Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

You’ve probably found yourself wondering lately: Is buying a home even worth it right now? It’s a question more and more people are asking.

With current home prices and mortgage rates, renting can feel like the simpler route. In some situations, it might even seem like the only practical choice for now. And if that’s where you are, that’s completely okay.

But if you’re trying to decide, there’s one important part of the conversation that often gets overlooked.

It’s how each option impacts your future.

What Renting Really Offers (And What It Doesn’t)

Depending on your situation, renting does come with some advantages:

Lower upfront expenses.

Less maintenance and responsibility.

Greater flexibility to move when needed.

But even with those perks, a Bank of America survey shows that 70% of future homeowners are concerned about what long-term renting means for their future. And that concern comes down to one key issue: you’re not building anything over time. As Yahoo Finance puts it:

“Paying rent doesn’t build equity. You get a place to live, but no ownership stake, no price appreciation, and no asset to leverage for future borrowing or investment.”

So while renting may feel more convenient, that flexibility often comes at a long-term cost.

How Homeownership Builds Wealth Over Time

On the other hand, owning a home remains one of the most reliable ways to build wealth. Why? Because as a homeowner, you build equity—the difference between your home’s value and what you still owe on it.

That equity grows with every payment you make. It can also increase as property values rise over time—and it adds up faster than many people expect.

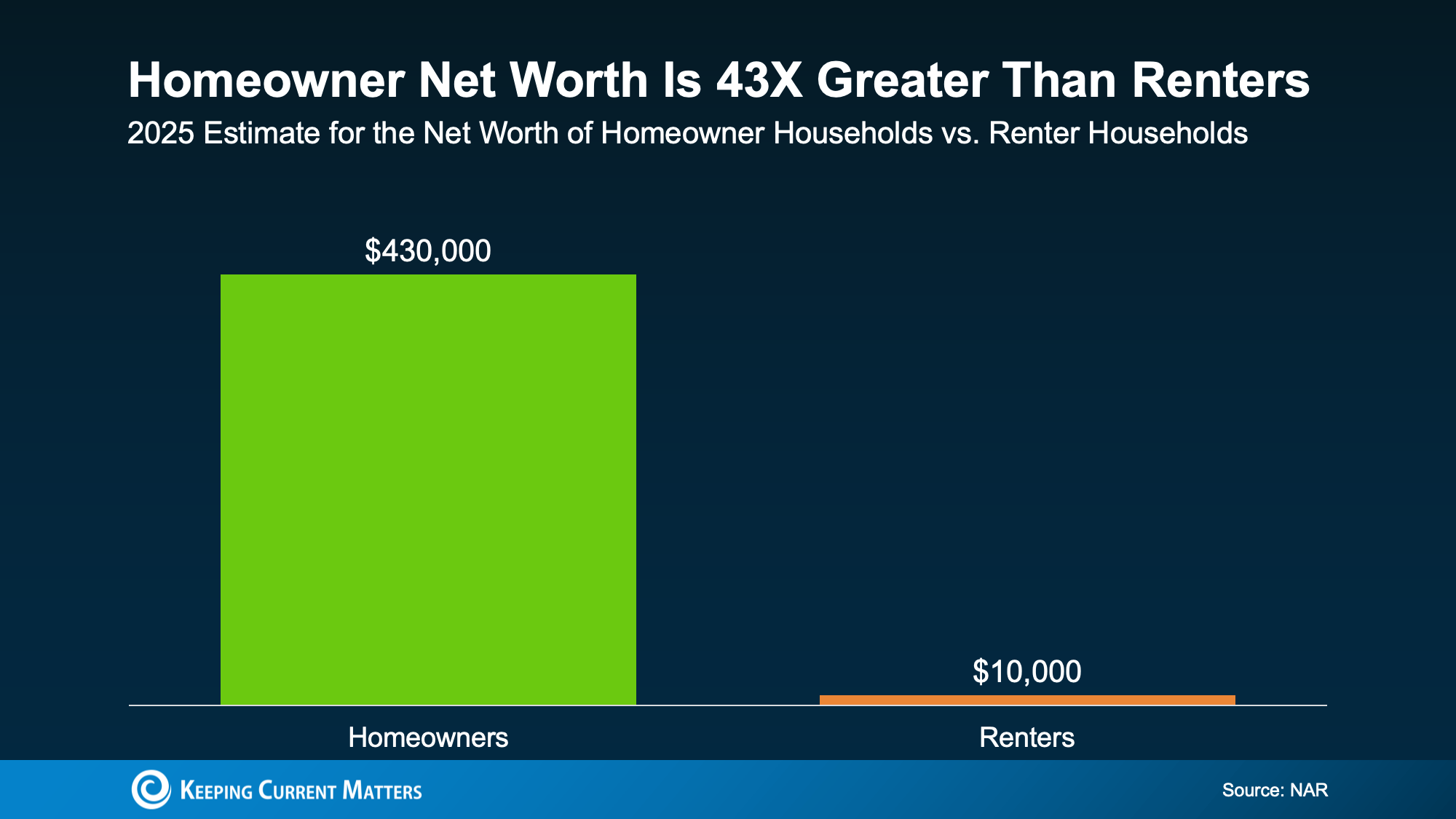

According to the National Association of Realtors (NAR), the average homeowner’s net worth is 43 times higher than that of a renter:

a graph of a number of people

The numbers speak for themselves. On average, here’s how net worth compares:

Homeowners: $430k

Renters: $10k

It’s not because homeowners make drastically different day-to-day choices. It’s because over time, one path builds wealth—and the other doesn’t.

So yes, buying comes with upfront costs and added responsibility. But it also functions like a savings account you live in.

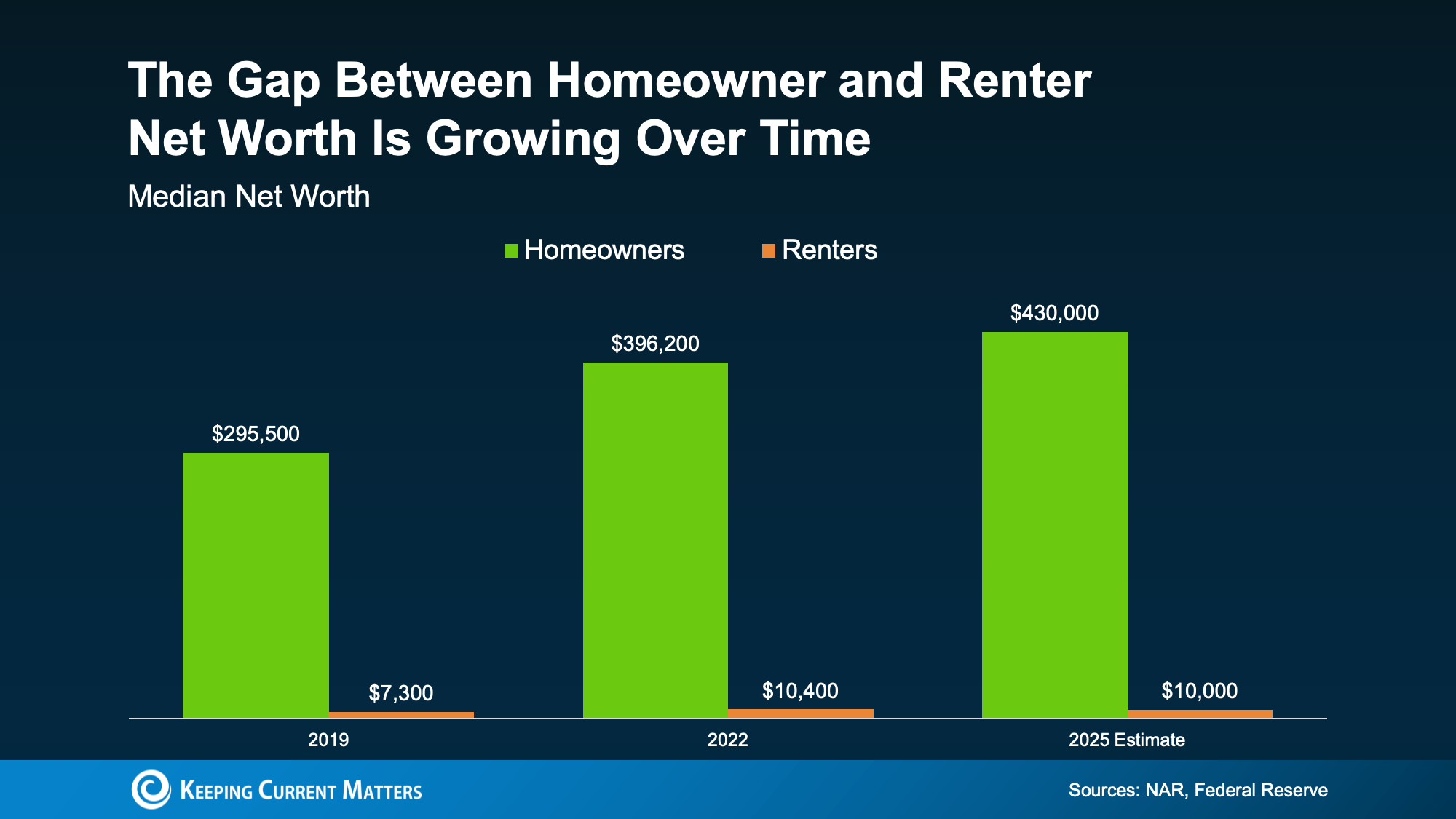

The Gap Continues to Grow

There’s another important point to consider. The net worth gap between homeowners and renters has been increasing over time—not shrinking.

Looking at historical data, the gap keeps widening as homeowners continue building wealth while renters remain in place (see graph below):

a graph of green and blue bars

Even in 2025, when home price growth slowed, homeowners still gained ground. And that highlights something important:

When you’re financially ready and able to take on the responsibility, history shows that buying is typically worth it in the long run. Because either way, you’re contributing to a mortgage—just not always your own.

When you rent, you’re paying your landlord’s mortgage. When you own, your payments build your own equity.

So the real question becomes: whose investment do you want to support—yours or someone else’s?

So, Should You Buy a Home Now?

The honest answer is: it depends on your situation.

While the long-term advantages of homeownership are clear, that doesn’t mean it’s the right time for everyone. And that’s perfectly fine. You should only buy when you’re financially ready and comfortable with the commitment.

Whether you’re ready now or planning ahead, the first step is the same. Have a quick conversation with a local real estate agent about your goals, timeline, and budget.

They can help you break down the numbers and see what’s possible. You might find that buying is more within reach than you expected. And if not, you’ll walk away with a clear plan to get there.

Because having a plan puts you in control—instead of constantly wondering if or when it will happen.

Bottom Line

Renting may feel more manageable today—but over time, it could cost you.

If your goal is to move beyond renting and start building for your future, it begins with a simple conversation. Connect with a real estate agent to discuss your goals and explore your options—so you’re ready when the timing is right.

{kind=link}