Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

If you’ve been searching for a home recently, you’ve probably noticed how challenging affordability still is. That’s exactly why more buyers are turning to adjustable-rate mortgages, or ARMs.

Here’s what you should know about how they work—and whether they might be right for you.

What Is an Adjustable-Rate Mortgage?

Since many people aren’t as familiar with this type of loan, let’s start with a simple explanation. Here’s how Business Insider describes the key difference between a fixed-rate mortgage and an adjustable-rate mortgage:

“With a fixed-rate mortgage, your interest rate stays the same for the entire life of the loan, keeping your monthly payment consistent over time . . . adjustable-rate mortgages work differently. You begin with a set rate for a few years, but after that, your rate can change at regular intervals. This means your payment could go up if rates rise, or go down if rates fall.”

In short, one remains stable over time.

And the other can fluctuate—sometimes slightly, sometimes significantly.

Of course, factors like taxes or homeowner’s insurance can still impact a fixed-rate loan. But overall, the base mortgage payment tends to stay consistent. With an ARM, however, your monthly payment can change as rates adjust.

Why Adjustable-Rate Mortgages Are Getting More Attention

So why are more buyers considering this option? It comes down to upfront savings. Business Insider explains:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers improve affordability when rates are high. A lower ARM rate can mean a smaller monthly payment or the ability to afford a more expensive home compared to a fixed-rate loan.”

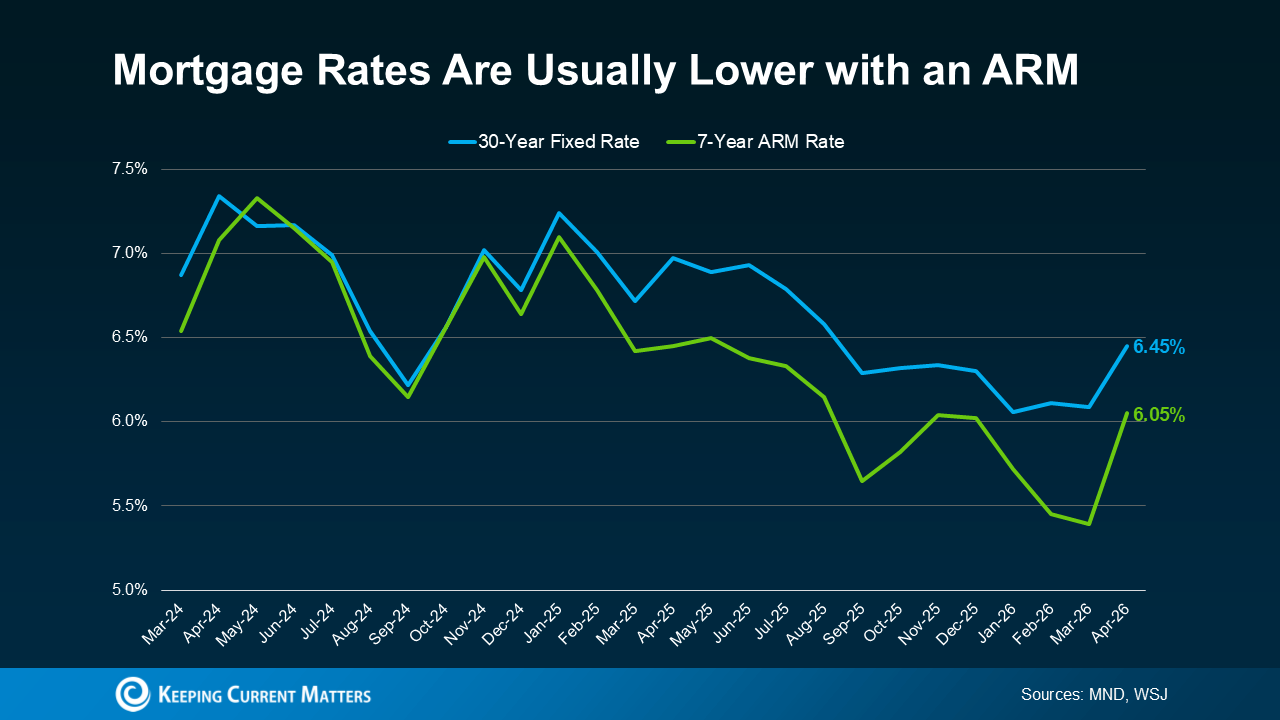

Right now, based on data from Mortgage News Daily and the Wall Street Journal, initial ARM rates are lower than those for a 30-year fixed mortgage.

If you’re wondering what that looks like in real numbers, Redfin reports that the average buyer could save about $150 per month by choosing an ARM over a 30-year fixed loan.

For many, that difference can be meaningful.

More Buyers Are Choosing Adjustable-Rate Mortgages Today

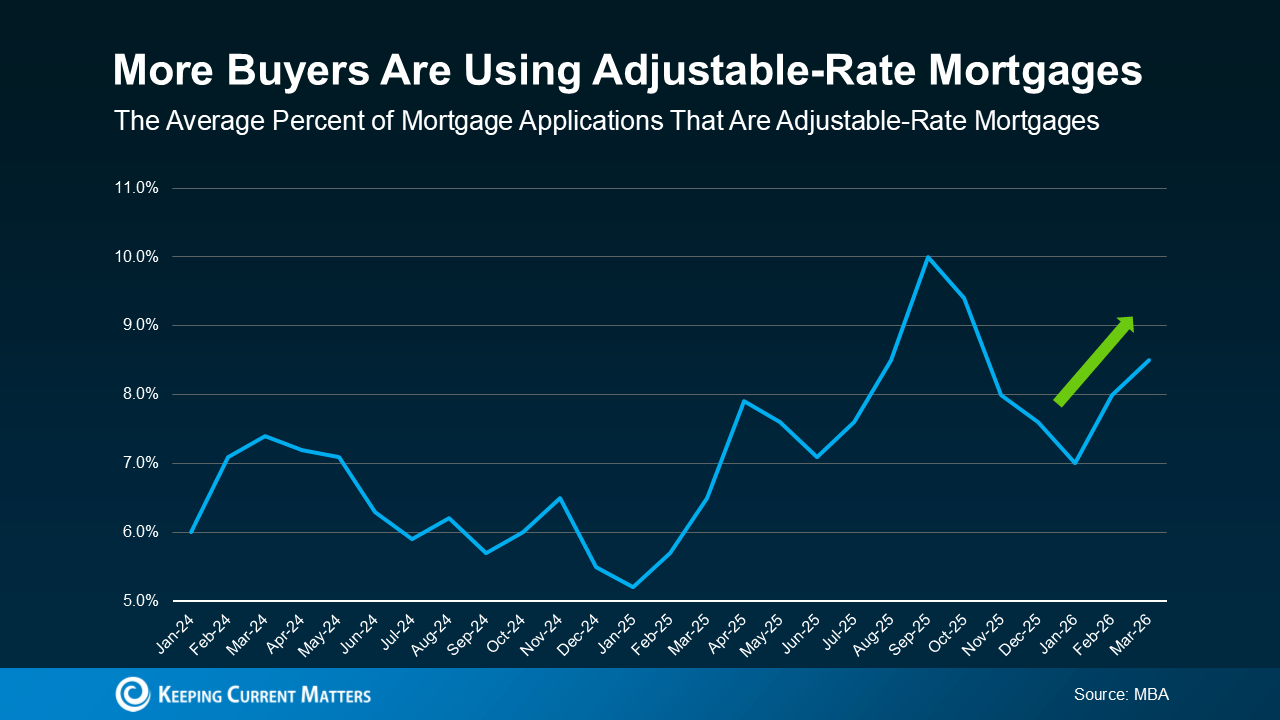

An increasing number of buyers are willing to accept some future uncertainty in exchange for lower payments today. Data from the Mortgage Bankers Association (MBA) shows that the share of buyers choosing ARMs has risen, particularly in recent years.

That doesn’t mean ARMs are becoming the default choice—it simply shows that some buyers are using them as a strategy to make homeownership more attainable right now.

If you remember the housing crash, this trend might sound concerning. But today’s ARMs are very different.

In the past, some borrowers were approved for loans they couldn’t afford once rates adjusted.

Now, lending standards are much stricter. Lenders assess whether borrowers can still manage payments if rates increase. So, the renewed interest in ARMs doesn’t signal another crisis—it reflects how buyers are adapting to today’s affordability pressures.

The Trade-Off – What You Need To Consider

If you’re thinking about an adjustable-rate mortgage, it ultimately comes down to your personal situation and comfort with risk.

An ARM might make sense if you plan to move before the rate adjusts, or if you expect your income to increase over time. Still, there are important trade-offs to consider.

Once the fixed-rate period ends, your rate can change—and your monthly payment could rise, potentially by a significant amount depending on market conditions.

Also, there’s no guarantee that mortgage rates will drop in the future, which means refinancing may not always be an option. That’s why it’s essential to have a clear plan, understand your long-term financial outlook, and work closely with a trusted lender before choosing this type of loan.

Bottom Line

ARMs are gaining attention again because they can offer lower payments upfront, making homeownership more accessible in the short term. But they aren’t the right fit for everyone.

The key is understanding how they work, weighing the risks, and deciding whether they align with your financial goals. That’s why it’s important to consult with a trusted lender and financial advisor before making any decisions.

{kind=link}