sell down the line. Just be sure to talk to a real estate agent before you tackle your project list, so you can prioritize updates that’ll give you the biggest return later on.

3. Fund a Major Life Goal

Equity can also help fund your life goals – whether it’s starting a business, saving for retirement, covering education costs, or helping out someone you love. Some homeowners are even passing down some of that wealth to help fund a loved one’s down payment on a home.

4. Avoid Foreclosure in Tough Times

If you’re struggling with payments, your equity can also be a lifeline. Many homeowners who hit financial hardships can sell their homes and walk away with money in their pockets instead of facing foreclosure. If that’s something on your mind, talk to a real estate expert about your options and how your equity can help.

Your Next Steps

If you’re interested in using your equity for one of the reasons above, here’s what to do:

- Step 1: Ask a local agent for a personalized equity assessment on your home.

- Step 2: Meet with a financial advisor if you’re interested in using that equity.

Because when it comes to tapping into this resource, there are a few things you’ll want to keep in mind – like making sure you still have a good loan-to-value ratio (LTV) even if you use some of your equity.

That means, as a general rule of thumb, you want to maintain at least 20% equity in your home as a financial cushion – something many homeowners didn’t know back in the crash of 2008.

The good news is, according to the Intercontinental Exchange, most of today’s equity meets that guideline:

“As of Q4, mortgage holders have $17.3T in home equity, including $11.2T in tappable equity ‒ accessible via cash-out refinances or home equity lines while maintaining 20% equity in the property.”

Bottom Line

Your home equity is one of the biggest financial assets you have. Whether you’re thinking about moving, remodeling, or working toward a big goal, it’s worth exploring your options.

Reference: https://www.keepingcurrentmatters.com/2026/02/12/four-ways-your-home-equity-can-work-for-you/

Why Townhomes Are a Smart Choice for First-Time Buyers

Buying your first home can feel frustrating when the numbers don’t line up the way you expected. Townhomes are increasingly becoming the solution for many first-time buyers who know they’re ready to own but struggle to find something that fits both their lifestyle and budget.

Townhomes are becoming a bigger part of today’s housing supply, and that shift is opening doors for first-time buyers in a way we haven’t seen in years. That’s because they offer a more realistic path to step into homeownership without stretching yourself too thin, especially in a market where affordability can still feel tight.

There Are More Townhomes To Choose From

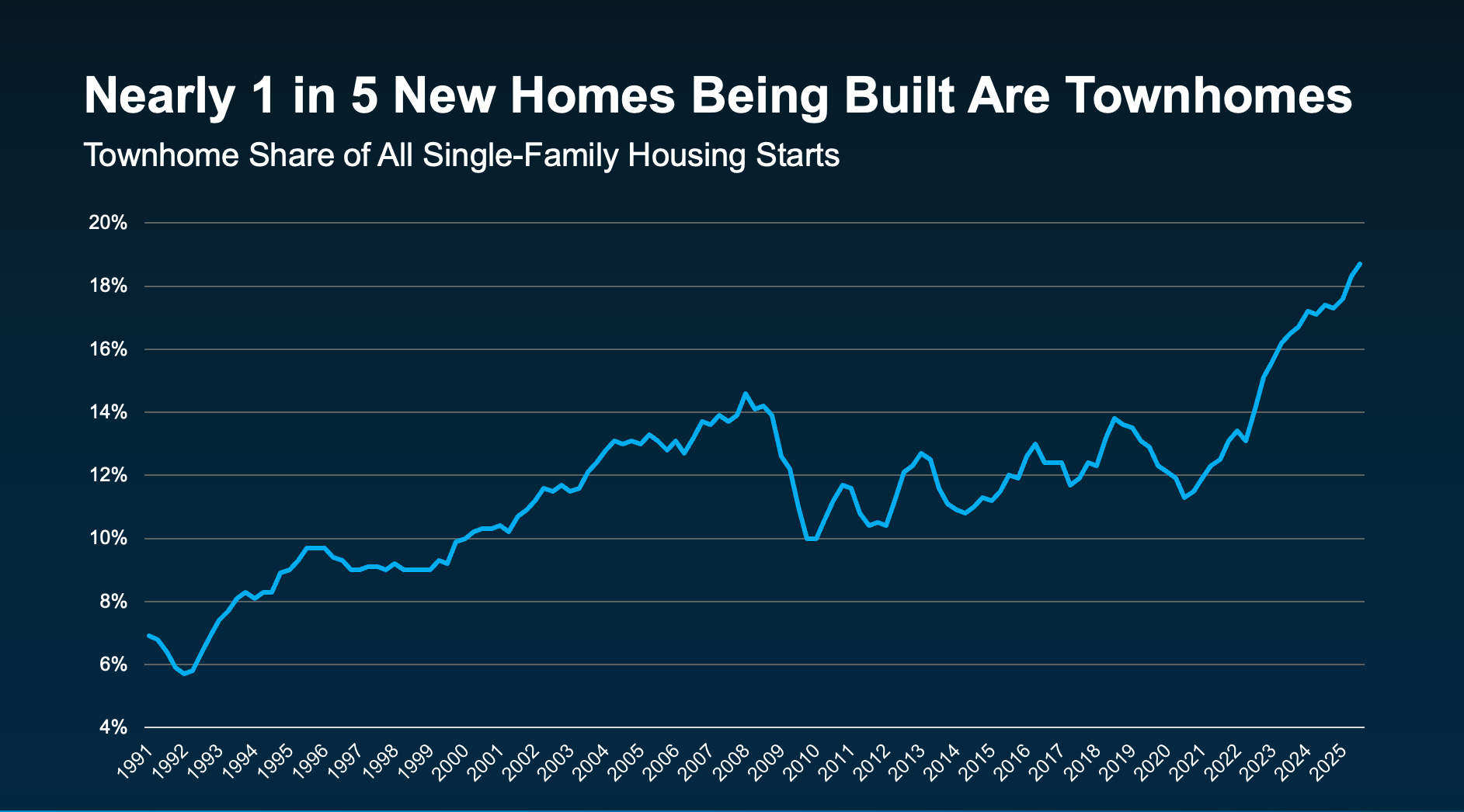

Builders are building more townhomes than they have in decades. In fact, when you look at data from the National Association of Home Builders, nearly 1 in 5 new single-family homes being built today is a townhome. That’s the highest share on record (see graph below):

To put that in perspective, just a decade ago, townhomes made up closer to 1 in 10 new construction homes.

That gives today’s buyers far more townhome options than they had in the past. And that’s a really good thing.

Townhomes are one of the best ways for first-time buyers to finally get their foot in the door. And seeing that there’s more available for sale means one thing: you may have more opportunity to break into the market than you think.

Here’s why they’re such a popular choice for buyers like you.

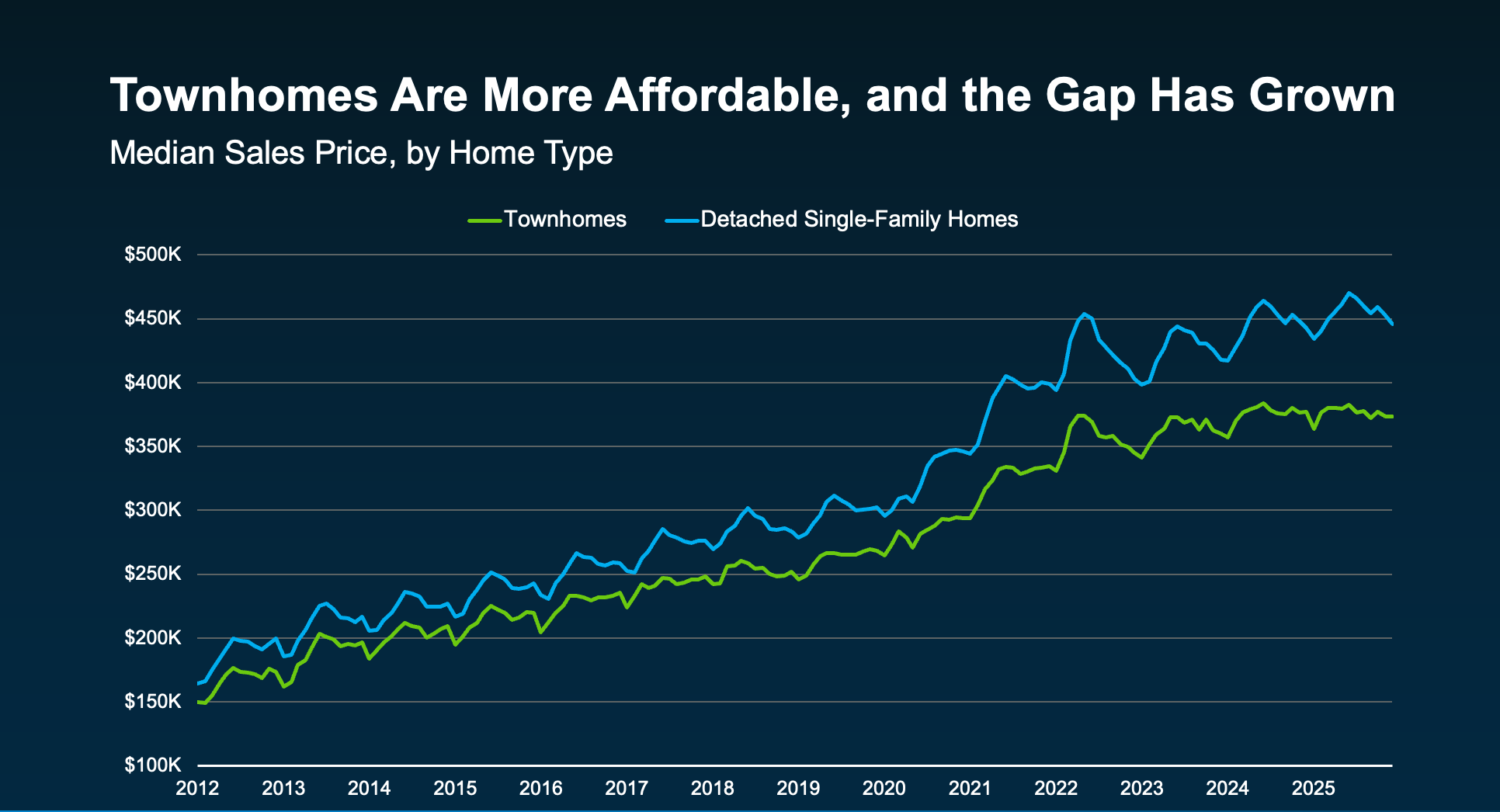

Townhomes Tend To Be More Affordable

While prices vary by market, Redfin data shows townhomes are typically priced lower than detached single-family homes nationally. And that gap has grown in recent years as the supply of this type of home has grown too (see graph below):

There are two main reasons you may find a better deal on a townhome today.

Reason #1: Size

Townhomes are usually smaller by design. Most modern townhomes fall in the 1,300–1,500 square foot range, which helps keep prices, and monthly payments, lower. Basically, it works like this. Since they usually have a smaller footprint, they’re cheaper to build, and that makes them less expensive to buy, too. Ali Wolf, Chief Economist at NewHomeSource, explains how this helps buyers:

“With the high cost of housing across the country, townhomes have emerged as a vital, more accessible entry point into homeownership. They are often priced lower than detached houses, offering buyers – especially first-timers, young professionals, and those downsizing – the chance to build equity without breaking the bank.”

Reason #2: Builder Motivation

And here’s another thing working in your favor. With more inventory than in recent years, homebuilders are motivated to sell what they’ve already built.

So, many may be more willing to negotiate, whether that means price flexibility, closing cost help, or potentially throwing in upgrades. According to the National Association of Realtors:

“. . . home builders say they’re ready to attract more first-time home buyers. They’re responding to affordability pressures through lower cost homes and builder incentives. About 40% of builders cut prices on newly built homes at the end of last year . . . Roughly two-thirds of builders also offered additional incentives, like mortgage rate buydowns.”

Bottom Line

If buying your first home feels just out of reach, the right option might not be a different timeline. It might be a different type of home.

Rising Home Insurance Costs: What Buyers Should Know

Rising home insurance costs are becoming an important factor for today’s buyers to plan for. Buying a home is one of the biggest purchases you’ll ever make, and homeowner’s insurance plays a critical role in protecting that investment. Think of it as your safety net. NerdWallet explains it:

- Covers Repairs and Rebuilding Costs: If your home is damaged by fire, storms, or other covered events, it helps pay for repairs and possibly even a full rebuild, if that’s deemed necessary.

- Protects Your Belongings: It can also cover personal items like furniture, electronics, jewelry, and clothing if they’re stolen or damaged.

- Provides Liability Coverage: And, if someone gets injured on your property, your policy can help cover medical bills or legal expenses.

But that peace of mind does come with a cost, and lately those costs have been rising.

Why Home Insurance Premiums Are Going Up

There are a number of factors causing insurance premiums to rise today. But, in the simplest sense, here’s what’s driving prices up according to the Insurance Research Council (IRC).

Severe weather events and natural disasters are happening increasingly often, leading to more claims. At the same time, homebuilding materials and labor are more expensive. So, when it comes time to work on those claims, insurers have to manage higher costs to repair or rebuild the affected homes.

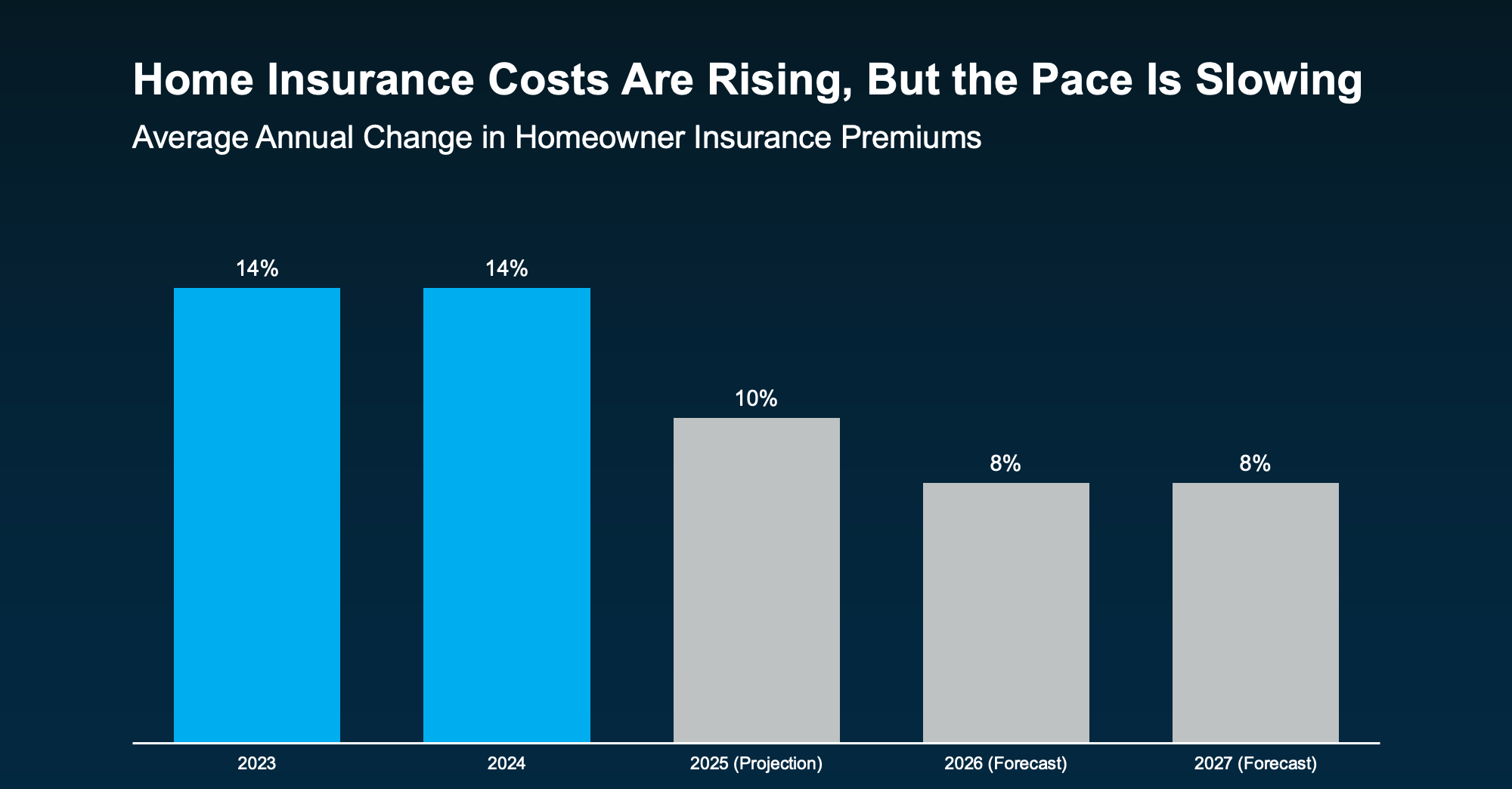

That combination adds up to higher premiums. You can see how it’s climbed recently in the graph below. Each bar marks the percentage increase in insurance costs for that calendar year.

The good news is, the annual pace of the increase may be starting to ease according to ResiClub and Cotality. By their count:

- In 2023 and 2024, insurance costs went up 14% a year.

- In 2025, they rose about 10%.

- And in 2026 and 2027, it’s expected to go up about 8% each year.

That’s still an increase, but at least the pace is slowing down. And here’s another silver lining.

While insurance costs are rising, mortgage rates are falling. And that can help offset some of this expense. As Michael Gaines, Senior VP of Capital Markets, Cardinal Financial, explains:

“Rising taxes and insurance do create pressure, but they don’t erase the benefits of a lower rate . . . A small rate improvement, paired with the right loan program and smart planning, can still make homeownership possible . . . It’s less about one factor canceling another out, and more about helping buyers layer the right solutions together.”

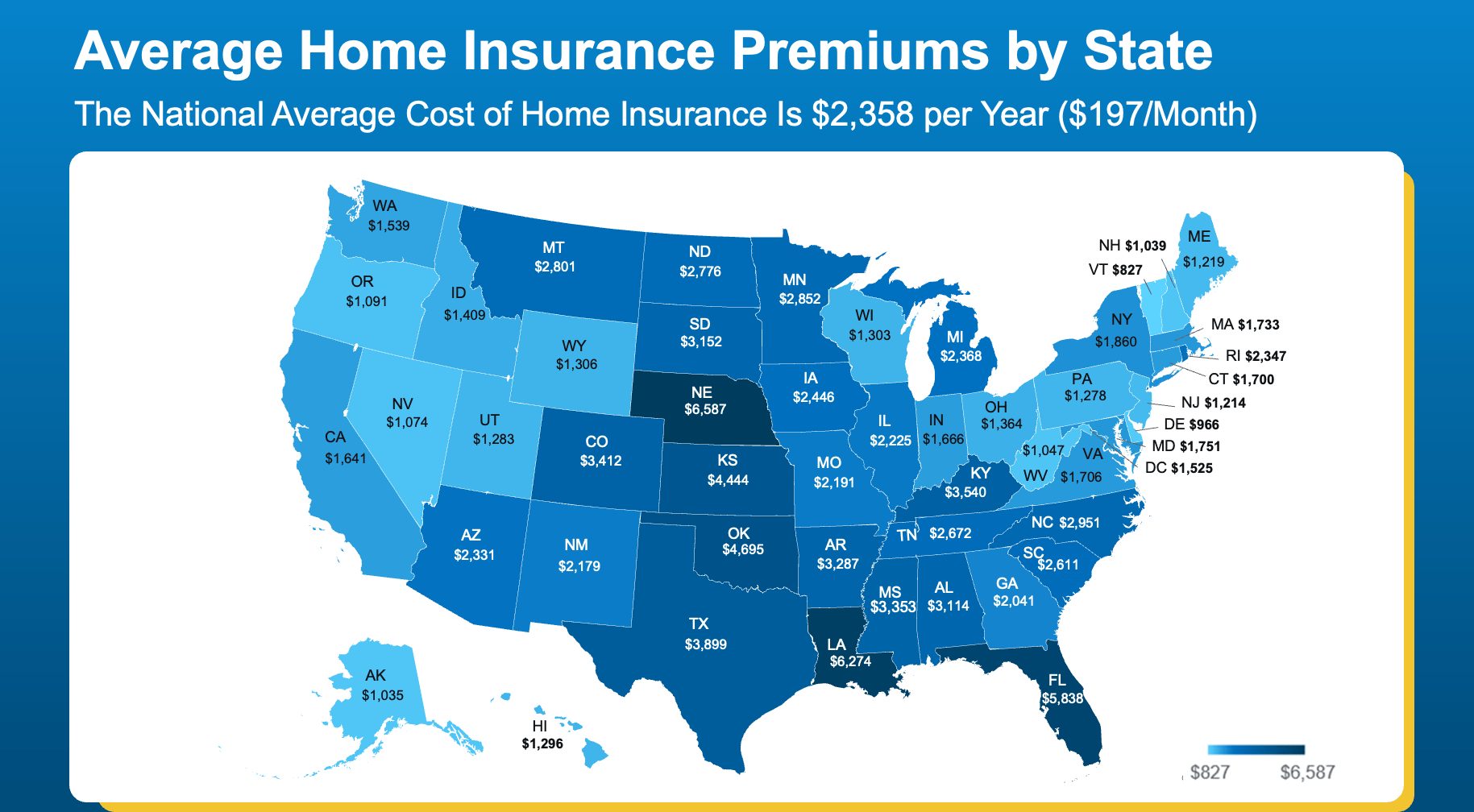

Costs Are Going To Be Different Depending on Where You Buy

So how much do you need to budget for this? It depends on the price point and location of house, the coverage you need, and more. And just like with everything else in real estate, costs vary by area.

You can get a rough idea of your state’s typical premiums in the map below:

So, What Can You Do About It?

Generally speaking, your first insurance payment will be wrapped into your closing costs. But after that, it’ll become a recurring expense. That’s why knowing these premiums are rising is so important. It helps you factor that into your budget, so you go in with a full picture of what you can comfortably afford.

If you’re crunching the numbers and trying to find other ways to save, here are a few tips from Insurify and NerdWallet that can help you get the best insurance price possible:

- Shop Around – Compare quotes from multiple companies.

- Bundle Policies – Combine home and auto for discounts.

- Ask About Discounts – Don’t miss out on savings you may qualify for.

- Highlight Upgrades – Features like a new roof or storm windows can cut costs.

- Improve Your Credit – A stronger credit score can mean better premiums.

Bottom Line

If you’re planning to buy a home, understanding rising home insurance costs is an important part of building a realistic budget.

While costs are rising, knowing what to expect and how to shop around can make a big difference as you’re budgeting for your purchase. Because this isn’t coverage you’ll want to skimp on. It’s your best protection for what’s likely your biggest investment.

Why You Shouldn’t Skip a Home Sitting on the Market

When you see a home sitting on the market longer than expected, the reaction is almost automatic. Buyers start asking themselves:

- What’s wrong with it?

- Why hasn’t anyone bought it yet?

- Am I missing something?

That mindset made sense a few years ago. But in today’s market, you may actually miss out.

More Time on Market Isn’t Automatically a Concern Anymore

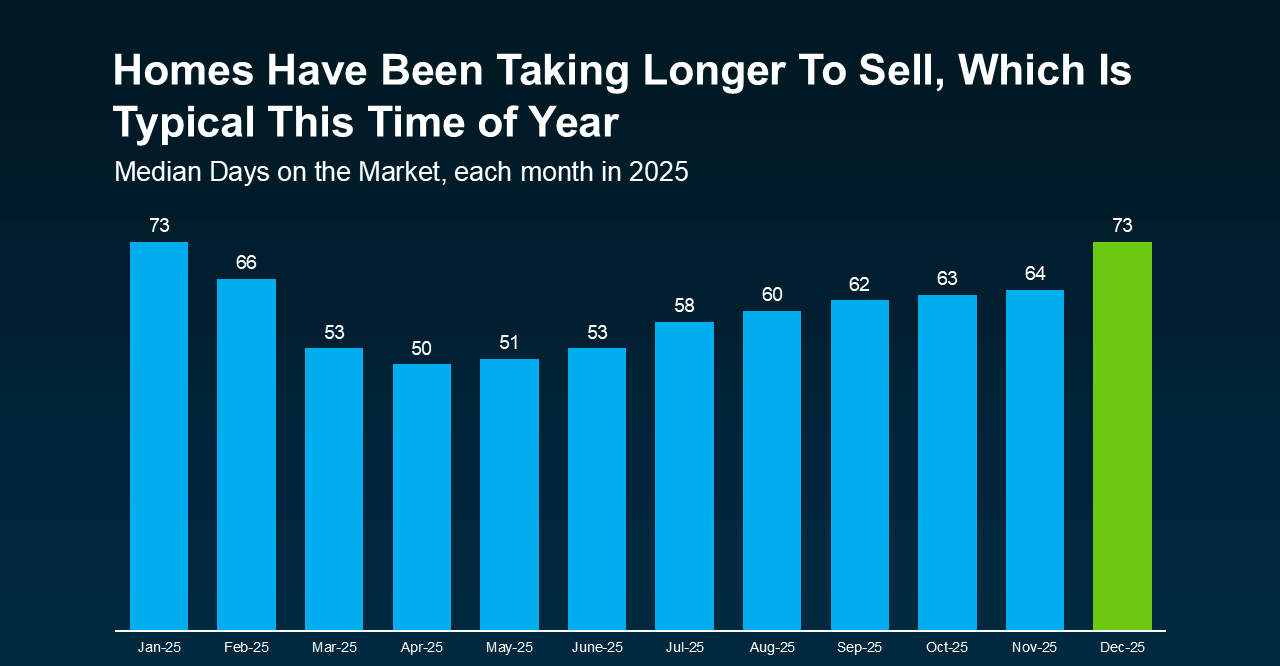

A few years ago, homes sold in just a matter of days. Sometimes, hours. Anything that lingered longer than that raised concerns. But that’s no longer the baseline.

Inventory has grown. Buyers have more choices. And homes are taking longer to sell across the board. Those are some of the reasons why the typical time it takes a home to sell has climbed this year.

And it’s not that 73 days is slow. That’s actually pretty normal for this time of year. It just feels slow because you heard so much about houses being snapped up in the buying frenzy a few years ago.

That shift alone explains a lot of what you’re seeing. It’s not necessarily that there’s anything wrong with the house itself. Although, let’s be honest, sometimes that is the case.

Most of the time today, a house that’s taking longer to sell simply means:

- There are a lot of homes for sale in that area

- The seller priced a little too high at first

- The home didn’t photograph as well online

- Buyers passed it over for flashier listings nearby

- The timing just wasn’t right when it first hit the market

None of those are necessarily deal-breakers.

What Buyers Often Get Wrong About These Listings

Because even though you may assume a house that hasn’t sold must have hidden issues, the reality is, that’s not always the case. And, if the house does have issues, it’ll show up quickly in your inspection.

That’s information you can use to negotiate. Not a reason to walk away automatically. And in many cases, that’s where buyers find the best deals.

The key is knowing which homes that have been sitting for a while are worth a second look – and which ones aren’t. That’s why working with a local agent makes a real difference. They’ll be able to look at disclosures and more to help you uncover hidden gems other buyers may overlook.

Bottom Line

A home sitting on the market isn’t always a warning sign. Sometimes it’s an overlooked opportunity.

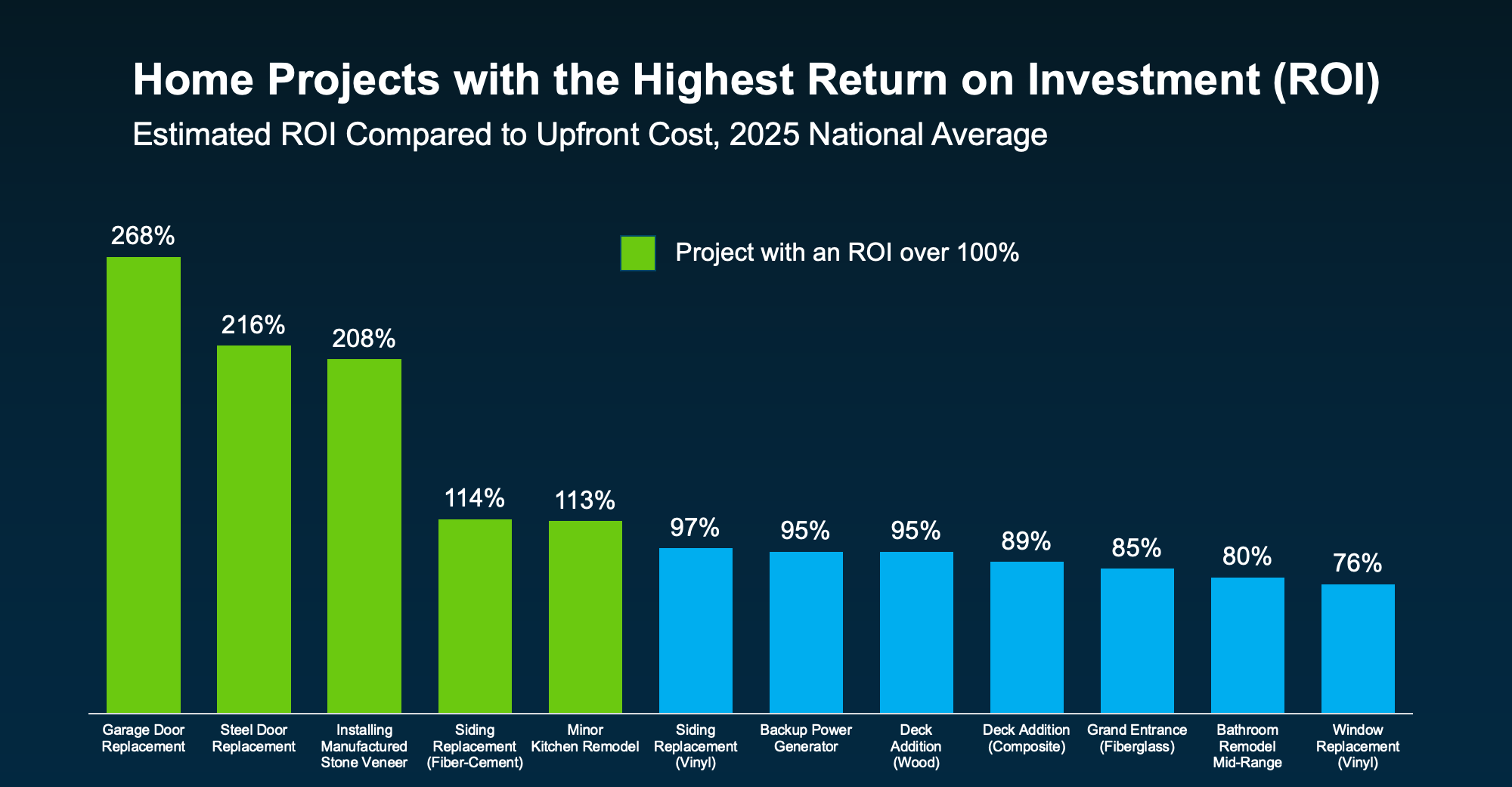

Home Updates That Pay Off When You Sell Your House

Planning to sell this spring? If so, starting your home updates sooner rather than later can make a real difference. While you may be tempted to wait until the first blooms appear or the spring showers hit, by today’s standards, that’s often waiting too long to get started.

Buyers have more options than they did a few years ago. Therefore, it’s worth it to tackle home updates now and make sure your house is set up to stand out. Because you don’t want to be caught scrambling right before the spring rush. Or, running out of time to do the work your house really needs.

The key is focusing on home improvements that actually matter. And that’s exactly where return-on-investment (ROI) data comes in handy.

Which Projects Tend to Pay Off?

Every year, Zonda looks at which home updates deliver the most bang for the buck when you go to sell the home. And the results can be a little surprising.

The green in the chart below shows the updates where sellers have the biggest potential to add value based on that research:

While there’s a wide range of projects represented in this data, the cool part is, some of the top winners aren’t big to-do’s. They’re just swapping out doors.

Small Updates, Big Visual Impact

This goes to show little projects can have a big impact. So, you don’t have to spend a fortune. And you don’t need to tackle everything on this list. But in today’s market, doing nothing can work against you.

Now that buyers have more homes to choose from, a lot of them are going to opt for what’s move-in ready.

The best advice? Focus on what your house needs, whether it’s listed here or not – like the home updates you’ve been putting off. A front door or shutters in need of a little TLC. Piles of leaves in the yard. Scuffed up paint where your kids play inside. Those details matter too.

Mallory Slesser, Interior designer and Home Stager, explains it to the National Association of Realtors (NAR) this way:

“If you’re looking for affordable updates that pack a punch, dollar for dollar, I would say painting; changing out light fixtures; changing out hardware; maybe new draperies or window treatments. Those are all cost-effective ways to make a big statement. It really changes the space.”

These seemingly small things help buyers focus on the home itself – not the work they think they’ll have to do after moving in. And that’s paying off for other sellers. Buyers are often willing to spend more on homes that feel well cared for, updated, and move-in ready.

This Chart Is a Starting Point, Not a Strategy

Here’s the important thing to remember. National data like this is a guideline. Buyer preferences are going to vary by location, price point, and even neighborhood. That means a project that boosts value in one area might be unnecessary (or even overkill) in yours.

That’s why the first step should always be to talk with a local real estate professional before you start.

An experienced agent can help you answer questions like:

- Which updates do buyers in your market expect?

- What can you skip without hurting your sale?

- Where will a small investment make the biggest difference?

- Is it better to update, or sell as-is?

That guidance helps you avoid over-improving and under-preparing.

Bottom Line

If you’re looking to sell this spring, you still have time to make updates that help your home stand out – without taking on a full renovation.

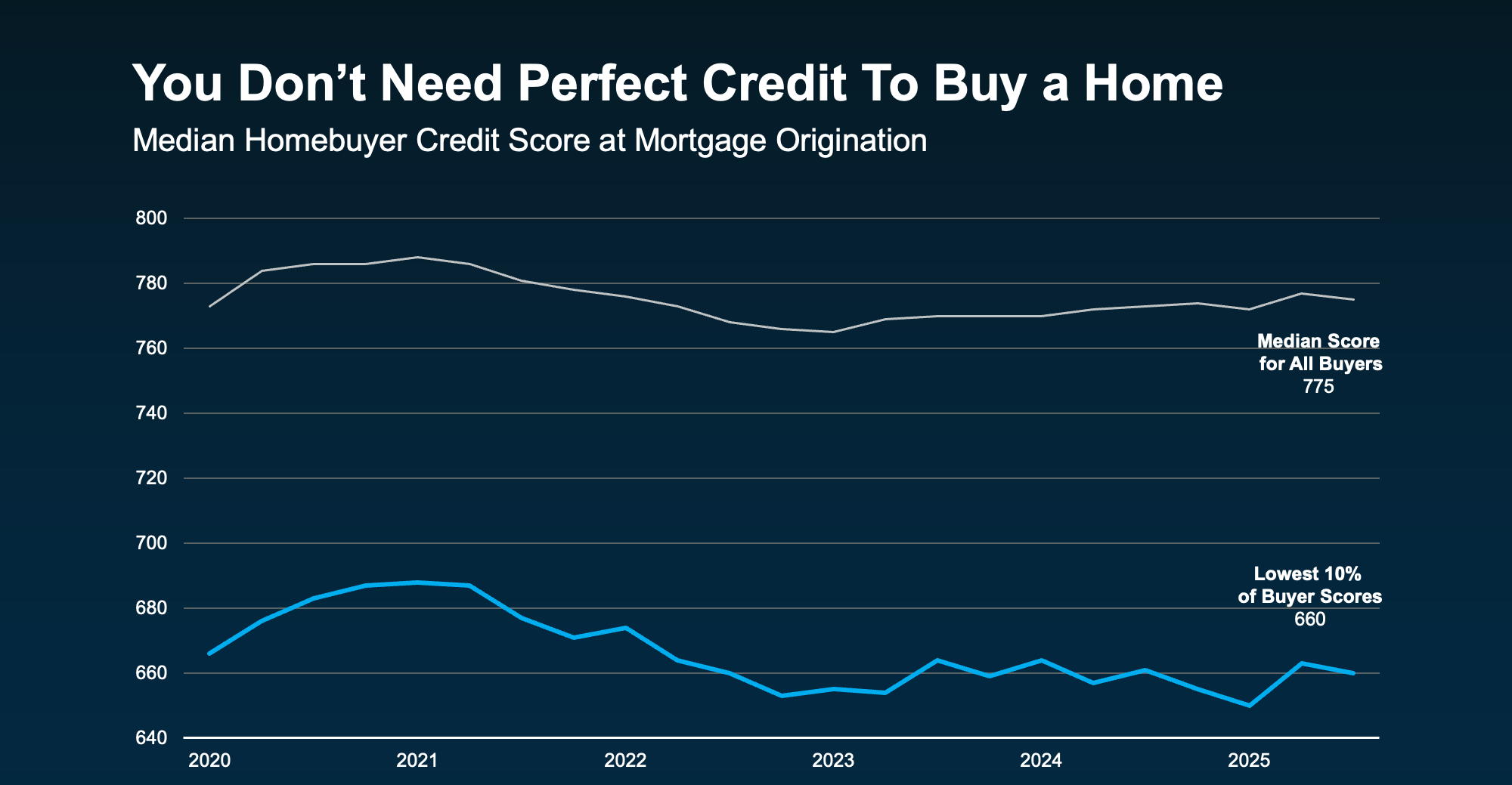

The Credit Score Myth Holding Buyers Back

Would-be homebuyers aren’t sitting on the sidelines because they don’t want to buy. They’re sitting out because they think they can’t. And sometimes, it’s their credit score that’s holding them back.

According to a Bankrate survey, 2 out of every 5 (42%) Americans believe you need excellent credit to qualify for a mortgage. That may be why, when renters are asked why they don’t own yet, “my credit isn’t good enough” comes up often.

Maybe you’re in the same boat. You look at your score, see it’s not where you want it to be, and assume buying your first place just isn’t realistic right now.

But here’s what you need to know.

Even though a lot of people assume you need flawless credit to buy a house, that’s not necessarily the case.

You Don’t Need Perfect Credit To Buy a Home

So, where’s this myth come from? Part of the confusion stems from the fact that the typical homebuyer today does have a fairly strong credit score. In fact, according to data from the NY Fed, the median credit score for all buyers is 775.

But that doesn’t mean you need a score that high to qualify.

Looking at recent homebuyers, a number were able to get a mortgage with scores below that threshold. Data shows 10% of scores were around 660. Which means some were higher than that and some were lower, but the median in that lowest 10th percentile was around that range (see graph below):

So, even if your score isn’t as high as you want, that doesn’t automatically close the door. FICO explains there is no universal credit score you absolutely have to have when buying a home:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single ‘cutoff score’ used by all lenders, and there are many additional factors that lenders may use . . .”

The best thing to do is to talk to a trusted lender to see what’s possible for you. Because a portion of buyers are buying with scores in the 600s – and maybe that means you can too.

Bottom Line

Your credit score is important. But that doesn’t mean it has to be perfect.

If credit has been the reason you’ve been waiting to buy a home, it might be time to take another look at your options. If you want help understanding where you stand and what your next step could be, connect with a local lender.

Reference: https://www.keepingcurrentmatters.com/2026/01/12/the-credit-score-myth-thats-holding-would-be-buyers-back/

{kind=link}