Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Saving for a down payment can often feel like the biggest obstacle to buying a home. With affordability still a challenge in many markets, it’s easy to wonder how buyers are making homeownership happen.

The good news is that many are getting into the market with smaller down payments than you might expect.

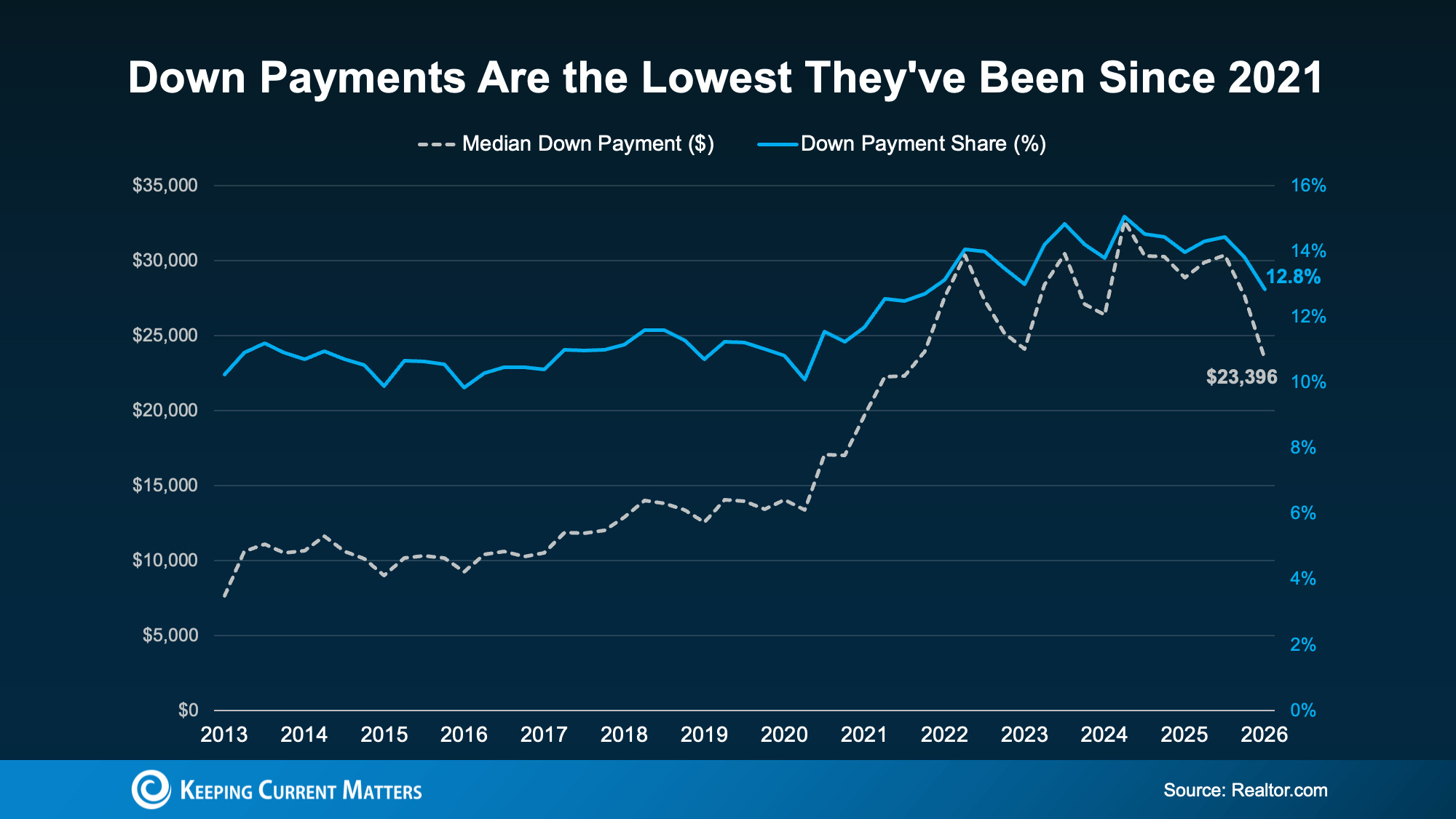

According to Realtor.com, the typical homebuyer put down about $23,400 in early 2026. That’s roughly $5,000 less than the average down payment a year earlier, representing a 19% year over year decrease. In fact, it’s the lowest typical down payment seen since 2021 (see graph below).

So why are buyers putting less money down, and how can you put less down, too? Here’s your answer.

Why Down Payments Are Getting Smaller

Several factors are contributing to this trend:

A More Balanced Housing Market

As the market becomes more balanced, buyers are facing less competition than they did a few years ago. That means there’s less pressure to make a larger down payment just to strengthen an offer.

Slower Home Price Growth

Since your down payment is based on a percentage of the home’s purchase price, slowed price appreciation can reduce the amount you need upfront. In many markets, home prices have stabilized, and some have even seen slight declines, making smaller down payments more achievable.

More Buyers Choosing Low Down Payment Loan Programs

Many homebuyers are taking advantage of government-backed loan options, such as FHA and VA loans, which often require little or even no money down. According to Mortgage Professional America, FHA loans have accounted for more than 24% of purchase mortgages for five consecutive quarters, while VA loans recently reached their highest market share in over a decade.

Even so, a down payment is still a significant expense, and saving for it isn’t always easy. That’s why many buyers rely on down payment assistance programs or financial support from family members to help bridge the gap.

Help You May Not Know You Qualify For

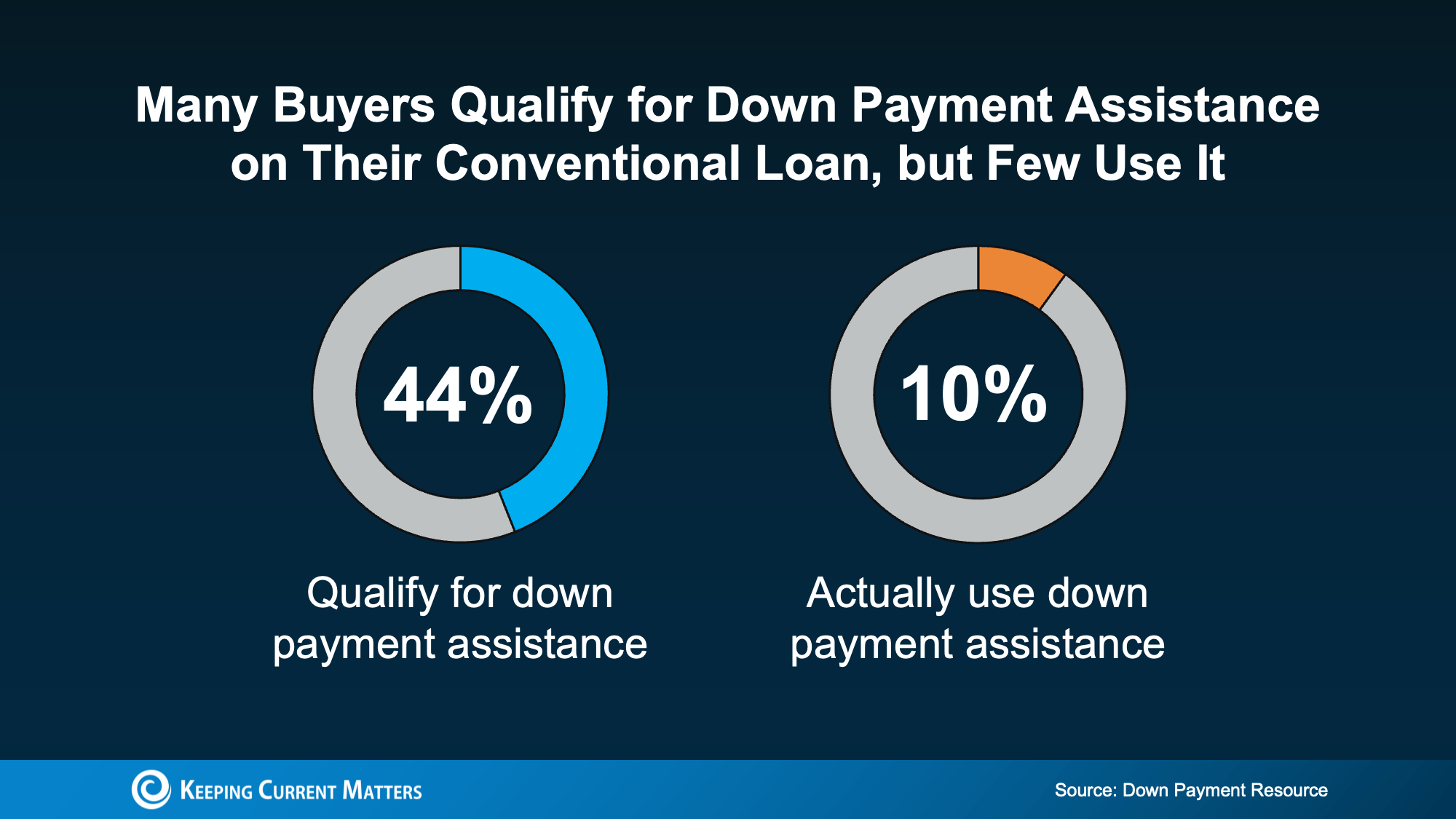

Down payment assistance is one of the most overlooked tools out there. Looking at the 10 largest U.S. metros, Urban Institute and Down Payment Resource found nearly 44% of recent buyers already qualified for a down payment program, but many of them closed on their loan without tapping the help (see chart below):

The options are broader than you might assume, too. According to Down Payment Resource:

- There are more than 2,600 down payment assistance programs available

- More than half (62%) are designed to help first-time buyers

- 38% have no first-time buyer requirement, so you may qualify even if you’ve owned before

- 62% are open to buyers earning $100,000 or more

A Helping Hand from Family

For many homebuyers, financial support starts with family. According to Veterans United, about 59% of parents have either helped or plan to help their children purchase a home.

That assistance most often goes toward the down payment, but it can also help with qualifying for a mortgage or covering closing costs. As Chris Birk, Vice President of Mortgage Insight at Veterans United, explains:

“For many families, helping a child buy a home has become less of an optional gesture and more of a practical response to today’s affordability challenges.”

If your loved ones are in a position to help, that support could make it possible to achieve homeownership sooner than you expected.

Bottom Line

Down payments are smaller than they’ve been in years, making homeownership more attainable for many buyers.

When you combine lower down payment options with down payment assistance programs and support from family, there may be more paths to homeownership than you realize. The best place to start is by connecting with a trusted lender who can help you explore your options and find the loan program that fits your needs.

{kind=link}