Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

2026 Housing Market Outlook

After a few years where the housing market seemed stuck in neutral, 2026 could finally be the year things pick up again. Experts are predicting that more people will be ready to move — and that could create new opportunities for you, too.

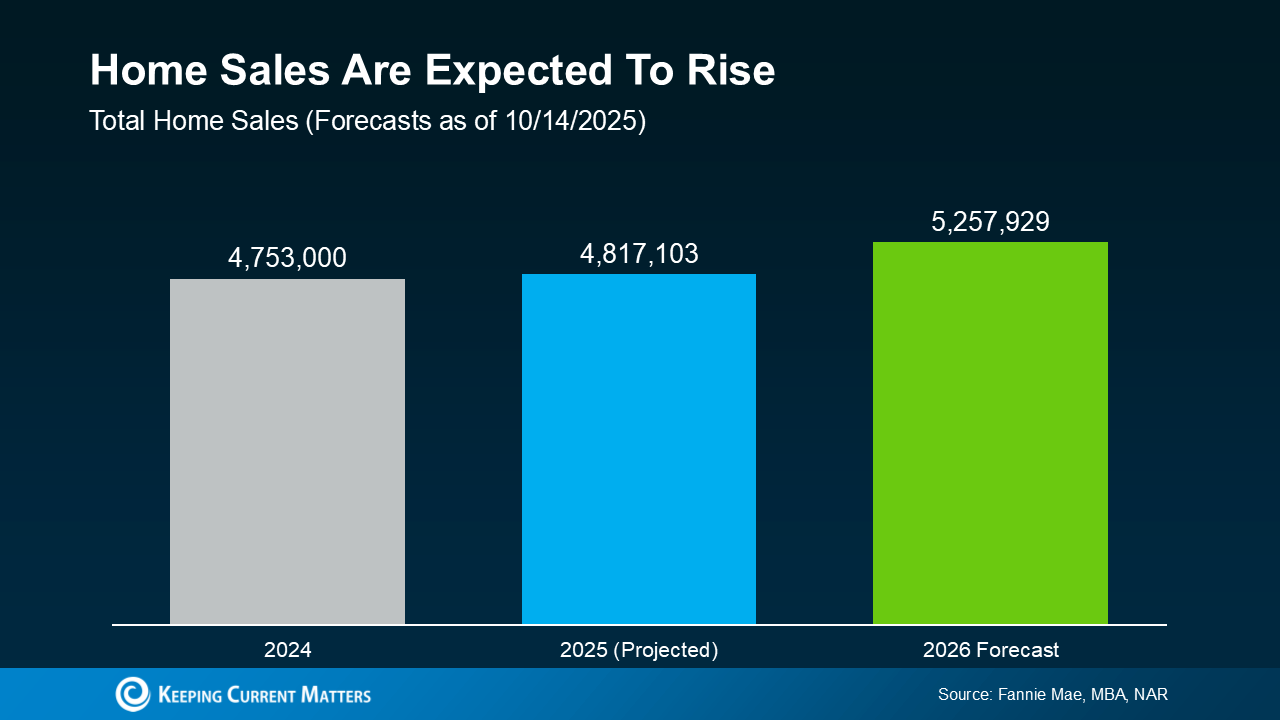

More Homes Expected To Sell

Over the past few years, many potential movers hit pause because of affordability challenges. But that pause can’t last forever — life happens, and people still need to relocate. Experts believe more of those moves will start happening in 2026 (see graph below):

What’s driving this change? Two major factors: mortgage rates and home prices. Let’s take a look at what experts are forecasting for both.

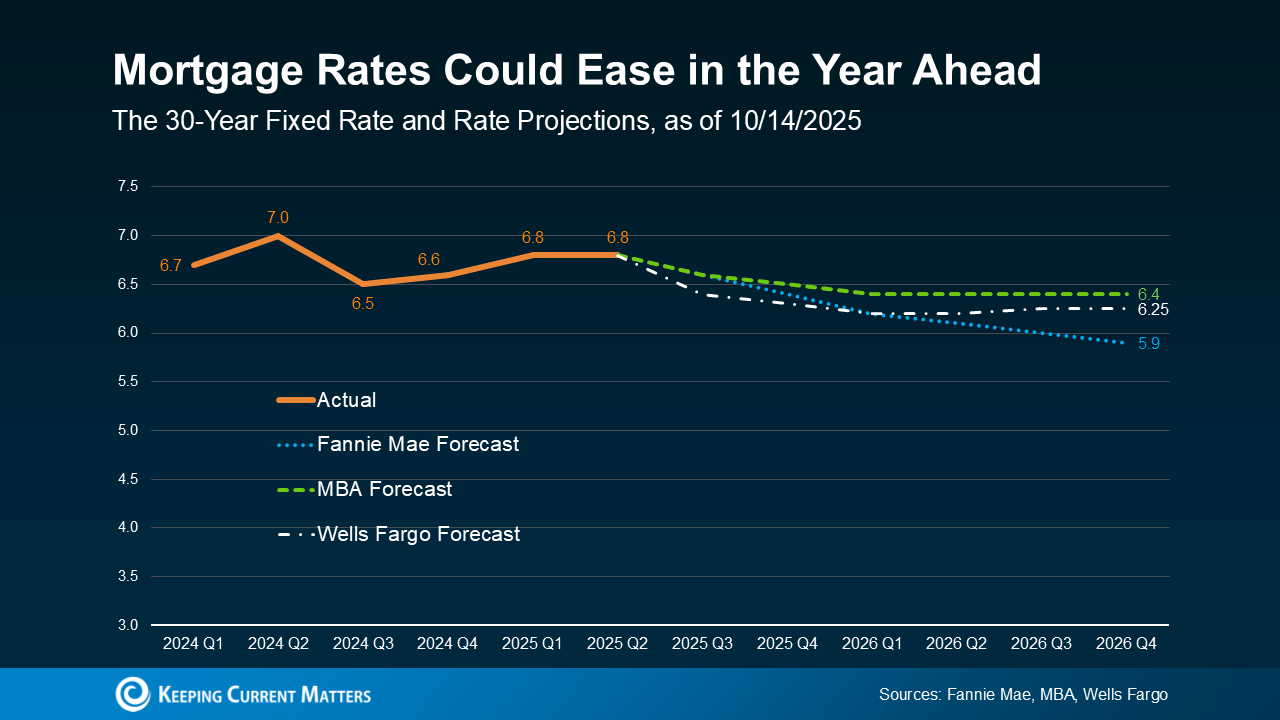

Mortgage Rates May Continue To Ease

One thing nearly every buyer has been hoping for is lower mortgage rates. After peaking around 7% earlier this year, rates have already started to come down — and that trend may continue into 2026 (see graph below):

As the saying goes: when rates go up, they take the escalator — but when they come down, they take the stairs. In other words, the path to lower rates will be gradual and sometimes uneven. Expect slight, steady improvements through next year, with some ups and downs along the way as new economic data comes out.

Even modest declines can make a noticeable difference. Compared to when rates were around 7%, today’s lower rates already mean hundreds of dollars in monthly savings for many buyers. That can make a real impact on affordability.

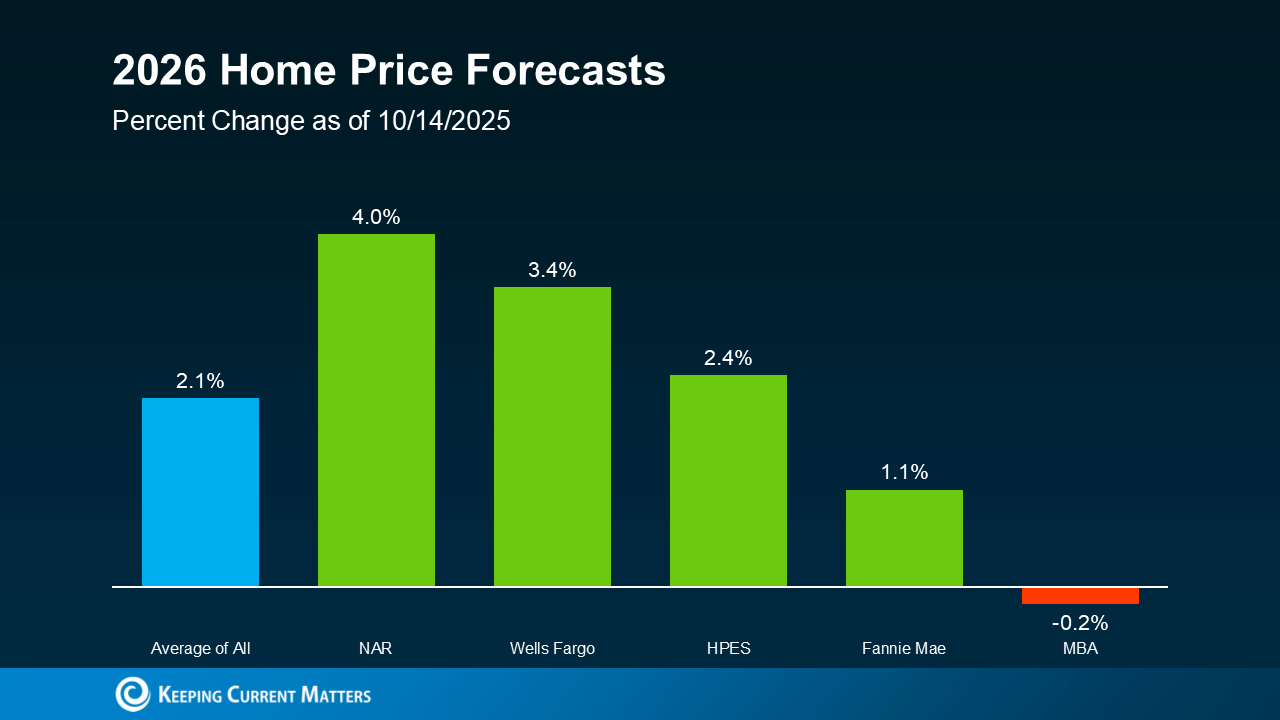

Home Prices Will Rise at a Steady Pace

What about home prices? Nationally, they’re projected to keep rising — just at a more moderate rate. With mortgage rates easing, more buyers will re-enter the market, which will keep demand strong enough to prevent major price drops.

While a few markets may experience slight declines, there’s no sign of a major crash. In fact, even areas seeing small dips are still up compared to several years ago.

Price trends will vary by location, depending on local inventory and demand, but overall, experts expect modest national appreciation (see graph below):

This moderation is actually good news. A steadier, more predictable rate of price growth makes it easier for buyers to plan — and gives more confidence that prices won’t spike overnight.

Bottom Line

After a slower stretch, 2026 is shaping up to be a year of renewed movement and opportunity. With sales likely to increase, mortgage rates easing, and price growth leveling out, the housing market could be headed toward a healthier balance.

So, the real question is: will 2026 be your year to make a move?

Connect with a trusted agent now to start preparing.

Why More Buyers Are Turning to New Construction This Year?

There’s a trend taking hold in real estate right now: more buyers are choosing newly built homes. And it’s not just about getting the latest technology or modern floorplans. It’s because they may be able to get a better deal.

Builders are offering serious incentives today, and people are jumping on them. In fact, new home sales just hit their highest level in over two years.

Why Builders Are Throwing in Perks

There are more newly built homes for sale right now than there have been in years. And as a buyer, that can help you in two big ways. It gives you more options to choose from on the market, and it motivates builders to sell their inventory before they build more.

That’s exactly why more buyers are scoring incentives like these:

- Mortgage rate buydowns to shrink your monthly payment

- Price cuts that make homeownership more attainable

- Help with closing costs and even upgrades in some communities

The best part is, a lot of builders are offering these perks right now. According to Zonda, nearly 6 out of 10 new home communities are doing incentives on to-be-built homes. And over 75% are doing the same for quick move-ins, which are homes that are already built and ready to move into. As real estate analyst Nick Gerli explains:

“. . . builders are adjusting to the realities of the current housing market. They’ve cut prices 13 percent from peak, and are giving generous mortgage rate buydowns on top of that.”

The big takeaway is: builders are motivated to sell. So, you could snag a lower price and maybe even a lower mortgage rate if you buy new. If you’ve been feeling priced out, these offers might be your way back in.

You Have More Brand-New Options Than Normal

Since there are more new homes on the market than usual, that gives you more options than you’ve had in years. Whether you’re looking for something turnkey or want to personalize a build, odds are there’s more available near you than you may realize.

Even though the number of new homes for sale is up throughout the country, there are pockets where you have an even better chance to find a better price. According to Census data, here’s a high-level look at which parts of the country are seeing the biggest boost in newly built homes.

Both the South and West have more new homes available, so you may find builders are even more willing to negotiate in these regions.

Just know that this opportunity won’t last forever. Recent data shows builders are slowing down their production efforts. And a lot of that is to avoid having too many homes for sale. As Robert Dietz, Chief Economist at the National Association of Home Builders (NAHB), explains:

“The slowdown in single-family home building has narrowed the home building pipeline. There are currently 621,000 single-family homes under construction, down 1% in July and 3.7% lower than a year ago. This is the lowest level since early 2021 as builders pull back on supply.”

Moving forward, the number of new options may start to shrink as builders focus more on selling what’s already built before they add more. So, the best time in years to buy a new home may actually be right now.

Bottom Line

With builders cutting prices and maybe even helping you score a lower monthly payment, that’s not something to overlook.

If you want to see how active builders are in your target area and what they’re offering, here’s your power move: before you even begin looking, connect with your own agent.

That way, you have someone to help you compare incentives from multiple builders and negotiate on your behalf, making sure you get the best deal possible.

Why Experts Say Mortgage Rates Should Ease Over the Next Year

You want mortgage rates to fall – and they’ve started to. But is it going to last? And how low will they go?

Experts say there’s room for rates to come down even more over the next year. And one of the leading indicators to watch is the 10-year treasury yield. Here’s why.

The Link Between Mortgage Rates and the 10-Year Treasury Yield

For over 50 years, the 30-year fixed mortgage rate has closely followed the movement of the 10-year treasury yield, which is a widely watched benchmark for long-term interest rates

When the treasury yield climbs, mortgage rates tend to follow. And when the yield falls, mortgage rates typically come down.

It’s been a predictable pattern for over 50 years. So predictable, that there’s a number experts consider normal for the gap between the two. It’s known as the spread, and it usually averages about 1.76 percentage points, or what you sometimes hear as 176 basis points.

The Spread Is Shrinking

Over the past couple of years, though, that spread has been much wider than normal. Why? Think of the spread as a measure of fear in the market. When there’s lingering uncertainty in the economy, the gap widens beyond its usual norm. That’s one of the reasons why mortgage rates have been unusually high over the past few years.

But here’s a sign for optimism. Even though there’s still some lingering uncertainty related to the economy, that spread is starting to shrink as the path forward is becoming clearer.

And that opens the door for mortgage rates to come down even more. As a recent article from Redfin explains:

“A lower mortgage spread equals lower mortgage rates. If the spread continues to decline, mortgage rates could fall more than they already have.”

The 10-Year Treasury Yield Is Expected To Decline

It’s not just the spread, though. The 10-year treasury yield itself is also forecast to come down in the months ahead. So, when you combine a lower yield with a narrowing spread, you have two key forces potentially pushing mortgage rates down going into next year.

This long-term relationship is a big reason why you see experts currently projecting mortgage rates will ease, with a fringe possibility they’ll hit the upper 5s toward the end of next year.

Here’s how it works. Take the 10-year treasury yield, which is sitting at about 4.09% at the time this article is being written, and then add the average spread of 1.76%. From there, you’d expect mortgage rates to be around 5.85%.

But remember, all of that can change as the economy shifts. And know for certain that there will be ups and downs along the way.

How these dynamics play out will depend on where the economy, the job market, inflation, and more go from here. But the 2026 outlook is currently expected to be a gradual mortgage rate decline. And as of now, things are starting to move in the right direction.

Bottom Line

Keeping up with all of these shifts can feel overwhelming. That’s why having an experienced agent or lender on your side matters. They’ll do the heavy lifting for you.

If you want real-time updates on mortgage rates, reach out to a trusted agent or lender who can keep you in the loop and help you plan your next move.

Should You Still Expect a Bidding War?

If you’re still worried about having to deal with a bidding war when you buy a home, you may be able to let some of that fear go.

While multiple-offer situations haven’t disappeared entirely, they’re not nearly as common as they used to be. In fact, a recent survey shows agents reported only 1 in 5 homes (20%) nationally received multiple offers in June 2025.

That’s down from nearly 1 in 3 (31%) just a year ago – and dramatically lower than in June 2023 (39%)

This trend means you should face less competition when you buy. That gives you more time to make decisions and the ability to negotiate price or terms.

It Still Depends on Where You’re Buying

Of course, national trends don’t tell the full story. Local dynamics matter, a lot. This second graph uses survey data from John Burns Research & Consulting (JBREC) and Keeping Current Matters (KCM) to break things down by region to prove just how true that is. It shows, while the share of homes getting multiple offers has dropped pretty much everywhere, some areas are still seeing more offers than others:

In the Northeast, 34% of homes (roughly 1 in 3) are still receiving multiple offers. That’s more than the national average. But in Southeast, that number drops to just 6%.

What’s behind the difference? In general, the areas still seeing bidding wars tend to have lower-than-normal inventory. That imbalance between buyers and available homes keeps pressure on prices and competition. But markets with more listings are seeing conditions cool – and that means fewer bidding wars.

Sellers Are More Flexible Than You Might Think

Here’s another shift to show you just how much things have changed. According to a Redfin report, almost half of sellers are offering concessions, like covering their buyer’s closing costs or dropping their asking price to get their house sold.

That’s a clear sign this isn’t the same ultra-competitive market we saw a few years ago. Back then, sellers rarely compromised. And buyers often waived their inspection or appraisal to try to make their offer stand out. Now, things are different.

But again, how often this is happening is going to vary based on where you’re looking to buy. And that’s why you need a local agent’s expertise.

Bottom Line

If concerns about bidding wars have been holding you back, it may be time to take another look. Nationally, competition is down. In some markets, it’s down significantly. And with more sellers offering concessions, buyers today have more power and flexibility than they’ve had in a long time.

Want to find out what the market looks like where you’re buying? Connect with a local agent.

Do You Know How Much Your House Is Really Worth?

When was the last time you checked your home’s value?

If you’re like most homeowners, probably not as often as you should. And here’s why that matters: your home is likely the biggest financial asset you own — and it’s been quietly growing your wealth in the background.

What’s Home Equity?

Home equity is the difference between what your house is worth today and what you still owe on your mortgage. For example: if your home is worth $500,000 and you owe $200,000, you’ve got $300,000 in equity. That’s real wealth you can use.

In fact, the average homeowner today has around $302,000 in equity, according to CoreLogic.

Why You Probably Have More Than You Think

Home prices have soared. Over the past five years, prices are up nearly 54% nationwide. Even with some recent market shifts, long-time homeowners are still sitting on big gains.

People are staying put longer. The typical homeowner stays in their home for about 10 years. That’s a decade of paying down your loan and watching your home’s value climb.

The result? On average, homeowners have gained $201,600 in wealth over the past 10 years just from rising prices.

What Can You Do with Your Equity?

Move Up: Use it as a down payment (or even all cash) for your next home.

Renovate: Upgrade your space and add even more value.

Invest in Your Dreams: Start a business, pay for education, or boost your retirement savings.

👉Bottom Line

Your house isn’t just where you live — it’s a wealth-building tool. If you’re curious about how much equity you have, reach out to a trusted local agent. You might be surprised at how much your home is really worth.

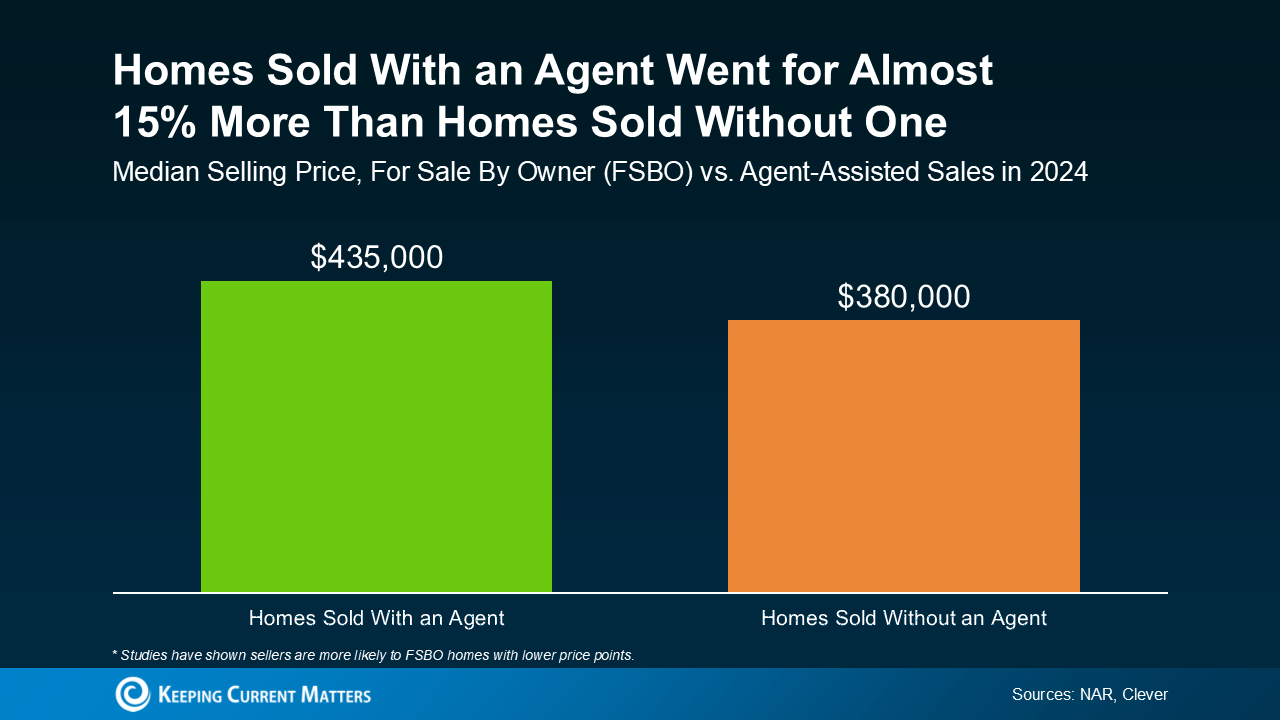

Why Selling Without an Agent Can Cost You More Than You Think

Thinking of selling your house without an agent to “save” on commission? Here’s the truth: it could actually cost you more.

💡 Last year, homes sold with an agent went for nearly 15% more than those sold by owners alone. That’s a big gap you don’t want to leave on the table.

This Isn’t the Market for DIY Selling

A few years back, putting up a “For Sale By Owner” sign might have worked. Homes were flying off the market, and buyers were competing hard.

But today, things look different. There are more homes for sale than we’ve seen in years, which means buyers have options. If your listing doesn’t shine with the right price, photos, and marketing, it can easily get skipped.

More Homes = More Competition

With more inventory out there, you need more than a sign and some snapshots. You need:

-

The right pricing strategy

-

Expert prep and staging advice

-

Professional marketing and exposure

-

Skilled negotiation to protect your bottom line

Without these, chances are you’ll end up losing money instead of saving it.

Why More Sellers Are Turning to Pros

The numbers speak for themselves: fewer homeowners are selling on their own than ever before. In fact, 21% of FSBO sellers eventually hired an agent after struggling to get the job done.

Bottom Line

In today’s market, an agent isn’t optional—it’s essential. If you want to sell for the best possible price (without stress or regrets), start with a local pro who knows exactly what works right now.

👉 Ready to find out what your house could sell for today? Reach out for a professional assessment and let’s get started.

Let’s connect to find out how I can help you find your perfect home with the best deal possible.

Builder Incentives Reach 5-Year High

Even with more homes on the market right now, some buyers are still having a tough time finding the right one at the right price. Maybe the layout feels off. Maybe it still needs some updating. Or maybe it’s just more of the same.

That’s why more buyers are turning to new construction – and finding some of the best deals available today.

Why? Today, many builders have more homes that are finished and sitting on the market than normal. And that means they’re motivated to sell. They’re running a business, and they don’t want to sit on their inventory. They want to sell it before they build more homes. And that can definitely work in your favor.

As Lance Lambert, Co-Founder of ResiClub, puts it:

“In housing markets where unsold completed inventory has built up, many homebuilders have pulled back on their spec builds—and many are doing bigger incentives or outright price cuts to move unsold inventory.”

Incentives Are the Highest They’ve Been in 5 Years

Data from the National Association of Home Builders (NAHB) shows 66% of builders offered sales incentives in August. That’s the peak so far this year, and the highest percentage we’ve seen in 5 years.

Why This Matters for You

As a buyer, you probably have a clear vision for your ideal home. Because you’re not just buying any house. You’re buying your house. The one with the space, features, and lifestyle you’ve been hoping for. New builds can check those boxes since they usually have:

- Bigger kitchens and open layouts

- Energy efficiency (hello lower utility bills)

- Smart-home upgrades

- Fewer repair headaches on day one

And today’s incentives make buying a new home more attainable than it’s been in years.

One Word of Advice: Don’t Go At It Alone

If you want to take advantage of this opportunity, just be sure to use your own agent. Builder reps aren’t there to save you money. They protect the builder’s bottom line. That’s why you need to bring your agent with you. Your agent will:

- Cut through the sales pitch and run the cold hard numbers

- Spot which incentives are actually worth it (and which ones are fluff)

- Handle negotiations so you walk away with the best deal possible

- Keep your best interest as their top priority

Bottom Line

If you’re not finding a home you love, the new home market is buzzing with opportunity. With record-high incentives, price cuts in play, and builders itching to move inventory, this is the best time in years to buy new construction.

Curious how far today’s incentives could stretch your budget? Connect with an agent to see what builders are offering in your area.

Thinking About Renting Your House Instead of Selling? Read This First.

If your house is on the market but you haven’t gotten any offers you’re comfortable with, you may be wondering: what do I do if it doesn’t sell? And for a growing number of homeowners, that’s turning into a new dilemma: should I just rent it instead?

There’s a term for this in the industry, and it’s called an accidental landlord. Here’s how Yahoo Finance defines it:

“These ‘accidental landlords’ are homeowners who tried to sell but couldn’t fetch the price they wanted — and instead have decided to rent out their homes until conditions improve.”

Why This Is Happening More Often Right Now

And right now, the number of homeowners turning into accidental landlords is rising. Business Insider explains why:

“While there have always been accidental landlords . . . an era of middling home sales brought on by a steep rise in borrowing rates — is minting a new wave of reluctant rental owners.”

Basically, sales have slowed down as buyers struggle with today’s affordability challenges. And that’s leaving some homeowners with listings that sit and go stale. And if they don’t want to drop their price to try to appeal to buyers, they may rent instead.

But here’s the thing you need to remember if renting your house has crossed your mind. Becoming a landlord wasn’t your original plan, and there’s probably a reason for that. It comes with a lot more responsibility (and risk) than most people expect.

So, if you find yourself toying with that option, ask yourself these questions first:

1. Does Your House Have Potential as a Profitable Rental?

Just because you can rent it doesn’t mean you should. For example:

- Are you moving out of state? Managing maintenance from far away isn’t easy.

- Does the home need repairs before it’s rental-ready? And do you have the time or the funds for that?

- Is your neighborhood one that typically attracts renters, and would your house be profitable as one?

If any of those give you pause, it’s a sign selling might be the better move.

2. Are You Ready To Be a Landlord?

On paper, renting sounds like easy passive income. In reality, it often looks more like this:

- Midnight calls about clogged toilets or broken air conditioners

- Chasing down missed rent payments

- Damage you’ll have to fix between tenants

As Redfin notes:

“Landlords have to fix things like broken pipes, defunct HVAC systems, and structural damage, among other essential repairs. If you don’t have a few thousand dollars on hand to take care of these repairs, you could end up in a bind.”

3. Have You Thought Through the True Costs?

According to Bankrate, here are just a few of the hidden costs that come with renting out your home:

- A higher insurance premium (landlord insurance typically costs about 25% more)

- Management fees (if you use a property manager, they typically charge around 10% of the rent)

- Maintenance and advertising to find tenants

- Gaps between tenants, where you cover the mortgage without rental income coming in

All of that adds up, fast.

While renting can be a smart move for the right person with the right house, if you’re only considering it because your listing didn’t get traction, there may be a better solution: talking to your current agent and revisiting the pricing strategy on your house first.

With their advice you can rework your strategy, relaunch at the right price, and attract real buyers to make the sale happen.

Bottom Line

Before you decide to rent your house, make sure to carefully weigh the pros and cons of becoming a landlord. For some homeowners, the hassle (and the expense) may not be worth it.

Why Selling Without an Agent Can Cost You More Than You Think

Cutting out a real estate agent may sound like a smart way to save money when selling your home—but the numbers tell a different story.

Last year, homes sold with an agent closed for nearly 15% more than those sold without one. That’s a pretty big gap to ignore. And with inventory rising and competition heating up, trying to go the DIY route could end up costing you more than you think.

Why FSBO Doesn’t Work Like It Used To

A few years ago, sticking a “For Sale By Owner” sign in the yard might’ve worked. Homes were flying off the market, and buyers were competing hard. But today, things look very different.

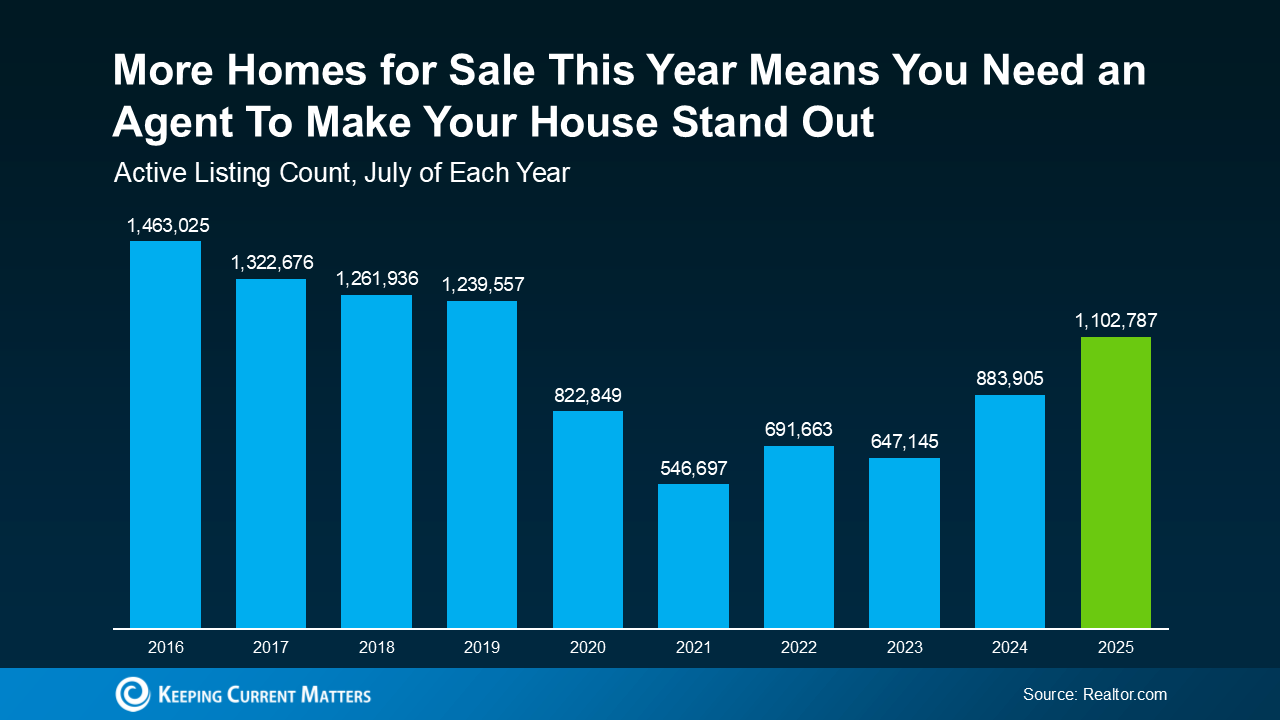

The housing market is balancing out, with more homes available than we’ve seen in years. In fact, according to Realtor.com, the number of active listings this July was the highest for that month since 2019.

That means buyers now have options—and they’re more selective. If your home doesn’t stand out in terms of price, condition, photos, and presentation, it risks being overlooked.

More Listings = More Competition

Selling today isn’t about throwing your home online and waiting for offers. It takes:

-

A sharp pricing strategy to capture attention

-

Professional staging and prep work

-

Marketing that actually reaches buyers

-

Strong negotiation skills to protect your bottom line

Without those, chances are you’ll walk away with less.

Why More Sellers Are Choosing Agents

It’s no surprise that fewer homeowners are going it alone. NAR data shows FSBO sales hit a record low last year. And even among those who tried, many ended up hiring an agent later—Zillow reports 21% switched to a pro after struggling to sell on their own.

Working with an agent gives you:

-

Accurate pricing that attracts serious buyers

-

Expert guidance on staging and presentation

-

Access to powerful marketing and buyer networks

-

Skilled negotiation through offers and inspections

-

Local market knowledge that helps your home shine

Bottom Line

With today’s market dynamics, an agent’s expertise isn’t just helpful—it’s essential. If you’re thinking about selling, don’t leave money on the table.

Start with a professional who knows exactly how to position your home for the best possible price.

👉 Reach out to a local agent today for an expert assessment of what your home could sell for right now.

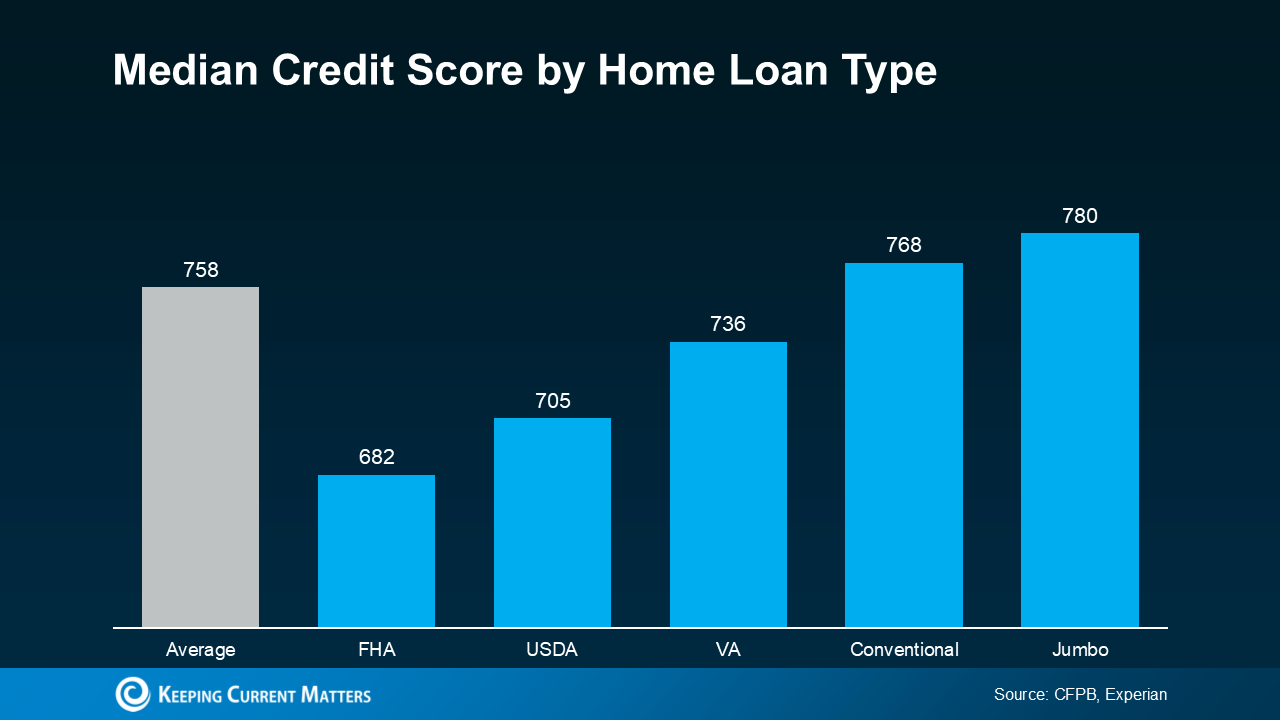

What Credit Score Do You Really Need To Buy a Home?

According to Fannie Mae, 90% of buyers don’t actually know what credit score lenders are looking for, or they overestimate the minimum needed.

Let that sink in. That means most homebuyers think they need better credit than they really do – and maybe you’re one of them. That misconception could make you believe buying a home is out of reach right now, even if that’s not necessarily the case. So, let’s look at what the data really says about credit scores and homebuying.

There’s No One Magic Number

There isn’t a universal credit score you absolutely must have to buy a home. That means there’s more flexibility than most people realize. Check out this graph showing the median credit scores recent buyers had for different home loan types:

📊 a graph of a credit score

Here’s the key takeaway: the numbers vary, and there’s no one-size-fits-all threshold. That could open doors you thought were closed. The best way to learn more is to talk to a trusted lender. As FICO explains:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single ‘cutoff score’ used by all lenders, and there are many additional factors that lenders may use . . .”

Why Your Score Still Matters

When you buy a home, lenders use your credit score to gauge how reliable you are with money. They want to know if you make payments on time, pay back debts, and handle your finances responsibly.

Your score can influence which loan types you qualify for, the terms of those loans, and even your mortgage rate. And since your mortgage rate plays a big role in how much house you can afford, your score feels even more important today. As Bankrate says:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

That doesn’t mean your credit has to be perfect. Even if your score isn’t where you’d like it to be, you may still be able to qualify for a mortgage.

Want To Boost Your Score? Start Here

If you talk to a lender and decide you want to improve your score (and hopefully your loan options too), here are a few smart moves according to the Federal Reserve Board:

-

Pay Your Bills on Time: This is huge. From credit cards to utilities and cell phone bills, consistent on-time payments show lenders you’re dependable.

-

Pay Down Your Debt: The less of your available credit you’re using, the better. Keeping this ratio low signals to lenders that you’re a lower-risk borrower.

-

Review Your Credit Report: Get copies of your report and dispute any errors. Correcting mistakes can give your score a boost.

-

Don’t Open New Accounts: Opening multiple new credit cards may seem helpful, but it can backfire. Too many new applications lead to hard inquiries, which can temporarily lower your score.

Bottom Line

Your credit score doesn’t have to be perfect to qualify for a home loan. But improving it can help you secure better terms. The best way to know where you stand and explore your mortgage options is to connect with a trusted lender.

{kind=link}